China Builders Weaken Debt Safeguards as Buyers Chase Yield

Warnings about bond covenants often seem to fall on deaf ears. Just ask Jake Avayou.

(Bloomberg) -- Warnings about bond covenants often seem to fall on deaf ears. Just ask Jake Avayou.

The senior covenant officer at Moody’s Investors Service has been cautioning for years that Chinese property developers are using their dominance of the Asian dollar debt market to borrow money from bondholders on looser terms. It’s a trend that shows no sign of going away: the average covenant quality score for property firms fell to the weakest last quarter since Moody’s began compiling the figures in 2011.

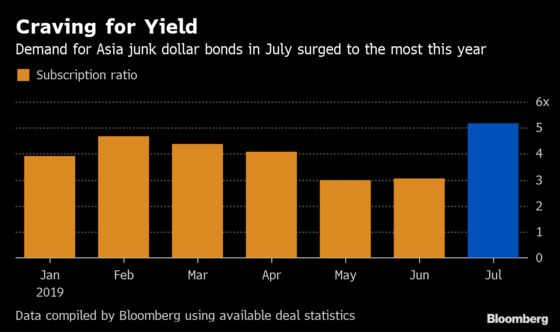

But a blistering 10% return on Asian junk bonds in the first half, of which Chinese real-estate firms account for a majority, saw investors take whatever they could get, with new deals underpinned by record order book sizes. That’s storing up risks on Chinese developer notes that may be getting closer to materializing, thanks to a surge in yuan volatility and curbs on financing that are behind an uptick in defaults.

“We are seeing this trend continuing ahead. There’s really less protection for bond investors now,” Avayou said. “It’s not only the top-tier developers which are having worsening covenants, but also some smaller and debut issuers have aggressive covenants too.”

Moody’s notes these concerns:

- Credit facility carve-outs that allow borrowers to load up on extra debt are getting larger. China Aoyuan Group Ltd., which Moody’s says had the biggest debt carve-out among deals priced in the first half, declined to comment when contacted.

- Fixed charge coverage ratios, which measures a firm’s ability to pay recurring expenses including interest, have fallen in recent years. This means it’s easier for issuers to borrow more.

- Among Chinese developer bonds rated by Moody’s, China SCE Group Holdings Ltd.’s $350 million 7.375% senior notes due 2024 had the weakest covenant quality score. China SCE said by email its dollar notes are issued under terms that are widely accepted by institutional investors.

Covenants in bond agreements are aimed at shielding bondholders against failures, but those terms are getting more borrower-friendly amid the blazing rally spurred by dovish central banks since start of the year. Chinese builders have sold a record $59.6 billion of dollar bonds so far this year.

For investors, the risks flagged by Moody’s have to be balanced against the challenge of delivering returns in a world where more than $15 trillion of debt pays a negative yield. Amy Kam, a London-based investment manager at GAM Investments, said that the market isn’t pricing in the weak covenant quality of some of these bonds.

Easing Bias

“With central banks worldwide again resuming an easing bias, this will translate into a return to the hunt for yield,’’ said Paul Lukaszewski, head of Asian corporate debt and emerging market credit research at Aberdeen Standard Investments. “This is likely to put issuers in a strong position, suggesting we will not see a change in this trajectory in the near term.’’

Company bond defaults in China hit a four-month high in July with the mainland real-estate sector topping the year-to-date onshore default list. China’s central bank recently urged banks to “reasonably” control lending to the property sector, and said it will step up supervision of already highly leveraged developers.

The recent slump in the yuan is also bad news for developers. “We expect that Chinese USD credit to be most adversely impacted by the weaker yuan and risk-off sentiment,” said Todd Schubert, head of fixed income research at Bank of Singapore Ltd, adding that the property sector is most vulnerable among Chinese dollar credits.

Andy Suen, a Hong Kong-based portfolio manager at PineBridge Investments Asia Ltd., is keeping an eye on the deterioration in covenant quality.

“While the loosened languages may not matter in a bull market, when the cycle turns, they could affect both default risks and recovery values," he said. Still, the fundamental impact on major borrowers is manageable and onshore investors may switch to buying dollar debt if the yuan softens further, he said.

--With assistance from Shawn Qiu, Rebecca Choong Wilkins and Natalie Lung.

To contact the reporter on this story: Annie Lee in Hong Kong at olee42@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Chan Tien Hin

©2019 Bloomberg L.P.