Chastened But Not Beaten, Emerging-Market Bonds Eye Reboot

Chastened But Not Beaten, Emerging-Market Bonds Eye 2019 Reboot

(Bloomberg) -- As the worst year for emerging markets since the financial crisis nears its end, bonds are looking ripe for a rebound in 2019.

With Federal Reserve policy tightening and the U.S.- China trade dispute battering developing-nation bonds, the year might have been expected to end with much more distressed debt, negative real yields and weakened government finances.

Far from it.

Besides China, where the property sector is under strain for domestic reasons, most emerging economies have seen distressed debt levels remain unchanged this year. Central banks have ensured currencies maintain yield spreads no matter what the Fed decides. Moreover, fiscal balances -- already looking healthy -- are projected to improve.

| This is the second in a three-part series on the 2019 outlook for emerging-market assets, which started with stocks on Dec. 4. Stay tuned for our analysis of currencies on Dec. 6. |

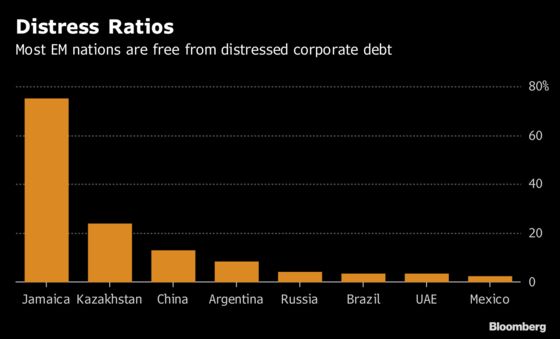

Dwindling Distress

Most emerging markets have few or no corporate bonds whose option-adjusted spreads over U.S. Treasuries are above 1,000 basis points, a typical definition of distress.

- Even vulnerable economies, such as South Africa and Turkey, are free of such contamination

- Commodity exporters like Russia and Brazil carry some legacy debt that’s in distress, but saw no addition this year

Bottom line: concerns that emerging markets are headed for defaults and restructurings are probably overblown.

| How we got the data: |

|---|

| Debt trading at least 1,000 basis points above Treasury yields as a proportion of country’s total debt. |

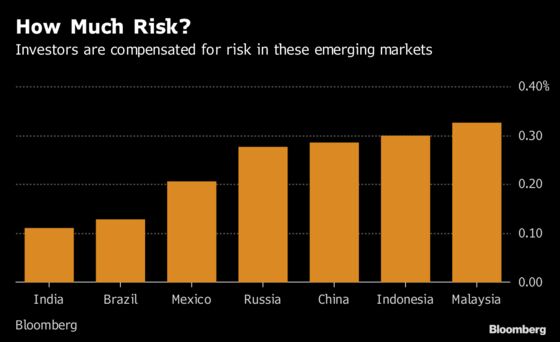

Real Yields

As central banks respond to the end of easy money and raise interest rates, yield differentials over Treasuries are luring back investors. But the higher returns don’t necessarily have to come with higher risk. The gap between policy rates and inflation rates is widening, and holding up even when corrected for volatility.

- Asian and Latin American currencies offer investors the best risk-adjusted returns

| How we got the data: |

|---|

| The spread between policy rates and inflation, divided by currency volatility. |

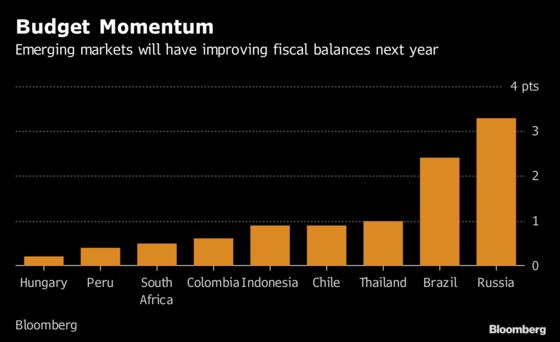

Fiscal Test

The challenge now is for governments to keep their economies growing at a time when borrowing costs are rising. Yet economists project governments will remain mindful of spending to avert fiscal shocks.

- Commodity exporters like Russia are likely to see the biggest improvement in budget balances between now and 2020

- While election action shifts to the east in the new year, the current-account and fiscal surpluses of many Asian economies provide a cushion against any rise in populism

- Meanwhile, the deficit economies of Turkey, Argentina and South Africa are projected to stabilize and offer a more conducive environment for capital inflows

| How we got the data: |

|---|

| The difference between the budget balances projected for 2018 and 2020. |

The Bloomberg Barclays Emerging Markets Hard Currency Aggregate Index trades at a one-month high, while its local-currency counterpart is near the highest level in six months. The extra yield investors demand to own sovereign dollar bonds of developing nations over U.S. Treasuries is at the widest since June 2016.

To contact the reporter on this story: Selcuk Gokoluk in London at sgokoluk@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Srinivasan Sivabalan, Robert Brand

©2018 Bloomberg L.P.