Central Bankers Are Hitting the Pause Button

The Federal Reserve and fellow leading central banks are hitting the pause button when it comes to monetary policy.

(Bloomberg) --

The Federal Reserve and fellow leading central banks are hitting the pause button when it comes to monetary policy.

Faced with slowing global growth and inflation, policy makers are taking to the sidelines or even becoming dovish again. The Fed is signaling it won’t hike interest rates for a while if at all and the European Central Bank is lining up fresh stimulus in the form of fresh bank loans.

While the world economy may ultimately pick up by enough to prompt authorities to resume restrictive policies, chances are that for the major central banks at least the peak for rates is near and may have already been reached. Rates markets are already pricing in an even more dovish shift in monetary policy.

What Bloomberg's Economists Say: “A sharper than expected slowdown in global growth in the first quarter and risks tilted to the downside meant it made sense for central banks to go into wait-and-see mode. Looking forward, we expect growth to regain a little momentum. The next challenge for monetary policy makers will be to nudge markets away from their extreme dovish expectations.” — Tom Orlik

Here is Bloomberg Economics’ quarterly review of 23 of the top central banks, which together set policy for almost 90 percent of the global economy. We outline the issues they face in 2019 and how they might respond.

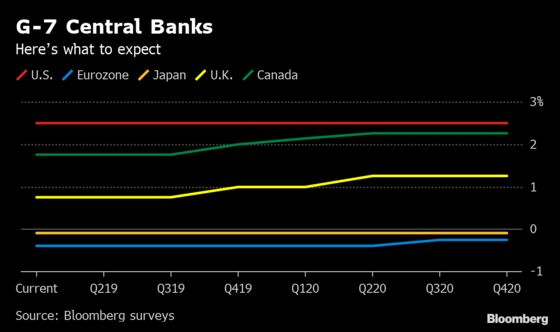

U.S. Federal Reserve

- Current federal funds rate (upper bound): 2.5%

- Forecast for end of 2019: 2.5%

The Fed made a surprising U-turn at the beginning of 2019 that eliminated expectations for an interest-rate hike this year, and then doubled-down on the dovishness at its March policy meeting by announcing plans to end the drawdown of its $4 trillion balance sheet. Now, as global growth looks shaky, investors see bigger odds of a U.S. rate cut before another increase. Lately, political pressure is building on Chairman Jerome Powell to keep the monetary medicine flowing. President Donald Trump and his economic advisers are publicly calling the Fed’s December rate increase a mistake and saying a 50 basis-point reduction in the federal funds rate, currently in a range of 2.25 percent to 2.5 percent, is needed immediately.

Fed officials maintain they’re relying on the economic data to guide them, stressing patience on rate moves as the nearly record-long expansion decelerates from a solid clip last year and inflation stays stubbornly below their 2 percent target.

What Bloomberg's Economists Say: “We have changed our Fed call to just one hike each in 2019 (December) and 2020. The extreme flattening of the yield curve in response to the Powell pause and a slew of weak economic data means that it will take longer for the Fed to get back onto a tightening track. However, following a soft patch in 1Q and possibly even spanning 1H, we expect growth to return to an above trend pace, which will in turn drive unemployment lower and wage inflation higher. Consumer inflation will perk up as a result. This will ultimately drive policy makers to conclude that an inflation-adjusted fed funds rate close to zero will need to be nudged a bit higher. The pessimism underlying the Powell-pause will ultimately prove overdone.” — Carl Riccadonna

European Central Bank

- Current deposit rate: -0.4%

- Forecast for end of 2019: -0.4%

In March, the ECB acknowledged the extent of the euro area’s slowdown and sought to alleviate it with a new round of cheap loans for banks and a prolonged pledge on interest rates staying low. President Mario Draghi then revealed that the central bank might need to soften the impact of its negative interest-rate policy on banks’ balance sheets. That could take the form of a tiered system as used by counterparts in Switzerland or Japan, but officials may take time to form a consensus on any such measure.

