Central Bank of Surprises Could Spring Swiss Rate Cut on Market

With the franc having touched a two-year peak against the euro, and the European Central Bank readying another round of stimulus.

(Bloomberg) --

If there’s a lesson of history for when to expect the Swiss National Bank to ease its monetary policy, it’s this: don’t wait for a meeting.

With the franc having touched a two-year peak against the euro, and the European Central Bank readying another round of stimulus, Swiss officials face mounting market pressure to deliver a response of their own. They already appear to have resumed currency interventions. Sooner or later this year, they may need to resort to a rate cut.

The next scheduled SNB decision is still six weeks away, and officials would be breaking a longstanding habit if they acted then. The last time the Swiss cut the benchmark at a quarterly meeting was in 2009 -- and policy rates have dropped 150 basis points since then.

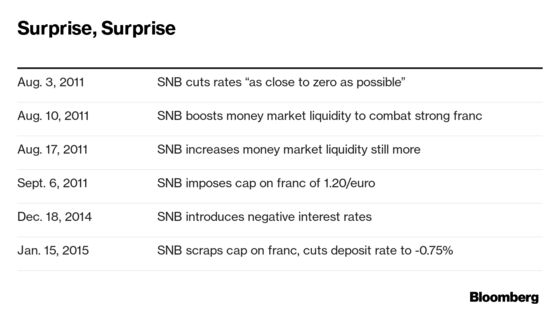

Instead, the SNB’s trademark style has been to deliver surprises: most notably, the market bombshell in 2015 when it gave up its exchange-rate limit on the franc with no prior warning, on a day no policy announcement was scheduled. Such a shock was all the more unsettling to traders used to prolific policy signaling by other central banks.

“We’ve all become accustomed over the last decade to being covered by all sorts of forward guidance,” said Jeremy Stretch, a currency strategist at Canadian Imperial Bank of Commerce. “That’s made us more susceptible to policy surprises.”

Stretch reckons opacity benefits the SNB. With an interest rate at -0.75%, already the lowest of any central bank and with limited room for maneuver, the institution’s silent treatment with the market means “you may get a slightly greater impact.”

With global trade disputes ramping up, investors have been seeking safety in the franc. The Swiss currency rose through 1.09 francs per euro earlier this week and was trading at 1.0931 at 9:37 a.m. Zurich time on Thursday.

By contrast, policy makers in the U.S., Britain and the euro region telegraph each move more explicitly in order to avoid causing an upset. Just last month, ECB President Mario Draghi teed up a new barrage of stimulus for later this year by saying that staff had been tasked with looking into the options for what action to deliver.

Clearly signaling the nature and timing of action has its critics. Bank for International Settlements Head of Research Hyun Song Shin argues it’s possible for monetary authorities to talk too much, and former U.S. Treasury Secretary Lawrence Summers recently criticized the “cacophony” of information the Fed participated in when delivering its rate cut.

SNB President Thomas Jordan doesn’t appear to be a fan of such signaling either. Unlike the Bank of England or the ECB, he doesn’t make predictions about the future path of interest rates.

No Warning

Any such communication “would always be conditional on what the ECB does or what happens to financial markets,” said Karsten Junius, chief economist at Bank J. Safra Sarasin. “So they don’t try.”

Jordan and his Swiss colleagues generally like to keep investors on their toes. Most recently, at their decision in June, they introduced a new benchmark interest rate and scrapped the old one -- again with no warning.

SNB officials are following a blueprint developed over the years that’s designed to take the wind out of the sails of speculators, whose trading has added to the real money capital inflows faced by Switzerland, exacerbating the pressure on the currency.

This time round, the central bank may choose to extend its defense of the franc a bit longer with interventions before escalating its response. Apart from cutting its interest rate, other tools it could use include tweaking rules that exempt some bank deposits from the penalty imposed by its monetary policy.

Of course, the SNB could always surprise people by breaking with its practice of springing surprises -- and deliver one at the next scheduled decision. That’s slated for Sept. 19, a week after the ECB meeting when Draghi is expected to cut interest rates.

--With assistance from Ven Ram.

To contact the reporter on this story: Catherine Bosley in Zurich at cbosley1@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Craig Stirling, Zoe Schneeweiss

©2019 Bloomberg L.P.