ADVERTISEMENT

Bunds Can Get Richer, So Maneuvering for a Selloff Needs Options

Bunds Can Get Richer, So Maneuvering for a Selloff Needs Options

04 Sep 2019, 01:23 PM IST

(Bloomberg) -- Bunds are trading rich against macro fundamentals, though fading the rally is not compelling in a world of trade uncertainty and bimodal nature of Brexit risk.

Any tactical sell-off in bunds on profit-taking of the extreme ECB easing expectations priced by markets may be captured by put spreads rather than outright short duration.

- Rate-cut expectations and the uncertainty associated with that path -- or the term premium -- are key to determine how low yields can fall, as seen in the case of the 10Y Swiss yield exploring sub-negative 1% with SNB policy rates at -0.75%

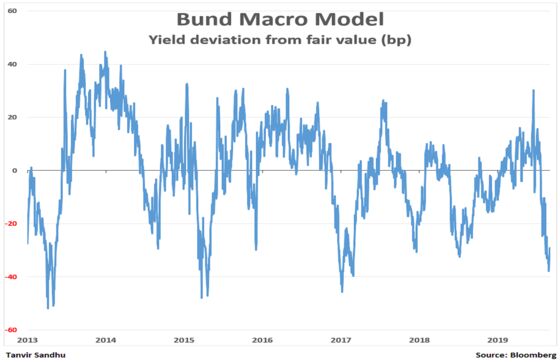

- The 10Y bund yield has been tracking ECB easing expectations, which now prices SNB-level policy rates and are reflective of a severe recession, as well as central banks’ inability to restore inflation

- It’s trading 31bps rich when modeled against macro fundamentals, implying a fair value of -0.43% vs current -0.74%, but the uncertainty of the outlook dominates taking any outright short

- Also, it’s not as rich relative to macro indicators as it was in the run-up to the 2015 bund VaR shock episode and the 2017 French presidential election

- The bar is low for ECB to disappoint next week with Eonia forwards already priced for 17bp of cuts in September and 40bp by the end of next summer

- A bund put spread would benefit from a tactical short-term sell-off if the easing package delivered is seen as modest

- For example, October 2019 176/173 put spread costs 70 cents, with the strikes having equivalent 10Y German yield of -0.69% and -0.50% respectively (compared to current yield of -0.74%)

- The steepness of the put skew helps reduce the cost of expressing a view for a limited sell-off, with pension and insurers likely to buy the dip and it remains skeptical whether ECB can get ahead of the curve with monetary policy alone

- NOTE: Tanvir Sandhu is a global fixed income and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2019 Bloomberg L.P.