The new promise that interest rates won’t rise this year means Draghi is now sure never to raise them before his term ends at the start of November. Several candidates are vying to replace him, but the choice of president is yet to be determined by governments, probably some time after the European Parliament elections in late May.

What Bloomberg's Economists Say: “The slowdown in the euro area caused the ECB to change its forward guidance in March, indicating interest rates will now be on hold through the end of the year instead of through the summer. We expect the deceleration of GDP growth to be temporary and the pace of expansion to return to its trend rate in the second half of the year. That, in combination with underlying inflation slowly trending upward, should allow the Governing Council to raise the deposit rate by 15 basis points in March 2020.” — David Powell

Bank of Japan

- Current policy-rate balance: -0.1%

- Forecast for end of 2019: -0.1%

The Bank of Japan is looking less the odd one out amid talk of "Japanification" in Europe and the prospect of a return to monetary easing by some if its peers. But this does nothing to reduce the challenges facing Governor Haruhiko Kuroda. In fact, they just keep piling up. The Bloomberg Inflation Barometer, which draws on eight drivers of prices, points to a sharp slowing in the months ahead that may bring a spell of deflation this summer. More than a third of BOJ watchers now think Kuroda’s next policy move will be additional easing rather than a step toward normalization.

While Kuroda insists he has room to boost stimulus if needed, his huge asset purchases and ultra-low borrowing costs are taking an increasing toll on markets and the financial industry. Lending margins are being squeezed hard again as 10-year government bond yields fall to around the same level as its short-term policy rate. There are even signs that the government may be wavering on the 2 percent inflation target, with the finance minister calling for a more flexible approach to the goal. On top of all this, a sales-tax hike looms later in the year, bringing the risk of an economic contraction to round out 2019.

What Bloomberg's Economists Say: “With increasing external risks and sales tax hike slated for October, the BOJ should keep policy unchanged through mid-2020. Driving inflation to 2% quickly in the current environment would require the BOJ to push much harder on the monetary front to widen the financial gap. But that would come at the cost of even larger financial imbalances — which would make the economy more vulnerable during any downturn. It would probably take a sharp surge in the yen or a material deterioration in the growth outlook — something that shakes Governor Haruhiko Kuroda’s confidence that reflation is on track — to prompt the BOJ to increase stimulus.” — Yuki Masujima

Bank of England

- Current bank rate: 0.75%

- Forecast for end of 2019: 1%

Brexit is a big, dark cloud over the U.K. central bank. Governor Mark Carney has twice extended his planned tenure at the BOE to see through the departure from the European Union, but now that date itself is being pushed back and Carney insists he really will step down in January.

That may leave the next interest-rate move to his successor, as markets don’t foresee a follow-up hike to the one in August until well into 2020 (though economists still see the chance of tightening this year). Like the many U.K. companies that are scaling back investment amid the uncertainty, the BOE appears to be waiting on Brexit before making any more big moves.

What Bloomberg's Economists Say: “Investors have lost faith in the Bank of England’s ability to lift interest rates this year. We’re more sanguine. If global growth stabilizes and the U.K. avoids a no deal Brexit, as we expect, the central bank is likely to look for an opportunity to take some of the fizz out of the labor market. We have pencilled in a move in the summer.” — Dan Hanson

Bank of Canada

- Current overnight lending rate: 1.75%

- Forecast for end of 2019: 2%

Bank of Canada Governor Stephen Poloz has settled into an indefinite holding pattern on interest rates, dismissive of the idea the nation’s economy could fall into a recession and require looser monetary policy but equally reluctant to suggest the future will be rosy enough to warrant higher borrowing costs.

With five interest-rate increases since 2017, the Bank of Canada had been one of a handful to embark on sustained hiking. The recent global economic slowdown and a creaky housing sector in Canada has raised the possibility the normalization process has come to an end.

