Can This Gold Rally Continue?

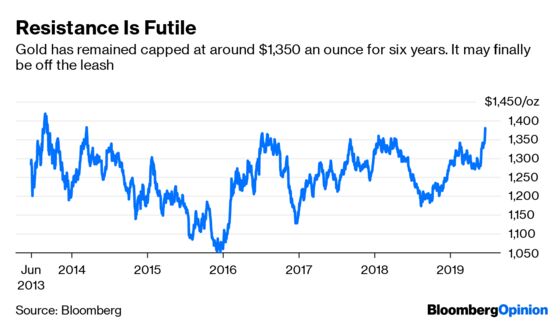

For the past six years, there’s been no number more filled with dread for gold bulls than $1,350 an ounce.

(Bloomberg Opinion) -- For the past six years, there’s been no number more filled with dread for gold bulls than $1,350 an ounce.

Barring a few brief spikes, the metal has struggled to break through that level ever since it came off its run-up to $1,900 between 2011 and 2013.

This matters, because an asset that has few fundamental factors drivingits performance (short of its negative correlation to the greenback) is unusually susceptible to the psychological hocus pocus that can sometimes make technical analysis work.

Thousands of investors believe that $1,350 an ounce is a “resistance level” that gold will struggle to break above. As a result, they’re likely to sell hard as the price approaches that point, and change their view of things if it confounds them by decisively moving higher.

It looks like we’re in that territory now. After a momentary incursion above $1,350 on Tuesday, spot gold decisively broke through on Wednesday afternoon and climbed as high as $1,394 early in the Asian day Thursday. That’s its most elevated level since September 2013.

The question is whether this is just another temporary spike.

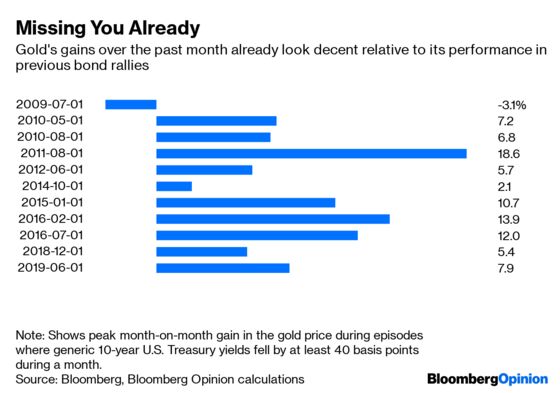

There’s some reason to think the best is already behind us. Investors tend to flock to the yellow metal when expectations of economic growth suffer a sharp setback. If you consider flight-to-safety sovereign bond rallies over the past decade, the median peak gain for gold has been 7.2%. This time around, we’re already sitting on an 8% rise.

At the same time, there are signs of a more dramatic re-evaluation of economic prospects than we saw in gold’s previous pips above $1,350 in July 2016 and March 2014.

Federal Reserve Chairman Jerome Powell opened the door to interest rate cuts as early as next month in a media briefing after the central bank’s policy meeting Wednesday – almost certainly the main reason that gold has been looking so peppy. If the Fed cuts in July, it’s more likely to be by half a percentage point than a quarter-point, Robert Mead, co-head of Asia-Pacific portfolio management at Pimco, told the Bloomberg Buy-Side Forum in Sydney on Thursday.

Should the Fed ease significantly – providing a “Powell put” to bail out an economy struggling under the weight of trade tariffs – you can expect to see a marked weakening of the dollar. That, in turn, ought to be good for gold.

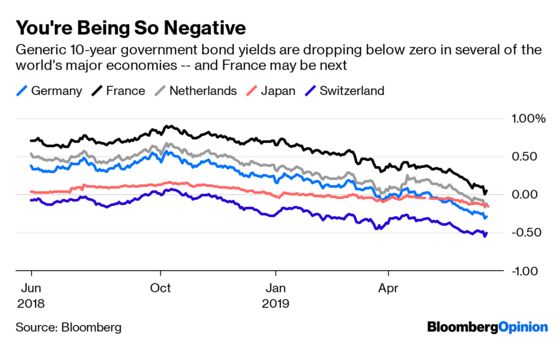

The deteriorating economic picture in Europe should also provide support. Gold doesn’t produce a return, but that’s not the disadvantage it once was in a world where sovereign debt in Germany, Sweden, the Netherlands, Switzerland, Denmark, Austria and Japan – and, perhaps soon, France – provides negative yields.

Funds so far seem unconvinced. Money managers, a group that’s been relentlessly bullish on the prospects for gold futures and options over most of the past decade, have been net-short for 24 weeks out of the past year and were still expecting price falls just last month. While that spiked up to a net-long position of 156,718 contracts in the most recent week, such data is subject to sharp reversals whenever movements in the underlying asset give investors a chance to take profits.

Still, in a world where uncertainty seems to spike every time the U.S. president opens his Twitter app, it’s hardly surprising a metal that thrives on chaos is finally getting its moment in the sun. The $1,350 level has been a price ceiling for gold for nearly six years. It could just as easilyturn into a floor in the future.

We're defining this as episodes when the yield on benchmark 10-year U.S. Treasuries fell by 40 basis points or more from a month earlier.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.