(Bloomberg Opinion) -- China has a standard road map for fixing state-owned giants that have gone off the rails: Create an even more inflated behemoth through a mega-merger, in the hope that the stronger business will be able to prop up the weaker one until the storm blows over.

It’s a playbook that’s been followed in steel, shipping, energy and rolling stock — but in the chemicals industry, it’s not working.

The country is planning to abandon the long-mooted merger of chemicals giants Sinochem Group Co. and China National Chemical Corp., or ChemChina, the Financial Times reported Thursday, citing people close to the matter it didn’t name. Executives at the two companies had clashed and Sinochem is likely to just buy some of ChemChina’s better assets instead, the newspaper reported.

It might seem remarkable that after about three years of will-they-won’t-they rumor, bosses at the two companies can’t get along. After all, both have the same chairman in Frank Ning, a Pittsburgh-educated dealmaker who ran state-owned grain trader Cofco Corp. before being brought into Sinochem in 2016. He was put atop ChemChina after its entrepreneurial boss Ren Jianxin retired last year.

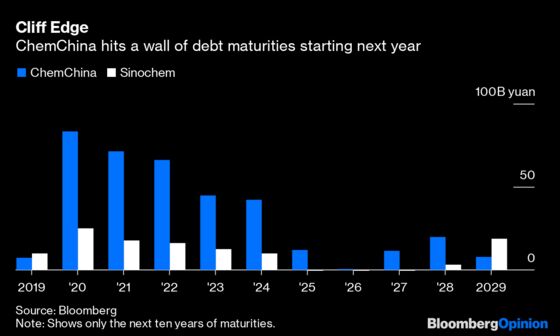

Still, it’s not hard to see why calling off the engagement makes sense for Sinochem, which has the better returns and lower debt levels. For ChemChina, with 83.37 billion yuan ($12 billion) of debt maturing next year and a negative 9.98 billion yuan of operating cash flows in the year through June, the prospects look tougher.

The two companies have had opposite approaches to making a profit in the fundamentally low-margin business of selling chemicals and fertilizers in a country where the government wants industrial and agricultural costs to be low.

Sinochem diversified into real estate and leasing, spinning off the property developer China Jinmao Holdings Group Ltd. and leasing firm Far East Horizon Ltd. into listings in Hong Kong. Jinmao’s net income of 5.2 billion yuan last year isn't far from the 6.5 billion yuan total for Sinochem’s main entity, and the chemicals company has brought in more cash from the business in recent months by selling off a stake to local life insurers.

ChemChina took a more globetrotting approach, making a splashy overseas deal for tire maker Pirelli & C. SpA followed by the $46 billion takeover of Swiss agribusiness giant Syngenta AG in 2016, when checkbooks for connected Chinese dealmakers were wide open. As the country has moved toward deleveraging in the years since, that strategy seems to have been its undoing.

Net debt more than doubled as a result of the Syngenta deal, overwhelming the ability of the investment to pay for itself. ChemChina’s adjusted debt at the end of 2018 was 10 times Ebitda, according to Moody’s Investors Service, well above figures that would be considered conservative. China’s ambassador to Switzerland in June described the deal as a mistake, an extraordinarily frank assessment from such a figure.

Things are likely to come to a head shortly. ChemChina’s 2020 debt maturities alone are equivalent to all the Sinochem debt maturing out to the start of 2029, according to data compiled by Bloomberg. After that there’s another 71.52 billion yuan to deal with in 2021 and 66.48 billion yuan in 2022, the data show.

One way around this would be the relisting of Syngenta, which could happen as soon as mid-2020 — but even selling half the business back onto the market at something close to the 2016 takeover price would represent an Alibaba Group Holding Ltd.-size share sale. That’s no easy task in the best of times; and given the signs of a deteriorating global economy there’s no guarantee that ChemChina could pull it off.

That could help explain why the company was holding out hope for a merger, but it’s understandable that Sinochem isn’t keen to see its debt blown up by another business. Its net debt at the end of 2018 was about 5.4 times Ebitda — a tolerable number by the standards of state-owned Chinese giants. Adding ChemChina to that total would have pushed the figure up to 7.5 times, far more risky territory.

No wonder the chemistry in this deal is lacking.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.