What Bloomberg's Economists Say: “Weakening global growth and growing uncertainty over trade relations are going to keep the Bank of Canada on the sidelines for the at least 2019. Inflationary pressures remain muted, giving policy makers time to assess whether the housing market and consumers — the latter weighed down by historic levels of debt — can find a second wind later this year. Still, the detrioration in global conditions, and flatter expected path of policy in the U.S., may mean we’ve seen the end of interest rate hikes this cycle.” — Tim Mahedy

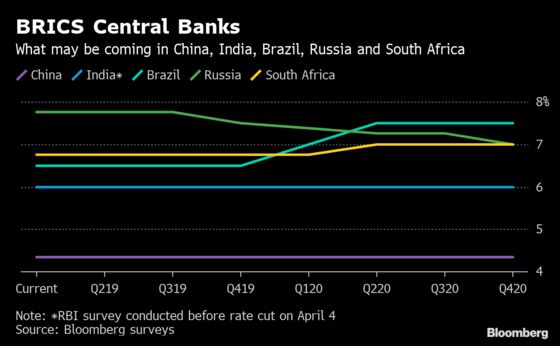

People’s Bank of China

- Current 1-year best lending rate: 4.35%

- Forecast for end of 2019: 4.35%

Expectation for more monetary easing has been dialed back a little, as economy shows some recovery signs and trade talks with the U.S. move forward. Liquidity injections via lower reserve-requirement ratios will continue but at a more moderate pace than last year.

The inflation outlook diverges between sectors. While factory-gate prices will probably flirt with deflation throughout the year, consumer inflation could accelerate close to the ceiling of 3 percent for the first time in many years amid soaring pork prices. Other central banks turning dovish puts a floor under the yuan, but it’s doubtful if China would agree to more on the currency front in trade talks beyond existing Group of 20 commitments. Tepid oil prices can help the country keep its full-year current account in a small surplus. The jobless rate is rising but from a low level. It’ll be a big concern for policymakers if it rises further.

What Bloomberg's Economists Say: “We expect further cuts in the reserve requirement ratio this year, on top of January’s 100 bps of reductions. Given the need to maintain support for bank lending, the next cut may come in the second quarter. A key aspect of the policy support is to unclog lending channels for funding to small private firms. To achieve this, the PBoC is expected to continue to use targeted measures such as targeted cuts to the reserve requirement ratio, targeted medium-term lending facilities, re-lending and rediscounting loans and credit support for smaller firms to issue bonds.” — Chang Shu

Reserve Bank of India

- Current repo rate: 6%

- Forecast for end of 2019: 6% (survey conducted before April 4 rate cut)

The RBI has been the most aggressive rate cutter of any major central bank this year, lowering borrowing costs twice to reverse the 50 basis points of hikes in 2018. Inflation remains well below the central bank’s medium-term target of 4 percent. That’s given Governor Shaktikanta Das room to support economic growth after it hit a six-quarter low in the three months ended December.

Aside from a global slowdown, uncertainty about the outcome of a general election that runs from April to May is clouding the outlook.

What Bloomberg's Economists Say: “A growth recovery requires much lower real interest rates. Below-target inflation gives the RBI room to provide further monetary policy easing. Our base case is for another 25 bp rate cut in June or August. Room for additional rate cuts could also open up, especially in the event of normal monsoon rains and oil prices staying benign.’’ — Abhishek Gupta

Central Bank of Brazil

- Current Selic target rate: 6.5%

- Forecast for end of 2019: 6.5%

New central bank chief Roberto Campos Neto is in a comfortable position, with inflation expectations anchored through 2021 and the benchmark interest rate at an all-time low. With little sign of price pressures and economic activity disappointing, analysts don’t anticipate any monetary tightening before mid-2020. Some even see the potential for easing this year.

In the first monetary policy meeting under Campos Neto, the central bank fueled such bets by saying risks to inflation are now even — a sign the next move could in theory be a rate cut if activity continues to weaken. Much of the bank’s policy approach, however, will depend on how successful President Jair Bolsonaro proves to be in achieving structural reforms, beginning with an overhaul of the pension system to ensure sustainability of public finances.

