Crude Touches One-Week Low as Iranian Shortage Fears Are Eased

Oil in London extended losses below $84 a barrel after Saudi Arabia said it can tap its spare production capacity immediately

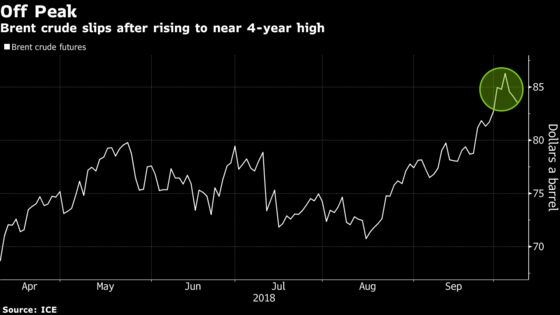

(Bloomberg) -- Oil slipped to a one-week low amid signs that Iranian supply disruptions may not be as severe as expected.

Futures declined 5 cents a barrel on Monday after last week touching the highest since 2014. U.S. government officials were said to be in talks with countries seeking exemptions from American sanctions that will ban crude purchases from Iran within weeks. Saudi Arabia and allied producers already have raised output to mitigate any drop in Iranian exports.

Absent clear indicators of fundamental supply and demand trends, so-called technical signals followed by chart-watching traders may hold sway. The next bearish threshold is the 20-day moving average just below $72 a barrel.

“Oil is going to do one of two things -- make another leg higher after this little pullback, or it’s likely to retest $71-72,” said Josh Graves, senior market strategist at RJO Futures in Chicago.

Oil has rallied since early September on concerns that OPEC and other major producers wouldn’t raise output enough to make up for the squeeze on Iranian shipments. Major buyers of crude from the Islamic Republic have been shunning or scaling back purchases as a Nov. 4 cutoff date set by the Trump administration approaches.

Meanwhile, Hurricane Michael is poised to hit the Florida Panhandle and is forecast to become the second hurricane to make landfall in the U.S. in a month. Offshore oil and natural gas producers have begun shutting down installations on the Gulf of Mexico, taking 19 percent of the Gulf crude production offline.

See Also: United States Oil Fund Sees Biggest Weekly Withdrawal Since August

West Texas Intermediate for November delivery settled at $74.29 a barrel on the New York Mercantile Exchange, the lowest close since Sept. 28.

Brent for December settlement fell 24 cents to $83.91 on the London-based ICE Futures Europe exchange. The global benchmark crude traded at a $9.74 premium to WTI for the same month.

Following U.S. President Donald Trump’s pressure to tame surging prices, Saudi Arabian Crown Prince Mohammed Bin Salman said the world’s top oil exporter is doing its part by pumping near record levels. Saudi output is now at about 10.7 million barrels a day, and the kingdom can add a further 1.3 million “if the market needs that,” he said in an interview.

| Other oil-market news: |

|---|

|

--With assistance from Heesu Lee, Sharon Cho and Grant Smith.

To contact the reporter on this story: Samuel Robinson in New York at srobinson145@bloomberg.net

To contact the editors responsible for this story: Simon Casey at scasey4@bloomberg.net, Joe Carroll, Joe Richter

©2018 Bloomberg L.P.