Bond Bulls Cheer Return of China’s Deflation Bugbear

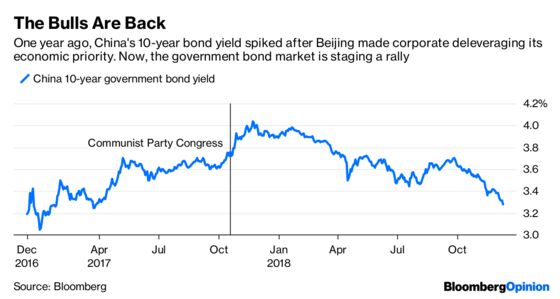

(Bloomberg Opinion) -- China’s $2 trillion government bond market has embarked on a bull run that would have been hard to envisage a year ago.

In December 2017, bond traders were watching nervously as the country’s 10-year yield spiked above 4 percent, sparking speculation of widespread corporate defaults. On Monday, the benchmark interest rate fell to 3.27 percent, the lowest since spring of last year.

It’s not hard to see why bullish spirits are being rekindled. With the U.S. 10-year yield at a four-month low, there’s less upward pressure on Chinese borrowing costs. Globally, rates tend to converge, especially when the world’s most powerful central bank is reversing a decade of easy money.

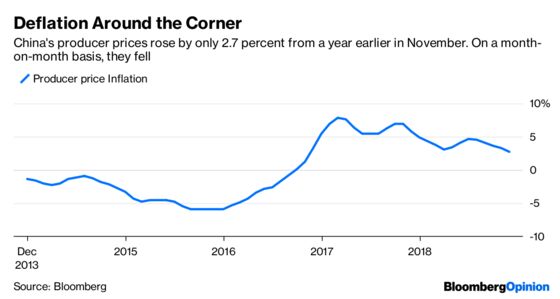

More importantly, the buzzword is no longer default; it’s deflation. Corporate deleveraging, an economic priority spelled out at the Communist Party Congress in October last year, is on the back burner. Of more concern is producer prices, which fell month-on-month in November.

If investors are pessimistic on the economy, it’s no surprise bond yields are declining. Amid a meltdown in the stock market, central government securities are seen as a safe haven.

The big worry is supply. If China relaxes its 2019 fiscal deficit target to 4 percent, how will Beijing fund it? Currently, the $11 trillion bond market is roughly split between the central government, policy banks, local governments and corporate issuers.

In the past, Beijing let provincial officials do the dirty work. Local governments lack reliable sources of income but are responsible for 90 percent of China’s infrastructure projects. As a result, while many local government financing vehicles are on the verge of default, the books of the Ministry of Finance look crispy clean and its securities are investment-grade.

It’s likely that the burden will fall on the local level again, because Beijing is eager to lure foreign money to the bond market. In August, the State Council said foreign investors will be exempt from taxes for the next three years. Next April, China’s yuan-denominated government and policy bank securities will probably be included in the Bloomberg Barclays Global Aggregate Index, the most widely tracked gauge for investors that buy both bonds and stocks, potentially triggering more than $100 billion of inflows.

So far, global fund managers have largely stayed away. Central banks account for about three-quarters of foreign holdings — most notably Russia, which has been selling U.S. Treasuries. The rest is dominated by Chinese banks’ overseas branches temporarily parking their offshore yuan deposits.

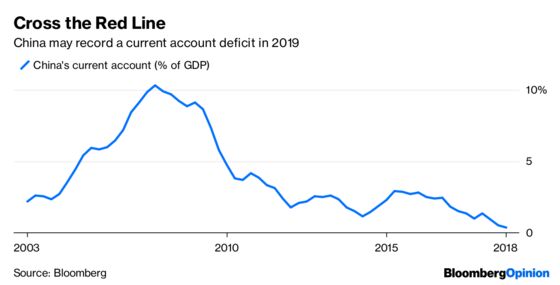

That’s not good enough. Next year, China will slip into a current account deficit and will need around $210 billion of portfolio inflows to keep its balance of payments stable, Morgan Stanley estimates.

As a result, a turbulent government bond market isn’t in China’s interest. Expect authorities to do what they can to keep the bull market going. As for local government financing, Beijing will kick that can down the road for another year.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.