Being Bullish on China Bank Stocks Is a Losing Game

(Bloomberg Opinion) -- Making bullish calls on Chinese banking stocks must be a depressing endeavor.

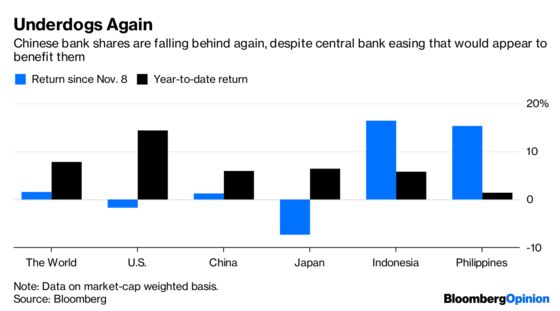

They’re falling behind again. On a market-cap weighted basis, the nation’s lenders rose only 6 percent this year, compared with a 14.4 percent rally for their U.S. peers. Financial institutions climbed 16.5 percent in Indonesia and 15.3 percent in the Philippines since early November, when the Federal Reserve took a dovish turn.

The divergence doesn’t seem to make sense. The U.S. yield curve continues to flatten, which in theory is bad news for American financials that rely on net interest margins. Goldman Sachs Group Inc. has soared 20 percent even while facing billions of dollars of damage claims from Malaysia over the 1MDB scandal. Even Morgan Stanley, whose bond trading revenue sank 30 percent in the fourth quarter, managed to eke out an 8 percent gain.

By contrast, macro conditions for Chinese banks look better. At the beginning of the year, the central bank cut the required reserve ratio for commercial lenders, sparking bets of many more reductions to come. A lower reserve ratio means banks will have more money to lend, and in turn can earn more. Meanwhile, 10-year bonds still yield 53 basis points more than two-year notes, a much steeper curve than in the U.S. Since banks borrow funds short-term from depositors and lend for longer periods, a wider spread makes their lending more profitable.

Beijing is opening new channels to help banks raise more equity. Last week, Bank of China Ltd. sold 40 billion yuan ($5.9 billion) of perpetual bonds, the first issue of its kind by a lender. The securities will count as tier-one capital. To boost demand for perpetuals, the PBOC said holders can swap them for central bank bills, and use them as collateral to access its liquidity facilities.

Does this mean that Chinese banks are only slowly waking up, in which case investors aren’t too late to join the rally, or that they are doomed to be a perennial underdog? The sector trades at an average of only 6.2 times earnings, among the lowest multiples in the world.

Investors are apprehensive because this isn’t the kind of easing that benefits banks.

It’s worth asking why the PBOC is cutting reserve ratios again. Lending to private businesses, which has long been neglected, is now high on Beijing’s agenda. Banks are being told that loans to the private sector must rise faster than other lines every year, eventually reaching at least half of new corporate advances. But in an economic slowdown, banks naturally shun smaller businesses (which are more likely to be private) because credit risk is higher. This forced counter-cyclical lending scares off stock investors.

Banks are also lending too cheaply, to please Beijing. At Industrial & Commercial Bank of China Ltd., the nation’s largest lender, the rate for loans to micro and small businesses under the so-called inclusive finance program fell to 4.35 percent in December, according to CLSA Ltd. That’s the same as the central bank’s one-year benchmark lending rate. For the risks commercial lenders are taking, this pricing has no logic.

Even perpetual bond sales can be looked at in a cynical light. Is the PBOC asking banks to create extra capital buffers because Beijing knows the zeal for inclusive finance will result in a tsunami of nonperforming loans?

During his Jan. 4 visit to an ICBC branch, Premier Li Keqiang was evidently delighted by a large banner displayed at the bank that said “there is no future without lending small.” Inclusive finance may well help the private sector. But bank shareholders should be wary – Beijing doesn’t have their back.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.