Get Used to It, America: We’re No Longer No. 1

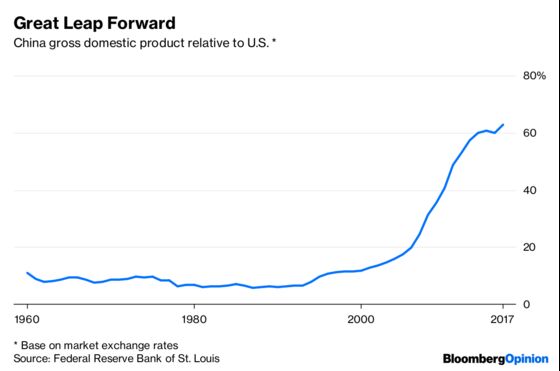

In 1997, China’s gross domestic product was about 11 percent of the U.S’s. By 2017, it was up to 63 percent.

(Bloomberg Opinion) -- What a difference two decades makes. In 1997, China’s gross domestic product was about 11 percent of the U.S's. By 2017, it was up to 63 percent:

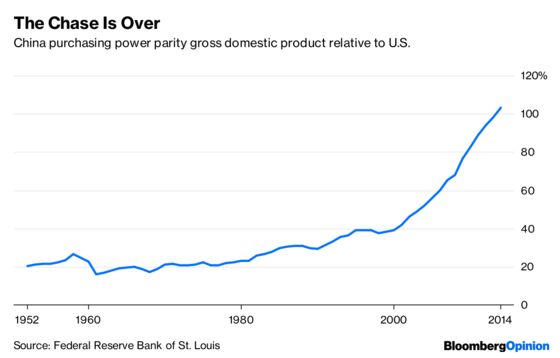

But this overstates the difference in living standards between the two countries, since prices are generally lower in China. In purchasing-power-parity terms, China’s economy became the world’s largest in about 2013:

So which country’s economy is really bigger? The truth probably lies somewhere between these two figures. If China were to abolish its capital controls and open its currency to foreign speculation, there’s a good chance the yuan would rise in value, bringing China’s GDP at market-exchange rates closer to its PPP numbers. In other words, the economies of China and the U.S. are now fairly evenly matched in size. But with four times the U.S. population, China has more room to grow. And China is already the world’s largest manufacturer and biggest exporter.

In other words, if it’s not already the world’s dominant economic power, China soon will be. But what does this mean? What are the implications of Chinese economic dominance, for the world and for U.S. policy?

The biggest effect will be that China becomes the leading beneficiary of what economists call agglomeration effects. Agglomeration refers to the tendency of businesses to cluster together in the same region, because one company’s workers are another’s customers. As economists Paul Krugman, Masahisa Fujita and Anthony Venables showed two decades ago, agglomeration can bring big benefits to whatever region has the densest concentration of economic activity.

Increasingly, that region is China rather than the U.S. China is where the biggest markets are, so that’s where multinational companies want to build their factories and offices. That in turn leads to whole supply chains migrating to China, as companies try to locate near their upstream suppliers and downstream customers. This process is accelerated by another phenomenon known as clustering effects — the collection of a huge repository of manufacturing talent and know-how in Chinese cities. China’s general hostility to foreign companies will slow this process, but the gravitational pull of the world’s biggest economy will be hard to resist.

This also means that President Donald Trump will be fighting an uphill battle in his trade war against China. To push a company to move out of China, U.S. tariffs would have to be very high, since they will have to overcome not just labor-cost differences between the two countries but the pull of the Chinese market, the concentration of manufacturing know-how, and the existence of stable supply chains. Many companies say they’re ready to pull out, but the reality may be very different — for example, last year Ford Motor Co. declared that it would build its next-generation car in China.

Another result of China’s new economic heft is that the web of institutions that the U.S. built to regulate the global economy after World War II will be increasingly irrelevant and toothless. The World Bank, for example, which lends money to poor countries, is already finding itself sidelined as Chinese loans pour into developing nations.

One of the most important U.S.-led economic institutions is the dollar itself. For decades, the dollar has functioned as the world’s reserve currency — nations around the world hold their foreign exchange stockpiles in dollars, many issue dollar-denominated debt, and commodities such as oil are often priced in dollars. Some believe this has put strains on the U.S. economy, because the increasing demand for dollars tends to make the currency more expensive, contributing to persistent U.S. trade deficits.

If this theory is right, then as China’s economy grows, the U.S. will be less able to handle the capital inflows that are necessary to remain the world’s reserve currency. It would seem like a good idea for China to shoulder some of the burden of being the global reserve currency, just as the U.S. took over this duty from the U.K. a century ago. But China insists on maintaining its system of capital controls, making it hard to move money in and out of the country. That will prevent the yuan from joining or replacing the dollar in international markets. But as China further eclipses the U.S. in size, that could lead to greater instability in the international monetary system.

The final impact of China’s economic rise is geopolitical. Countries that once would cater to the U.S. in military and political matters in order to secure access to U.S. markets will now be tempted to switch their allegiance to China. This pressure will be especially acute for East Asian countries that are close to Chinese markets.

The U.S., of course, could have acted to counter or slow this process by establishing a trading bloc with other East Asian countries that excluded the Chinese. President Barack Obama tried to do exactly this with the Trans-Pacific Partnership, but Trump killed that deal as soon as he came into office.

So the fact that China is now or will soon be the world’s biggest economy matters a lot. It means the U.S. can no longer depend as much on its large markets to secure investment or geopolitical fealty. Unless China makes severe missteps in the near future — like barring foreign companies, crushing productivity with excessive government control, or precipitating domestic conflict — it will enjoy many of the benefits that once flowed to its chief rival.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.