Central Banks Edge Toward Money’s Next Frontier in Digital World

Money is moving toward its biggest reinvention in centuries as central banks start to embrace the creation of digital currencies.

(Bloomberg) -- Money is edging closer toward its biggest reinvention in centuries as central banks start to embrace the creation of digital currencies.

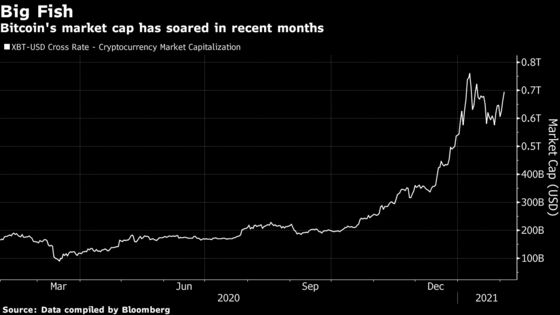

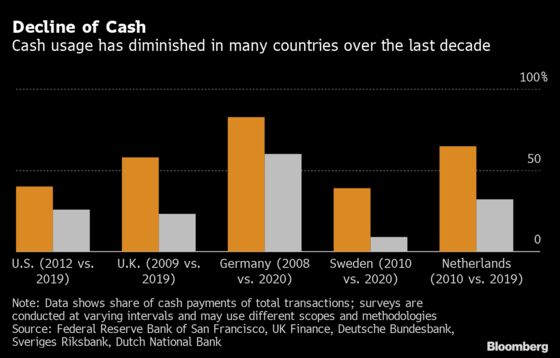

With modern technology and even the coronavirus facilitating a global shift toward cashless economies, and alternative concepts such as Bitcoin taking hold, monetary policy makers are acting to ensure they don’t fall behind.

That might one day mean central banks could make currencies directly available electronically for people to spend with their smartphone, backed by the integrity of the state. Before that comes to pass, a power struggle will play out over the future of money, raising issues ranging from privacy to social equality and financial stability.

“The whole effort is defensive,” said David Dollar, a senior fellow at the Brookings Institution in Washington. Central banks are “trying to get back into the key position to control currency and the money supply.”

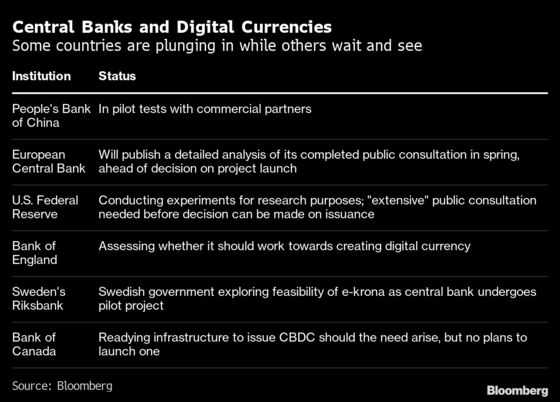

The most proactive country is China, conducting real-world trials of a digital yuan, partnering with the SWIFT global transactions system, and cracking down on payment services like Jack Ma’s Alipay to reassert supremacy over its currency. Elsewhere, officials from Frankfurt to Washington are watching closely, pondering experiments of their own.

The idea behind central-bank digital currencies is that, unlike conventional electronic money, they aren’t bound up with regular banks. Nor are they debts, as on a credit card. And they certainly aren’t a privately created currency like Bitcoin.

They are cash -- created by the state, just as notes and coins are -- held directly in a citizen’s electronic “wallet” or phone app. There is no financial middle man.

“If you look at the history of money, you had Phase One with the gold and silver coins of the Greek Islands, Phase Two was book money with the Amsterdam Exchange Bank, Phase Three was banknotes,” said Wouter Bossu, deputy head of the International Monetary Fund’s Financial and Fiscal Law Unit. Central-bank digital currency would be a “fourth form of money in human civilization.”