What Bloomberg's Economists Say: “The revamped BCB board has indicated, on its first meeting in March, that it does not intend to cut interest rates for now — but may be open to it later on, if the situation so allows and requires. In our view, a rate could come conditional on a combination of the following factors: an even more dovish Fed, a swift advance on pension reform in Congress, a decline in inflation expectations for 2020 to below-target levels, and continued negative surprises on growth. However, we do not believe this is the most likely scenario: we see the Selic stable through at least end-2019.” — Adriana Dupita

Bank of Russia

- Current key rate: 7.75%

- Forecast for end of 2019: 7.5%

After surprising most forecasters with two rate hikes late last year, the Bank of Russia is running out of reasons to stay cautious. A ruble rally and weak consumer demand helped blunt a spike in inflation from a Jan. 1 tax increase. Governor Elvira Nabiullina struck a slightly softer note after the last rate meeting, saying monetary easing could resume later in the year. Some economists have brought forward their forecasts for a rate cut to as early as June.

But the threat of further U.S. sanctions, which plagued Russian markets last year, hasn’t gone away and the central bank still has to keep one eye on geopolitics. Although initial reports of the results of Special Counsel Robert Mueller’s investigation weren’t as bad as many had expected, its conclusion that Russia interfered in the 2016 election could prompt U.S. Senators to push ahead with proposed penalties.

What Bloomberg's Economists Say: The Bank of Russia is done tightening, but a rate cut may not come until late this year. While price pressure has been more subdued than expected, inflation is well above target and could prove stubborn on the descent. Policy makers are likely to keep rates on hold until they see a sustainable downward trend. That should be apparent by the fourth quarter.” — Scott Johnson

South African Reserve Bank

- Current repo average rate: 6.75%

- Forecast for end of 2019: 6.75%

The South African Reserve Bank hasn’t had any MPC member vote for easing policy since March last year. While some people on the panel could start favoring rate cuts from the next meeting in May, they are unlikely to be in the majority. The appointment of a new deputy governor and sixth MPC member could change the weighting of the vote, but that may only happen after the May 8 election and won’t affect that month’s MPC meeting.

The central bank kept its inflation forecast for 2019 unchanged at 4.8 percent last month and slashed economic growth projections for the next three years, but Governor Lesetja Kganyago said the MPC wants to see price-growth expectations even closer to the 4.5 percent mid-point of the target range. The bank’s quarterly projection model still prices in one rate increase of 25 basis points by the end of the year and while that may not mean rates will rise, it does take cuts off the table for now.

What Bloomberg's Economists Say: “The SARB’s turn to a more dovish outlook in March has prompted calls for it to cut rates as early as by mid-year. Bloomberg Economics’ views these expectations as premature and see the SARB remaining on hold at 6.75% until the end of the year. The SARB has succeeded in bringing down inflation expectations but these gains could be quickly reversed as price growth is likely to accelerate and the rand remains vulnerable to financial outflows.” — Mark Bohlund

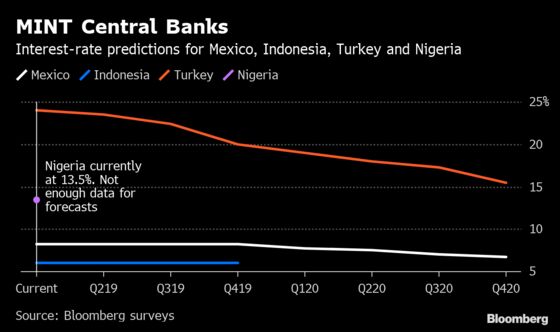

Banco de Mexico

- Current overnight rate: 8.25%

- Forecast for end of 2019: 8.25%

Mexico’s central bank last raised interest rates in December, and most economists believe that the tightening cycle, which saw rates almost tripled to a decade high since the end of 2015, is at its end. Attention has turned to when policy makers led by Governor Alejandro Diaz de Leon may be able to begin lowering borrowing costs.

