Watch China’s GDP for Signs of Post-Pandemic Slowdown

China GDP to Be Scrutinized for Signs of Post-Pandemic Slowdown

(Bloomberg) -- After China’s surprise central bank support last week, key economic data released on Thursday will be studied for signs the world’s second-largest economy is entering a new post-pandemic phase, where slowing momentum leads to new policy aid.

Debate is growing over whether China will shift from its gradual monetary and fiscal tightening, which began late last year after a rapid V-shaped recovery from the coronavirus pandemic. While the People’s Bank of China has said the cut to the reserve requirement ratio last week was a liquidity operation and not a sign of a change in policy direction, the sudden and broad move took many by surprise and stoked concerns about the growth outlook.

As well as the tapering of policy stimulus, the last quarter saw a range of headwinds to the economy, from surging raw materials prices to chip shortages in the automotive sector and localized virus outbreaks interrupting exports. The data will show how much those sector specific issues hit overall growth.

Premier Li Keqiang sounded a cautious note this week, warning that the nation needs to prepare for cyclical risks and make counter-cyclical adjustments. The government should focus on supporting smaller companies, he said, but reiterated that the government shouldn’t adopt flood-like stimulus policies.

Here are five things to look for in the second-quarter gross domestic product report and June activity data:

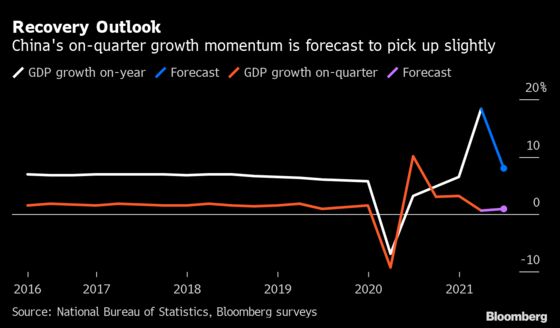

Growth Momentum

The sources that powered China’s recovery -- strong exports, property investment and industrial production -- remained solid in the first half of the year, but showed a moderation from the end of 2020 as developed economies normalized and Beijing tried to limit property speculation.

As a result economists expect headline GDP growth to slow markedly to 8% in the second quarter from the record 18.3% expansion seen in the first three months of the year. That is largely due to a rising base of comparison from a year ago, when China was already moving past virus lockdowns in the second quarter of 2020. Beijing is likely to look beyond the headline number to determine whether growth is slowing and the economy needs further policy easing.

To correct for that distortion, economists can look at official quarter-on-quarter growth, which is forecast to accelerate to 1% from 0.6% in the first quarter. The data is subject to frequent revisions though. The best alternative is to look at average two-year growth from 2019. By that measure, the line for quarter-on-quarter acceleration is anything above 5%.

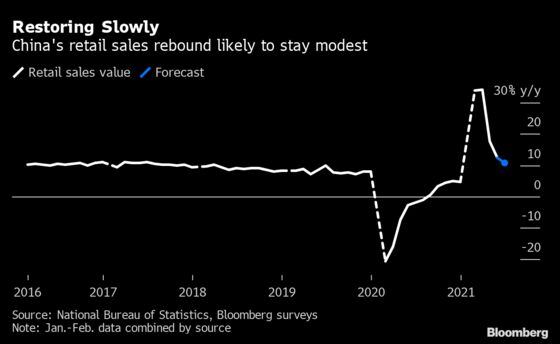

Consumption and Re-Balancing

Households are still cautious following the pandemic shock to incomes. Early indicators such as tourism spending suggested that remained the case in June, but the pace of consumer spending as showed by monthly retail sales has gradually picked up since the beginning of the year. The best gauge of momentum will be the 2-year growth rate, of retail sales, with a reading above May’s figure of 4.5% seen as an improvement.

“Near-real-time data show that online sales of some durable goods picked up month-on-month in June, after sharp declines in recent months,” analysts at Pantheon Macroeconomics said in a note. “We think this likely translated into a pick-up for the value of retail sales more generally, after two consecutive months of decline.”

But even optimists expect retail growth will remain well below pre-pandemic rates of around 8%. That means the economy is short of “re-balancing” toward one driven by consumer demand.

Unemployment data for June will show whether a tightening job market could help with that. Still, “China has a very long way to go before we can say that it is meaningfully re-balancing,” said Michael Pettis, a professor of finance at Peking University.

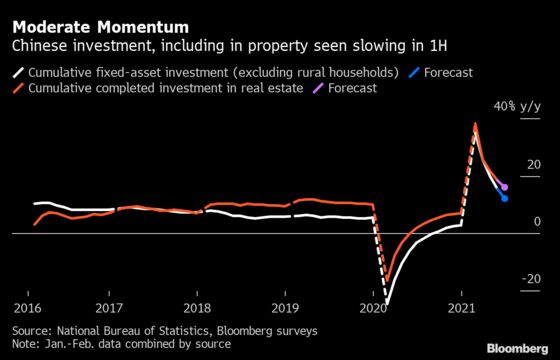

Investment and Commodities

The state of Chinese investment in property, manufacturing and infrastructure drives a global industrial and commodity cycle. Beijing tightened financing for property development in the first half of the year, while slow bond sales by local governments meant infrastructure investment was muted. Economists expect the slowing trend to continue, with fixed asset investment seen expanding 12% in the first half of the year, from the 15.4% increase recorded in January to May.

With base effects also at play, economists will look for a two-year average growth figure above 4.2% for the first half to indicate an acceleration. That could have been driven by year-to-date growth in manufacturing investment, which turned positive for the first time in the year to May. A bigger role for manufacturing investment could also mean that growth has become more sustainable.

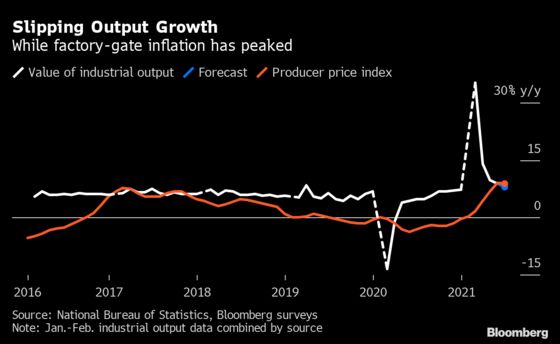

Industrial Output and Inflation

China saw record-breaking monthly production of commodities such as steel in the second quarter as exports and property investment remained strong and prices for industrial goods surged. However, factors such as the global chip shortage and new Covid-19 control measures introduced to combat coronavirus in the industrial heartland of Guangdong in June may have dented production of automobiles and some consumer goods.

Those factors mean economists polled by Bloomberg News expect industrial production expanded by 7.9% in June from a year ago, slowing from 8.8% in the previous month. Policy makers seem to have been effective in controlling price surges for now. An upside surprise from production data will give support to the idea that factory gate inflation will be temporary as supply catches up with demand.

Policy Rescue

If the data suggests a loss of momentum in the second quarter, Beijing is likely to try to avoid further deceleration. There are some tailwinds that could benefit the outlook: the last three months saw China supercharge its vaccine roll-out, administering nearly 1.4 billion shots -- about enough to fully vaccinate half the population, which could boost consumer confidence.

Analysts see at least two sources of policy support on the horizon. First, local governments are expected to increase the pace of bond issuance, boosting infrastructure spending. Second, there could be more room for monetary easing: export growth is expected to be strong in the second half relative to pre-pandemic levels, which will support the yuan and give Beijing more policy space to ease, even if that leads to more capital outflows.

©2021 Bloomberg L.P.

With assistance from Bloomberg