Carney’s 2017 Jolt Needed Again If He’s Serious About Hiking

Carney’s 2017 Jolt Needed Again If He’s Serious About Hiking

(Bloomberg) -- Go inside the global economy with Stephanie Flanders in her new podcast, Stephanomics. Subscribe via Pocket Cast or iTunes.

The Bank of England will be forced to dig out its old playbook if it wants to convince traders it’s prepared to move faster on lifting interest rates.

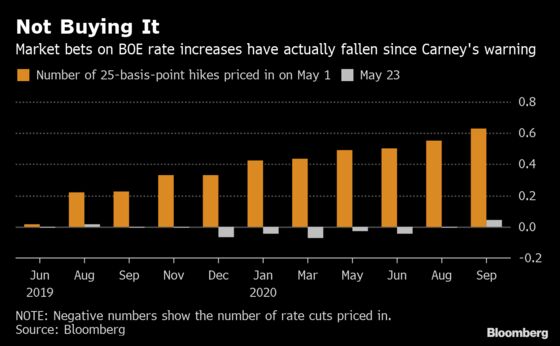

Governor Mark Carney said earlier this month that the current market curve showing one rate hike over the next three years was “unequal” to the BOE’s remit. That fell largely on deaf ears.

Berenberg’s Kallum Pickering said that “seldom do central banks say so clearly” that investors had got it wrong, but there was precious little in terms of market reaction.

More than two weeks later the curve is showing an even less optimistic outlook, with the latest bout of Brexit concern leaving markets seeing a less-than 5% chance of a hike before September 2020. In fact, traders now see a greater chance of a near-term cut.

The situation has echoes of the months before the bank’s first rate rise in more than a decade in November 2017.

Back then, the market was similarly unwilling to believe a hike was imminent, forcing officials to explicitly say in minutes of their September meeting that a move would be made “in coming months.” That statement, essentially a pre-commitment to hike, wasn’t universally popular within the BOE, but did the job, and meant that the increase in November didn’t upend financial markets.

The major difference this time round is a far greater dose of Brexit uncertainty. With the chance of a no deal exit growing amid the prospect that Prime Minister Theresa May is about to step down, investors just aren’t buying the BOE’s arguments.

That’s partly because the central bank’s forecasts -- including its hawkish view of longer-term inflation -- are based on the assumption of a smooth Brexit process. Investors, meanwhile, have the luxury of being able to take a more nuanced view.

“The market is convinced they won’t hike while political risk remains elevated,” said John Wraith, head of U.K. rates strategy at UBS Group AG. “To credibly indicate a hike may be a realistic prospect over the coming months, they would have to say something direct. They would have to sound hawkish, while explicitly warning ongoing political uncertainty will not be a barrier.”

The BOE is far from alone from having trouble controlling market expectations. The Federal Reserve and investors had a different view of the outlook for a long period following 2012, while emerging market institutions have also often struggled to convince traders of their messages.

According to HSBC Holdings Plc, the BOE isn’t making the most of the communication tools it has as its disposal, with vote counts and minutes showing only small differences in views and forecasts not adequately reflecting the range of possible scenarios.

“At some point it may need to be as explicit as it was in September 2017, when it basically said it would raise at the next meeting,” chief economist Simon Wells said.

To contact the reporters on this story: David Goodman in London at dgoodman28@bloomberg.net;Charlotte Ryan in London at cryan147@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Brian Swint, Jill Ward

©2019 Bloomberg L.P.