On that question, economists are split. With inflation now below the 4 percent upper bound of the central bank’s range, some see reductions later this year, while the majority polled by Bloomberg expect the bank to wait until early 2020. Much may depend on the evolution of growth. The expansion in Latin America’s second-largest economy is expected to slow to 1.6 percent this year, the least since 2013, as U.S. growth decelerates and uncertainty over President Andres Manuel Lopez Obrador’s policies weighs on private investment.

What Bloomberg's Economists Say: “Already high interest rates and more moderate headline inflation imply the tightening cycle is over. But headline inflation remains high and together with resilient core inflation and inflation expectations suggest policy makers in Mexico are likely to maintain tight monetary conditions despite evidence of weaker economic activity and increasing slack in the economy. Lingering concerns about trade and economic policy are also obstacles to cut interest rates. Bloomberg Economics expects the central bank to maintain interest rates until lower inflation in the second half allows to cut interest rates late in 2019.” — Felipe Hernandez

Bank Indonesia

- Current 7-day reverse repo rate: 6%

- Forecast for end of 2019: 6%

After raising interest rates by 175 basis points last year to stem a currency rout, Bank Indonesia is getting a breather from a more dovish Fed and a recovery in the rupiah. Policy makers have dropped their hawkish rhetoric and shifted their focus to supporting economic growth through easing lending rules for banks.

While inflation remains benign — staying close to the lower end of the central bank’s 2.5 percent to 4.5 percent target band — Bank Indonesia isn’t ready to signal interest-rate cuts just yet. It’s still concerned about the current-account deficit, which reached a four-year high of 3 percent of GDP last year, and the economy’s vulnerability to currency swings.

What Bloomberg's Economists Say: “Bank Indonesia is working to support lending with ample liquidity and macro-prudential measures, all while ensuring the currency remains stable. The central bank has a cautious stance, signaling a willingness to hike further, if necessary. This suggests the policy rate won’t be lowered anytime soon. While we expect the next move in the policy rate to be lower, it’s unclear whether economic conditions will be all be in place for a rate cut before year end. The remaining hurdles for the rupiah are a narrowing in the current account deficit (which should happen in 1H), policy uncertainty (which should clear after April’s presidential election) and sustained risk appetite from global investors (which remains a wildcard).” — Tamara Henderson

Central Bank of Turkey

- Current 1-week repo rate: 24%

- Forecast for end of 2019: 20%

With Turkish inflation hovering at more than four times the official target, central bank Governor Murat Cetinkaya says he’s waiting for a “convincing” deceleration before resuming monetary easing. But his job could get more complicated soon as Turkish President Recep Tayyip Erdogan’s turns his attention back to cutting interest rates as he seeks to pull the economy out of recession.

Investors worry that the central bank will kick off an easing cycle sooner than warranted by the inflation outlook. But there’s reason to be concerned about growth, too: industrial production capped 2018 with its biggest plunge in more than nine years, and economic confidence languishes near the lowest level since the 2009 global crisis. Most economists predict that the central bank will start easing before the next quarter and on average see it delivering more than 350 basis points of cuts by the end of the year. Some investors are arguing that it may have to hold off on lowering rates until the second half though.

What Bloomberg's Economists Say: “Life was meant to be straightforward for the central bank. With the economy in recession and inflation falling, it was set to aggressively cut rates, starting in 2Q. The recent wobble in the lira changed all this. Instead of easing, the central bank effectively hiked rates on March 22. It could formalize this with a 150 basis-point increase in the repo rate at its next meeting in April. Monetary easing will probably have to wait until the second half of the year.” — Ziad Daoud

Central Bank of Nigeria

- Current central bank rate: 13.5%

The Nigerian central bank surprised in March with its first rate cut in more than three years. The market was pricing in some loosening for this year, but the move was earlier than expected, with Governor Godwin Emefiele saying monetary policy should help boost growth in an economy that’s still recovering from a 2016 contraction.

