(Bloomberg Opinion) -- For years, China’s biggest borrowers relied on accounting alchemy to prop up their balance sheets. Those days are over.

Corporate perpetual bonds have almost always been recognized by Chinese auditors as equity, not debt. That enabled state-owned enterprises to borrow billions of dollars without it showing up that way.

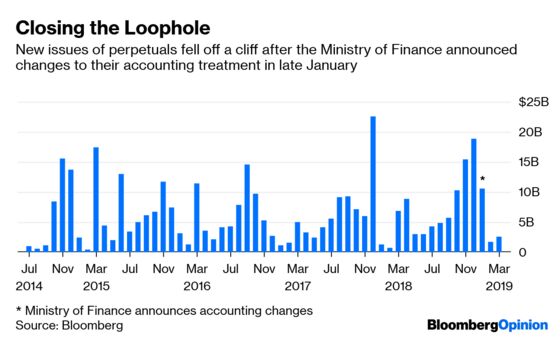

As part of its effort to shine a light on hidden debt, the Ministry of Finance earlier this year announced changes to its treatment of such securities. Now more than $360 billion worth of bonds could be reclassified as liabilities.

Of the 1,227 perpetual notes outstanding, almost all are issued by central or regional SOEs. It comes as little surprise that more than 70 percent of these issues get a pristine AAA rating.

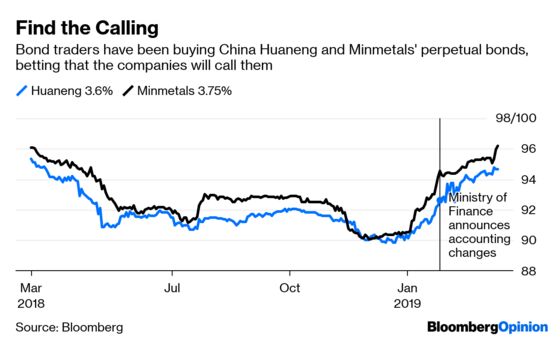

Perpetuals tend to have a call option, allowing the issuer to repay its debt in three to five years. If the borrower chooses not to do so, it has to reset its coupon rate, often paying 3 percentage points to 5 percentage points more. As a result, most chose to avoid the steeper interest costs: Of the 81 issues that have hit their call dates since issuance took off in 2014, roughly 90 percent decided to retire their debt.

In its announcement on Jan. 28, the Ministry of Finance decided these securities should be rightfully classified as fixed income. Perpetuals that have the same credit ranking as senior debt, or a step-up coupon rate much higher than the industry standard, also will need to be reclassified, the government said.

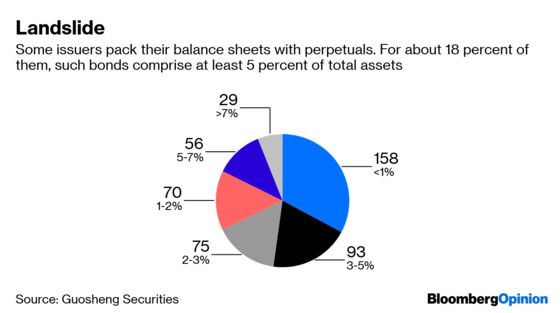

Over the past three years, loss-making SOEs from power generators to infrastructure builders embraced perpetuals. The latest accounting change could affect 80 percent of issuers’ leverage profiles, according to Guosheng Securities Co. China Communications Construction Co., for instance, which incurred a $7.7 billion free-cash-flow loss in the year ended September, would have seen its net debt-to-equity ratio jump to 121 percent from 92 percent.

The Ministry of Finance’s cleanup is also paving the way for China’s banking system to replenish capital. Just look at Bank of China Ltd.’s offering in late January, the first perpetual bonds from a Chinese lender. The People’s Bank of China established a new facility called the central bank bill swap that aims to boost bank liquidity through this channel. Insurance companies can also buy these bonds, China’s banking regulator said.

Now that perpetual bonds have become a new tool of the central bank, the market will no longer have room for the likes of troubled power generators and railway builders — even if they perform a public service at Beijing’s bidding. Meanwhile, the private enterprises farther down the totem pole simply lose an option they never really had.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.