That idea is conceptually different to a so-called cryptocurrency like Bitcoin, which is too volatile to be a store of value and insufficiently widely accepted to be useful for payments. It’s more in the realm of a speculative asset. Likewise, tools such as Alipay are intermediary platforms for payment, not currencies in their own right.

In Shenzhen, the tech metropolis in southern China, citizens have already been testing out a trial digital yuan at Walmart, gas stations and convenience stores. In October, the central bank distributed the experimental currency via a dedicated smartphone app, which recipients use in a similar way to existing electronic payments.

One challenge confronting policy makers is that such a system offers less privacy than cash or other digital payments. That means weighing citizens’ discomfort about the ability of governments to track transactions against the legitimate need for authorities to stop money laundering and other financial crimes.

Even in China, privacy is a lingering concern. The People’s Bank of China has discussed allowing “controllable anonymity” -- meaning user transactions would not be generally known to each other but could be visible to the central bank.

Anonymity Vouchers

Such invasiveness would hardly be tolerated in Europe or the U.S., where policy makers like European Central Bank President Christine Lagarde are considering their own options. The ECB has explored the possibility of “anonymity vouchers”, allowing users to privately transfer a limited amount of digital currency over a defined period of time.

Another pressing issue is access. The need to use a smartphone and the Internet to spend such money could leave poorer people disadvantaged.

“Users need to have access to digital technology,” said Catalina Margulis, a lawyer for the IMF. “If universal access cannot be ensured by the state, it would raise fundamental questions about proportionality, fairness, and financial inclusion if CBDC acquired legal tender status.”

An even more existential question stems from the banking system’s structural reliance on deposits of income and savings. Until internet payment giants like PayPal or Alipay came along, normal financial institutions were often the only conduit for everyday transactions.

A digital currency issued directly by the state however wouldn’t necessarily use commercial banks, and that prospect is causing jitters.

In the euro area alone, lenders are sitting on some 11.4 trillion euros ($13.8 trillion) of household and corporate deposits, representing about a third of their funding. Migrating even a small portion of that to a central-bank currency would risk the stability of the banking sector and its ability to make loans to the economy.

“If you give easy access to central bank money, in an unlimited and seamless way, that can have an adverse effect on bank deposits,” said Benoit Coeure, former ECB Executive Board member and now head of the Bank for International Settlements’ innovation hub in Basel. “If not mitigated in some way, it could permanently change the status of bank deposits as a funding source for banks.”

Few central bankers have an interest in torpedoing, or even undermining, the financial system, even if they would like to regain some control over payments and money. That’s one reason why Coeure reckons progress on central-bank digital currencies will be slow.

Officials are also mindful of the next frontier in monetary policy, in an era when conventional stimulus tools such as interest-rate cuts are losing potency. A digital currency could offer the ability to boost economies more directly than ever by dropping cash directly into consumers’ wallets -- with all the dangers that might bring.

“A lot of central banks are rather uncomfortable talking about this because it suggests they’re contemplating helicopter money,” says Remi Bourgeot, an economist at the French Institute for International and Strategic Affairs in Paris.

One area of consideration in this connection centers around being able to make central-bank digital currencies “programmable” -- for example, offering money for loans that carries a built-in expiry date, or limited to certain purposes desired by policy. That could offer central bankers a range of tools with features they can currently only dream about.

Much discussion remains theoretical and unhurried for now. The U.S. Federal Reserve revealed last year that a group from the Boston Fed is working with the MIT Media Lab in Cambridge, Massachusetts on a research project to construct and test a hypothetical digital dollar, but Chair Jerome Powell insists it’s more important to be right than first.

China’s advanced progress with the digital yuan has taken some global peers by surprise however. Expectations of more developments are building, and a BIS survey released in January found that monetary institutions serving a fifth of the world population expect to issue a digital currency in the next three years.

“Central banks need to be prepared for how fast the space might move,” said Neha Narula, director of the Digital Currency Initiative at the MIT Media Lab. “It would be wise for them to be ready even if they have no interest in launching a digital currency, or might never launch one.”

| Read More... |

©2021 Bloomberg L.P.