While Emefiele said price risks would moderate through the year, further big rate cuts may be complicated by possible inflation pressure from an increase in the nation’s minimum wage and the expected deregulation of the fuel price. The governor’s term ends in June. He could be reappointed, but if not, a change in leadership at the central bank is unlikely to drastically change the more accommodative policy trajectory.

What Bloomberg's Economists Say: “The 50 basis point rate cut in March came earlier than expected following the elections in February. Unrealized risks to inflation from election-related disruptions and spending are likely to have persuade the MPC to proceed with the rate cut. We expect 50-100 basis points of additional rate cuts this year but view additional easing at risks from renewed pressures on the naira’s peg to the US dollar. We expect the balance of payments to weaken from rising imports and weak financial inflows, and this could prompt the CBN to halt its monetary easing.” — Mark Bohlund

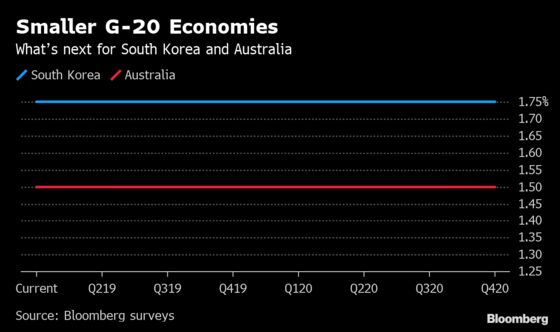

Bank of Korea

- Current base rate: 1.75%

- Forecast for end of 2019: 1.75%

South Korea’s three-year bond yield dropped below the central bank’s benchmark interest rate for the first time in years as headwinds buffeted the economy, stoking speculation that borrowing costs could be cut this year. Economists are yet to be convinced by the market moves. Most of them are still holding to the view that the benchmark rate will remain unchanged throughout 2019. Still, Governor Lee Ju-yeol has told parliament the Bank of Korea may consider adjusting policy if the economic slowdown becomes more pronounced. Exports and industrial production are weakening and the central bank has backed calls for more fiscal support. Lee has suggested that a supplementary spending package of about $9 billion would have a positive impact on growth.

What Bloomberg's Economists Say: “Despite pressures on growth and low inflation, the Bank of Korea will probably keep rates steady this year, reluctant to give up policy space it scraped back with hikes in 2017 and 2018. Governor Lee Ju-yeol has emphasized at the last two policy meetings that it’s not the time to cut rates, and has signalled the need for more expansionary fiscal policy to support growth.” — Justin Jimenez

Reserve Bank of Australia

- Current cash rate target: 1.5%

- Forecast for end of 2019: 1.5%

RBA Governor Philip Lowe is facing the most sustained pressure to resume cutting interest rates since he took the helm in September 2016. A once-in-a-generation plunge in property prices is spooking consumers out of spending and slowing economic growth. One of his few supports for holding the policy line is that unemployment has fallen below 5 percent for the first time in eight years.

Sydney house prices have tumbled and the economy decelerated in the second half of last year. This slowdown prompted money markets to start seriously pricing in rate cuts and they now expect two within 18 months, while economists have yet to catch up. Consumer spending — which accounts for almost 60 percent of GDP — has weakened as households struggle under one of the developed world’s highest debt burdens and stagnant real wages. Lowe maintains that as long as people have a job, they should be able to meet their financial commitments; he’s wary of easing further as cuts lose traction once the cash rate approaches 1 percent. He might receive a lifeline on the fiscal front: the government and opposition are pledging tax cuts and extra spending ahead of a May election as the budget returns to surplus. This could at least give Lowe more room for maneuver as he watches how events unfold at home and abroad.

