Cash Squeeze at Small China Banks Is Warning Sign for Market

China Funding Squeeze at Small Banks Is Warning Sign for Market

(Bloomberg) -- Some of China’s smaller banks are finding it increasingly difficult to borrow from each other, another sign that rising corporate defaults are starting to infect the financial system.

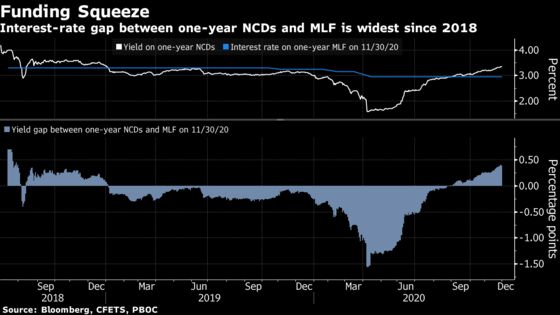

The cost of one-year interbank debt -- a lifeline for small and medium lenders -- was at 3.34% on Monday, or about twice what it was in April. The yield is now 39 basis points higher than the rate offered by the People’s Bank of China on its medium-term loans, the widest gap since July 2018.

China’s smaller lenders rely on cash from other banks because they don’t have direct access to liquidity offered by the central bank. A series of high-profile credit defaults have recently made China’s larger lenders more cautious in handing out funds. Brokerages and insurers are also grappling with a volatile market for short-term borrowing.

Another concern is that the People’s Bank of China may soon pull back on the emergency stimulus measures it deployed to support the economy during the virus pandemic. Recent economic data seem to endorse such a move, with an official gauge of factory activity climbing faster than expected in November. PBOC Vice Governor Liu Guoqiang said last month that tapering easing policies “is a matter of time and it is also necessary.”

It all means that even though the PBOC injected $30 billion with medium-term lending facility into the financial system on Monday -- after adding short-term cash every day last week -- those funds aren’t trickling down to some of the most vulnerable parts of China’s financial system.

| Read more on China’s credit market |

|---|

| China Defaults May Provide Investors With Increased Transparency |

| State Sector Defaults Raise Alarm Over China Local Town Builders |

| Can Banks Possibly Absorb All These Defaults?: Anjani Trivedi |

| China Unexpectedly Injects $30 Billion Into Financial System |

China’s borrowing costs will likely remain elevated, keeping government yields and the cost on interbank debt high in the near term, according to Larry Hu, head of China economics at Macquarie Bank Ltd. in Hong Kong.

“More defaults could happen next year due to the ongoing policy tightening and the growth deceleration later,” he said, adding the MLF injection doesn’t mean the PBOC has changed its stance.

Government bond traders seem to be pricing in tighter monetary policy. Futures on 10-year notes slid 0.19% on Tuesday, after a short-lived surge following Monday’s MLF injection. The yield on the notes in the cash bond market rose 2 basis points to 3.29% on Tuesday.

©2020 Bloomberg L.P.