Debt Rally May Have Run Its Course, India's Oldest Fund Says

The sustainability of gains from bonds is in doubt, given the government might bust its fiscal-deficit target.

(Bloomberg) -- The rally that saw Indian sovereign bonds post their best quarterly gain in four years may have it limits as the central bank is unlikely to embark on a series of interest-rate cuts, according to the nation’s oldest mutual-fund company.

Cheaper oil and a new central bank governor widely seen to have a dovish bent helped local bonds and the rupee rebound from a selloff toward the year-end. The sustainability of those gains is in doubt amid concern that the government may bust its fiscal-deficit target by boosting spending before this year’s national election.

“Markets as usual always price-in moves ahead of the actual events and if you see a rate cut, the market may not rally much further,” said Amandeep Chopra, head of fixed income at UTI Asset Management Co., which oversees about $22 billion. “The best you can expect from the Reserve Bank of India are shallow cuts, not the start of an easing cycle.”

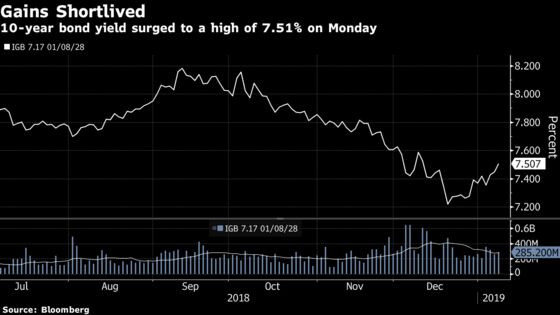

The yield on 2028 bonds, the most traded, hit an eight-month low of 7.21 percent last month as falling oil prices eased worries about inflation in the world’s fastest-growing oil user. The optimism is waning amid reports of the government considering cash handouts to appease farmers -- a key voting block -- before elections due before May.

The yield rose as high as 7.54 percent on Tuesday, extending a 6-basis point gain in the previous session. It is likely to hover in the 7.25-7.50 percent range by end-March, Chopra said.

UTI Asset prefers short-term debt over long-tenor paper because it doesn’t expect the RBI to aggressively ease its monetary policy.

“With an expectation of shallow rate-cut cycle to benign interest-rate outlook, we prefer to be in the liquid segments -- the 5-, 7- and 10-year bonds,” he said. “It’s time to exercise a bit of caution.”

Here are other comments from the interview:

On long-tenor government debt:

- “Going long on the 20-, 30-year government bonds will depend on the longer-term inflation outlook and whether we’re looking at a sustained easing cycle or just a shallow one.”

- “If the RBI cuts rates and renews expectations of one more down the line, then there could be a reason for bonds to rally.”

On company bonds:

- Corporate bonds “will face a bit of a challenge. Barring traditional investors like pension funds and insurers, mutual funds are not so active as they are not adding duration in the current environment.”

On oil prices:

- “Oil remains the joker in the rates outlook. If prices were to jump by $10 dollars, the positivity may need to be reassessed.”

- “You could see range bound markets if oil stays below $56. What helps us is that the average cost of crude would be much lower than what it was in 2018.”

To contact the reporter on this story: Kartik Goyal in Mumbai at kgoyal@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Ravil Shirodkar, Anto Antony

©2019 Bloomberg L.P.