What Bloomberg's Economists Say: “Developments in 2Q will be pivotal in determining whether the current level of stimulus is sufficient to keep the economy on track. For now, the Reserve Bank of Australia looks inclined to leave rates unchanged this year. Its focus is the labor market, where still robust hiring suggests a further pickup in wage growth. Beijing’s wide-ranging tax cuts and other stimulus should also start to benefit Australia’s goods and services exports. But visibility on the growth outlook is low, with still sizable monthly declines in house prices and a less positive outlook for global demand more broadly. Also, surveys suggest businesses are more wary. Markets are priced for a rate cut before year-end.” — Tamara Henderson

Central Bank of Argentina

- Current target: to freeze the expansion of monetary aggregates

Argentina’s central bank is maintaining the world’s highest interest rates and recently tightened policy even more as the nation grinds through recession. With the benchmark rate at 68 percent, the bank promised this week not to lower rates below 62.5 percent for all of April.

In March, it also promised to extend its policy of zero monetary base growth until December and reduce the money supply by an extra 10 percent. The moves are intended to cool stubbornly high inflation, which hit 51 percent annually in February. Despite its measures, the bank is already forecasting elevated inflation for March and April.

What Bloomberg's Economists Say: “Faced with a sequence of bad inflation readings, BCRA Governor Guido Sandleris doubled down on the current policies, in practice tying the BCRA's hands and making an unwarranted monetary easing virtually impossible. We view his move as correct, though it is hard to say at this point whether it will be sufficient. Resilient inflation and electoral uncertainty will likely keep local rates under pressure, closing the year still at high levels.” — Adriana Dupita

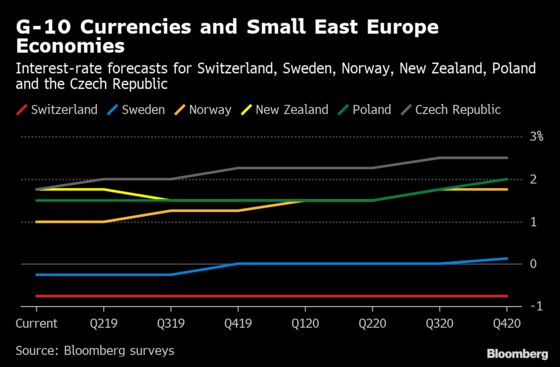

Swiss National Bank

- Current Libor target rate: -0.75%

- Forecast for end of 2019: -0.75%

With the European economy on shaky footing and the ECB pledging to keep borrowing costs at rock bottom for the rest of this year, the SNB is all but sure to stick with its current policy, consisting of the lowest interest rates of any major central bank plus a pledge to intervene in currency markets if needed.

The deposit rate has been at minus 0.75 percent since 2015, when the SNB gave up its minimum exchange rate, and raising it would risk increasing appreciation pressure on the franc, which is considered a haven currency. With an inflation forecast of just 0.3 percent for 2019, President Thomas Jordan and his colleagues have ample reason to keep policy accommodative.

Sveriges Riksbank

- Current repo rate: -0.25%

- Forecast for end of 2019: 0%

Sweden’s central bank raised rates in December for the first time in seven years and has flagged it will tighten again later this year to bring its benchmark back to zero. But doubts are starting to grow whether they will be able to amid slowing economic growth, more dovish colleagues abroad and slowing inflation.

Governor Stefan Ingves and his colleagues have so far sounded upbeat, arguing inflation has stabilized around the 2 percent target, as they prepare for the next meeting later this month. At that meeting, they will also decide whether to keep reinvesting proceeds from their massive bond portfolio, or call a final end to quantitative easing, at least for the time being.

Norges Bank

- Current deposit rate: 1%

- Forecast for end of 2019: 1.25%

Unlike most of its peers, Norway’s central bank is actually in tightening mode. Governor Oystein Olsen last month raised rates a second time since September, signaled that another increase could come as soon as June and predicted one more hike before the end of 2019.

