Britons Reduce Spending and Lift Savings in Virus Crunch

Britons Reduce Spending and Lift Savings in Coronavirus Crunch

(Bloomberg) -- Britons responded to the coronavirus crisis by slashing spending and saving more as the economy slipped into what may be the deepest slump in at least a century.

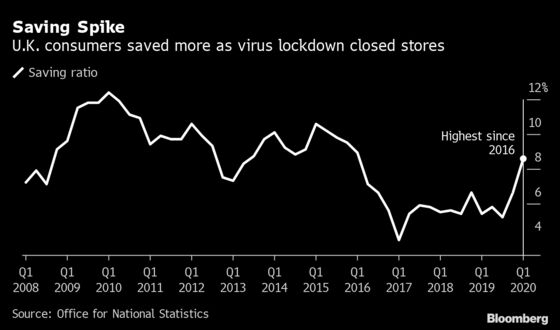

Households saved more of their disposable income in the first quarter than at any time for four years, thanks in part to the closure of all but essential stores after the country went into lockdown on March 23. Nominal spending fell an unprecedented 9.5 billion pounds ($11.7 billion), or almost 3%, as less was spent on cars, eating out, hotel stays and clothes. By contrast, incomes were down only marginally.

With government wage subsides meaning that furloughed workers are experiencing only a limited loss of income, the saving ratio -- which reached 8.6% last quarter -- is expected to climb further. How quickly the economy bounces back will largely be determined by whether people feel confident enough to spend their spare cash as the lockdown restrictions ease.

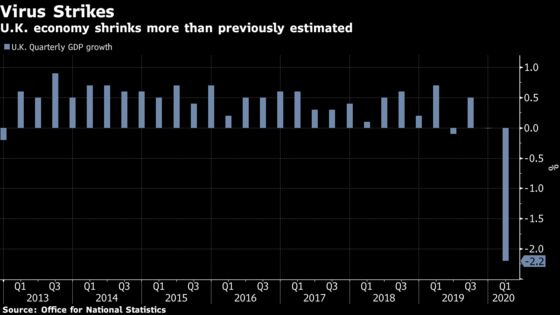

The Office for National Statistics said Tuesday the economy shrank by 2.2%, slightly more than the 2% previously estimated, but the real damage inflicted by the pandemic came in the second quarter. Gross domestic product shrank by over 20% in April and jobless claims soared, leaving many Britons worried about the future.

The data come as Boris Johnson prepares to set out his plans to revive the economy. In a major policy speech, the prime minister will promise to “build, build, build” with 5 billion pounds of accelerated investment in roads, schools and hospitals.

Separate figures showed the current account deficit widened to 21.1 billion pounds in the first quarter, the equivalent of 3.8% of GDP.

Britain posted a small trade deficit compared with a surplus in the previous quarter, as both exports and imports fell amid disruptions caused by the pandemic. The deficit on investment income also widened, driven by a decline in the earnings U.K. investors get on their foreign holdings.

The fall in GDP in the first quarter was the largest since 1979. Consumer spending plunged 2.9%, the most in 41 years, government spending fell a record 4.1% and business investment declined 0.3%. On the output side, the dominant services industry shrank a record 2.3%, led by health and education. Manufacturing and construction also contracted.

It left GDP 1.7% lower than a year earlier, the first annual decline since the financial crisis over a decade ago.

There was also evidence of a “dash for cash,” with financial institutions seeing deposits placed with them jump a record 820 billion pounds as investors switched to safer investments amid global market turmoil. They funded the deposits by issuing new loans, and short-term borrowing rose by a record 305 billion pounds.

Almost every industry saw profits decline in the period, the statistics office said.

©2020 Bloomberg L.P.