Bonds From India, Philippines Most at Risk Amid Variant Threat

Bonds from India and the Philippines look to be most vulnerable to further economic slowdowns in Asia amid omicron scares.

(Bloomberg) -- Bonds from India and the Philippines look to be most vulnerable to further economic slowdowns in Asia as the threat from a new coronavirus variant revives virus resurgence fears.

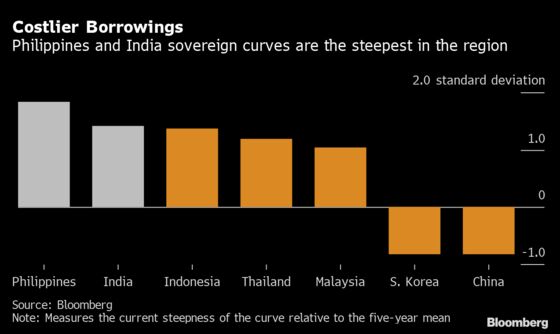

The two nations have the steepest yield curves among seven Asian countries, which means any additional fiscal stimulus would come at a higher cost for the governments. Their scope for monetary easing would also be limited by higher inflation, with lower vaccination rates compounding the stress on their economies.

News on the omicron variant roiled global markets this week as travel bans and doubts about the effectiveness of existing vaccines on the new strain weakened economic recovery bets. Sentiment stabilized as South African health experts, including the doctor who sounded an alarm on the variant, signaled symptoms linked to the strain have been mild so far. Still, investors are watching if results from the World Health Organization’s research on omicron reveal worrying signs.

“In the event omicron turns out worse than the delta strain, India and Philippines may see some deterioration of the fiscal and debt outlook due to weaker government revenues and the need for extended stimulus in 2022,” according to Duncan Tan, a strategist at DBS Bank Ltd. in Singapore. No known cases of omicron have been detected in India and the Philippines so far.

The yield spread between two- and 10-year government bonds from India and Philippines is the widest compared to the five-year average. That’s because India’s borrowing program for the current fiscal year ending March 2022 is already near a record high, while the Philippine budget deficit is at an all-time high this year.

The pressure on Indian bonds may be exacerbated as the central bank ended its announced bond purchase program in the quarter ended September. Rising yields in the Philippines have prompted the government to reject some tenders at auctions in October while auctions in November attracted weak demand.

Inflation Hurdle

Along with fiscal constraints, higher inflation in India and the Philippines could narrow the scope for monetary easing. Philippines has the tightest real policy rate, or nominal policy rate after adjusting for inflation, compared to the five-year average. The nation’s inflation has been mostly hovering above the central bank’s 2%-4% target since January. November inflation figures will be released Dec. 7.

While India’s real policy rate offers a bigger buffer than some of its Asian peers, that gap is expected to shrink as price pressures are seen picking up amid fading base effects and supply-chain constraints. Korea’s real policy rates are tight relative to the historical mean but the central bank’s 50-basis point rate hike since August has created space for future cuts, if needed.

India has the lowest vaccination coverage in the region, with only 32.3% of the population fully inoculated, followed by Philippines at 33.3%, according to data compiled by Bloomberg. Lagging vaccination rates would not only make their economies vulnerable to a resurgence in existing strains but also signal a slower roll-out of potential new vaccines to combat variants.

| Factors | Philippines | India | Indonesia | Thailand | Malaysia | China | S. Korea |

|---|---|---|---|---|---|---|---|

| Yield curve (higher z-score means steeper curve) | 1.83 | 1.44 | 1.37 | 1.22 | 1.03 | -0.79 | -0.75 |

| Real policy rates (higher z-score means more policy buffer) | -1.59 | -0.64 | -0.03 | -1.48 | -1.06 | - | -1.92 |

| Percentage of fully vaccinated | 33.3 | 32.3 | 35.3 | 59.0 | 77.2 | 76.9 | 79.3 |

| Aggregate ranking score | 1.67 | 2.67 | 4.00 | 3.67 | 5.00 | 6.00 | 4.67 |

©2021 Bloomberg L.P.