The economy of western Europe’s biggest oil producer is benefiting from a rally in crude prices and unemployment is below 4 percent while inflation is above target. The krone has so far remained weak despite the country’s economic strength, giving the central bank further room to raise rates without hurting exports.

Reserve Bank of New Zealand

- Current cash rate: 1.75%

- Forecast for end of 2019: 1.5%

Governor Adrian Orr has unexpectedly put an interest rate cut in play, saying the more likely direction of the next move is down. He attributed his switch from a previous neutral stance to a weaker global growth outlook and the risks that slowing domestic demand will damp inflation.

Some economists are tipping rate cuts as early as May when the decision will be made for the first time by a new policy committee including external members. Other analysts say a tight labor market and rising dairy prices could yet persuade policy makers to stay their hand until later in the year, or indefinitely.

What Bloomberg's Economists Say: “The RBNZ abruptly changed gears in March, signaling the next direction in rates is ‘more likely’ to be lower. As recently as February the central bank had reaffirmed its forecasts indicating a bias for tightening, though not until early 2021. The shift puts the RBNZ policy bias in alignment with the rates market and should reduce upward pressure on the New Zealand dollar. Barring a sharp turnaround in the external or domestic climate, a 25 bps cut in 2Q looks likely. A complicating factor for the near-term policy outlook, though, is the operational shift in policy setting from April 1. From that point policy will be set by the newly established Monetary Policy Committee, rather than RBNZ Governor Orr on his own.” — Tamara Henderson

National Bank of Poland

- Current cash rate: 1.5%

- Forecast for end of 2019: 1.5%

Polish interest rates, on hold at a record-low 1.5 percent since May 2015, are unlikely to be changed this year. But while central bank Governor Adam Glapinski said in January that the longest ever pause in borrowing costs could extend to 2022, when the term of this Monetary Policy Council ends, doubts are starting to creep in.

A benign inflation outlook is being challenged by bumper pre-election spending that’s set to boost an economy already expanding at 4 percent on an annual basis. The MPC’s traditional hawkish minority is gaining wider support for the prospect of a rate hike in 2020, though a slowdown in the neighboring eurozone and concerns over global growth could yet deter policy makers from taking action.

Czech National Bank

- Current cash rate: 1.75%

- Forecast for end of 2019: 2.25%

The Czech central bank, one of the global front-runners in lifting borrowing costs last year, has paused its tightening push for three meetings. While domestic inflation is running above the target, policy makers are taking a cautious stance because of concerns about an economic slowdown in major export markets.

The central bank says the benchmark could rise twice this year, bringing real interest rates from negative to neutral levels. But Governor Jiri Rusnok says borrowing costs may also remain where they are. A lot will depend on whether Germany’s economy rebounds and domestic consumers boost spending again. A potential disorderly Brexit is also a big risk. “There aren’t fewer uncertainties, they are maybe even more complex than before,” Rusnok said after holding rates unchanged in March.

Methodology: Based on median estimate in monthly or quarterly survey, where available, or most recent collected forecasts. All interest rate and forecast data is as of April 3.

--With assistance from Hayley Warren, Theophilos Argitis, David Biller, Amanda Billner, Catherine Bosley, Paul Dobson, Natasha Doff, Patrick Gillespie, Michael Heath, Harumi Ichikura, Cagan Koc, Peter Laca, Andrew Langley, Cynthia Li, Eric Martin, Brett Miller, Brendan Murray, Prinesha Naidoo, Solape Renner, Catarina Saraiva, Tomoko Sato, Nasreen Seria, Sveinung Sleire, Craig Stirling, Karthikeyan Sundaram, Brian Swint, Tracy Withers, Sarina Yoo and Yinan Zhao.

To contact the editor responsible for this story: Simon Kennedy at skennedy4@bloomberg.net, Zoe SchneeweissFergal O'BrienLucy Meakin

©2019 Bloomberg L.P.

With assistance from Bloomberg