(Bloomberg Opinion) -- China’s steelmakers have had enough of the squeeze.

The government needs to “maintain normal iron-ore market order” and push prices back to “reasonable levels” Qu Xiuli, vice chairwoman of the China Iron & Steel Association, or CISA, told a conference in Shanghai on Friday.

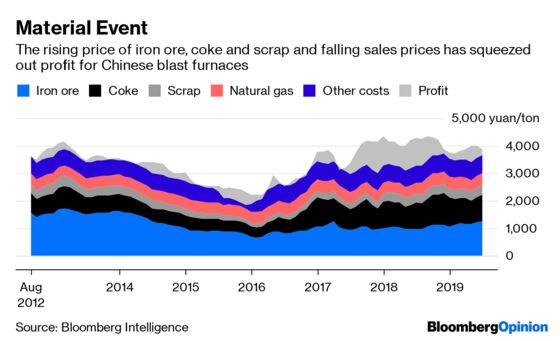

It’s not hard to understand the frustration. Iron-ore costs in June amounted to about a third of the revenue that Chinese steelmakers can expect to get for producing hot-rolled coil, in line with the highest proportion since 2017. Owing to a simultaneous rise in coking coal and scrap prices, operating margins were in the region of 5.3%, according to Bloomberg Intelligence data. At those levels, any steel mills bearing heavy debt loads will be flirting with losses on their raw production.

Unfortunately for CISA’s members, there’s not much Beijing can do about the price of iron ore. Singapore-traded contracts, as if to ram home the point, jumped as much as 3.9% on Monday morning.

The reason for this is quite straightforward. China simply doesn’t control enough iron-ore production to move the market if (as we’ve seen this year) major exporters Brazil and Australia aren’t shipping enough product. In contrast to thermal coal, where a sort of buyers’ cartel has managed to keep a monthly index of prices more or less in a band from 500 yuan to 550 yuan ($73 to $80) a metric ton since 2016, China is too dependent on the activity of mines outside the government’s control to be anything more than a price-taker.

Look at the sources of China’s bulk commodities and the contrast is clear. Imported coal accounts for no more than about 5% of demand – one reason the country has been able to play politics with major suppliers such as Australia by slowing and stopping imports. In iron ore, by contrast, more than half of the total is imported – and China’s dependence on trading partners is only rising as its domestic deposits are tapped out.

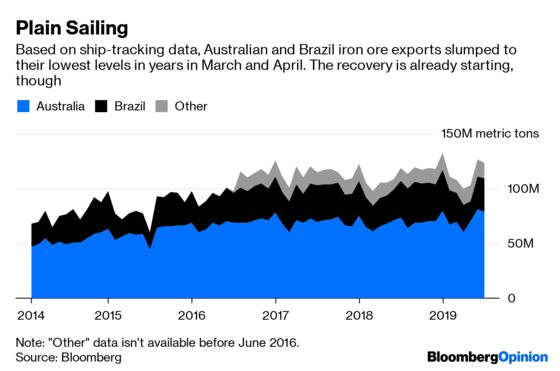

The basic reason that iron ore prices have almost doubled since the start of December is on the supply side. Brazil’s Brumadinho dam tragedy in January has led to a slump in exports that had been forecast to grow this year as the country’s S11D mine ramped up output. Two months later, Cyclone Veronica tore through Australia’smain iron ore-producing region. As a result, Australia’s March ore exports were the lowest in three years, while Brazil’s trade in April dropped to its weakest level since 2015.

To be sure, the last leg of the run-up in prices is hard to justify on the fundamentals. With supply from Brazil and Australia recovering, May’s shipments of 127 million tons were the second-highest on record; the demand side, meanwhile, has been fading, with China’s Caixin Manufacturing PMI showing a year-long contraction in that industry and fixed-asset investment in infrastructure on the floor.

The main driver of the latest spike looks to have been the continuing decline of port inventories of ore, an indicator that the market is running short of product – but even that has now turned up for the first time since February.

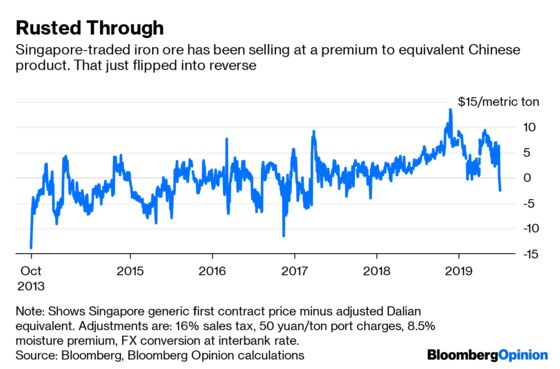

As a result, CISA’s complaint about prices could be dealt with by market forces well before the government gets round to intervening. The Singapore contract, which tends to be more exposed to the dynamics of China’s overseas suppliers, is trading at a significant discount to the more domestic-focused Dalian futures for the first time since 2017, suggesting major industry players are already backing out.

That should be little comfort to Chinese steelmakers. If there’s one thing that’s going to settle the market in the coming months, it’s that demand these days just isn’t what it was. Car sales – a major driver for producers of automotive steel such as Baoshan Iron & Steel Co. – have been in decline for a year, with numbers in the February low season hitting their weakest level since 2013. The Citi Economic Surprise Index for China stands at minus-48, close to its lowest levels since the country’s 2015 mini-slump.

When China’s steelmakers asked for lower iron-ore prices, what they really wanted was better profits – but it’s looking like they’ll only get the former as a result of losing the latter. Be careful what you wish for.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.