Carney’s Warning That a No-Deal Brexit Would Mean Rate Hikes Draws Skepticism

Carney said that the BoE’s response to a no-deal scenario will be shaped by the demand and supply environment, and exchange rates.

(Bloomberg) -- Mark Carney’s warning that a no-deal Brexit would mean interest-rate hikes isn’t convincing economists.

The Bank of England governor says that crashing out of the European Union without a deal could trigger a supply side shock of a rare, once-in-a-generation magnitude. That would push up inflation and warrant tighter monetary policy.

But in the chaos of a disorderly exit, judging the extent of any hit to supply will be nigh-on impossible, meaning officials would probably be more defensive.

Carney himself was at pains to find comparable situations in major advanced economies -- he mentioned the oil shock of the 1970s, which sparked spiraling wages as output shrank. The only recent examples of central banks lifting rates while the economy tanks come from emerging markets such as Turkey or Argentina.

“It is possible that they could raise rates but I just think that would be contrary to their instincts at that time,” said Samuel Tombs, an economist at Pantheon Macroeconomics in London. “Their initial reaction will be to try and cushion the blow.”

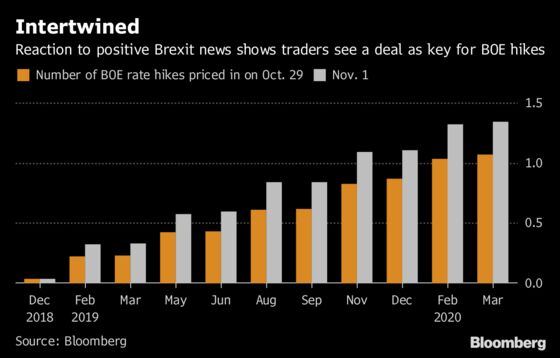

Investors also seem to have a clear view on what a chaotic Brexit may mean for the BOE’s outlook. Last week, an apparent impasse in talks saw traders push bets on the next hike into 2020, only for that to snap back on Thursday amid a flurry of reports suggesting a deal was more likely.

Carney has repeatedly said that the central bank’s response to a no-deal scenario will be shaped by the demand and supply environment, and exchange rates. On Thursday, he outlined a potential scenario where border delays, supply chain disruption and costly shifts in production patterns weigh painfully on U.K. producers, pushing prices higher.

| Read more: |

|

“If the outcome of Brexit negotiations is worse than expected, then the economy can weaken but equally the exchange rate can fall,” BOE Deputy Governor Ben Broadbent said in an interview with BBC Radio on Friday. “It’s difficult for the MPC to predict before we see what kind of deal is struck.”

The other argument for a hike after a no-deal comes from the emerging market playbook. Following a likely crash in the pound, the BOE could follow its counterparts in Turkey and Argentina by raising rates to stem the decline and mitigate against a large inflation shock.

That move could prove a hard sell.

“In theory it’s all well and good, but in practice whether a BOE Monetary Policy Committee would be sufficiently brave to take such action when the economy is weakening sharply and possibly entering a recession is an entirely different question,” said Philip Shaw, chief economist at Investec. “I’d be more than happy if we never got a practical demonstration.”

Another reason for skepticism is the reaction of officials to 2016’s referendum. While they made similar warnings about rate hikes before the vote, they ultimately chose to loosen rather than tighten policy in the aftermath to shore up the economy and mitigate the economic shock.

The August 2016 rate cut has since been more-than reversed, with officials using the supply-driven justification that that Brexit has reduced the potential growth rate of the U.K. economy, increasing the chance that it overheats. That same scenario could play out after a no-deal outcome.

“The BOE is trying cover all eventualities,” said Hetal Mehta, an economist at Legal & General Investment Management. “It does seem difficult to comprehend that an outcome associated with a GDP slowdown, or even decline, would be met with higher rates but, if the weaker pound pushes up inflation, it needs to consider the appropriate response.”

--With assistance from Anurag Kotoky.

To contact the reporters on this story: Lucy Meakin in London at lmeakin1@bloomberg.net;David Goodman in London at dgoodman28@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Brian Swint, Fergal O'Brien

©2018 Bloomberg L.P.