Central Bank Crusade to Spark Inflation Isn't Convincing Traders

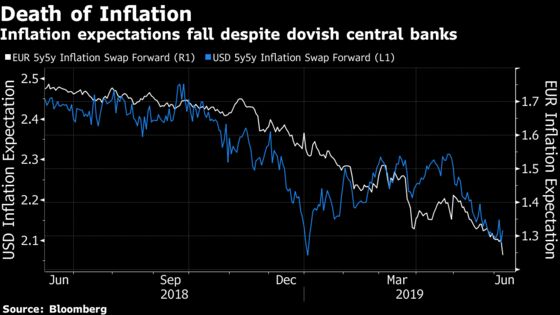

Long-term price expectations remain muted despite dovish turn.

(Bloomberg) -- The dovish turn by global central banks is failing to persuade investors that policy makers have what it takes to ignite inflation.

Spurred by flagging global growth and renewed trade frictions, the Federal Reserve and European Central Bank both flashed new willingness this week to deliver stimulus to their respective economies if necessary. Their counterparts in India and Australia went a step further and cut interest rates.

But investors are doubling down on bets that inflation won’t rebound. U.S. break-even rates, a proxy for inflation expectations, fell on Friday even as a big miss on jobs and wages prompted traders to up bets on the first Fed rate cut in a decade.

To boot, long-term price-growth expectations in the U.S. -- as captured by five-year, five-year forward inflation swaps -- have fallen toward a 27-month low. A similar gauge for the euro zone sits below its level during the financial crisis.

Markets may be pricing in concerns that central banks have less room to reduce rates than they once had. But there’s a more cynical way to read the numbers -- that policy makers are hamstrung in being able to spur price growth.

U.S. CPI data due Wednesday is likely to add to that worry as analysts forecast inflation rose just 0.1% in May from last month, down from 0.3% in the previous month.

Economists at JPMorgan Chase & Co. this week predicted average inflation in developed markets would slide to 1.6% by the end of this year from 2.1% in the current quarter.

“Low inflation is a global phenomenon,” said Zakaria Darouich, senior fund manager at Paris-based CPR Asset Management. “Years of record low interest rates don’t seem to have much impact on inflation. In terms of investment, we don’t have strategies in place that envisage inflation going back to targets in the near term.”

Part of the problem is that policy makers have little room to act. The Fed may have hiked interest rates from their record low but their benchmark range -- 2.25% to 2.5% -- is still below where it was in the run-up other economic slumps.

Less Ammo

Fed cuts to fight past recessions have tended to average 575 basis points, according to Bank of America Corp. analysts. The ECB and Bank of Japan, neither of which has tightened from record low rates, possess even less ammunition they can fire at weakening economies.

Other tools in the central-bank arsenal have sparked criticism in the wake of the post-crisis bond-buying spree. Quantitative easing is seen as having mixed results the more it’s deployed.

Low inflation tends to spur demand for bonds and push down yields as it’s interpreted as a signal of slowing growth. Falling yields can in turn prompt investors to turn to riskier assets like longer-dated securities or those with lower credit ratings for their higher returns.

Policy makers appear sanguine even as traders try to call their bluffs.

ECB President Mario Draghi said this week that the bank still has “headroom,” while Chair Jay Powell and fellow Fed officials met in Chicago to discuss ways of changing their monetary policy strategy to tackle a recession that may come sooner than they previously suspected.

Central bankers may be eyeing up the trade war as the biggest threat to their outlooks, but Citigroup Inc. economists take a dimmer view. Easing from central banks without fiscal support from governments won’t help policy officials achieve their inflation targets, Citi argues.

“Monetary policy is relatively impotent to achieve the desired outcomes,” said Cesar Rojas, an economist at the New York-based lender.

It’s often posited that forces such as ageing populations, technological advances and shifting labor trends are pulling down inflation. Offsetting these effects is more the job of governments than monetary officials, the argument goes, even as they too have little room to work given rising debt burdens.

“It is clear that central banks cannot do this alone,” said Paul Donovan, chief global economist at UBS Group AG.

--With assistance from Simon Kennedy and Liz Capo McCormick.

To contact the reporter on this story: Anchalee Worrachate in London at aworrachate@bloomberg.net

To contact the editors responsible for this story: Simon Kennedy at skennedy4@bloomberg.net, Yakob Peterseil, David Goodman

©2019 Bloomberg L.P.