Bond Demand in Gulf Compared to Stocks Is `Like Mars and Venus'

Bonds Are From Mars and Stocks From Venus for Investors in Gulf

(Bloomberg) -- The Gulf is proving to be fertile ground for debt investors.

Yield-hungry global funds are plowing into regional bonds at the expense of local stock markets, where liquidity has dwindled following the 2014 oil-price crash. The last initial public offering in the United Arab Emirates was in 2017.

Once debt-averse, the petrostates of the Gulf have pivoted to borrowing to plug ballooning budget deficits. They’ve tried to cut capital spending and slash subsidies -- steps that helped shore up finances but spelled trouble for equity investments as austerity undermined consumer spending and credit growth.

“When it comes to looking at bond and equity markets in the Middle East, it is like Mars and Venus,” Richard Lacaille, the chief investment officer at State Street Global Advisors, said in Riyadh. “The interest from bond investors is very clear: they want a little bit of spread, they want diversified assets, and they want liquidity.”

The bond buyer’s Gulf couldn’t be more different from the place shunned by stock pickers for its lack of corporate transparency and market selloffs driven by knee-jerk retail traders. Borrowers in the Gulf Cooperation Council, comprising six monarchies including Saudi Arabia, are now among the biggest issuers in emerging markets, with sales of bonds and Islamic securities tripling in the first four months of this year from 2016.

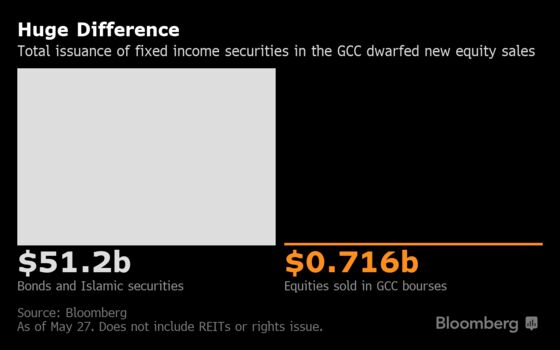

One reason that regional debt is now high on the radar of investors is that Saudi Arabia, Qatar, the U.A.E., Bahrain and Kuwait joined JPMorgan Chase & Co.’s emerging-market bond indexes in January. Governments and companies in the GCC sold $51.2 billion of bonds and Islamic securities this year through May 27, according to data compiled by Bloomberg.

In comparison, the only initial public offerings in the region raised just over $700 million in the same period.

“The emergence of large sovereign issuers and issuances in the past couple of years has also improved the breadth and depth of the debt market,” said Abdul Kadir Hussain, the head of fixed-income asset management at Arqaam Capital Ltd. in Dubai.

When Arqaam Capital’s Hussain moved to Dubai from London in 2006, banks were the main borrowers in a shallow market. Three years later, Dubai just skirted a default after receiving a bailout from fellow emirate Abu Dhabi.

The ranks of borrowers now range from state-run oil giant Aramco, which raised $12 billion in one of the most oversubscribed offerings in history, to Majid Al Futtaim Holding LLC, the Middle East operator of Carrefour SA stores. Recent debut issuers also include Saudi Telecom Co. and dairy-farm operator Almarai Co. Meanwhile, Aramco’s IPO plan has been delayed at least until 2021.

“The ability of the region to survive major high-profile defaults during that period garnered it more attention from international investors,” Hussain said. “The final piece of the puzzle was the inclusion in indexes.”

Brighter Outlook

“We had an environment that was much more conducive for fixed-income investing than equities,” according to Mohieddine Kronfol, chief investment officer for global sukuk and fixed income for Middle East and North Africa at Franklin Templeton Investments. “The equities story is now beginning to improve with a brighter outlook for growth.’’

Non-oil economic growth is bouncing back in the GCC, with the International Monetary Fund projecting a pickup to 2.9% in 2019 and 3.3% next year, the strongest since the crash in crude prices.

But out of about 40 IPOs announced in Gulf markets since the start of 2017, around 75% of the stocks are trading below their offer price, according to data compiled by Bloomberg. Many companies in the Gulf, including the biggest bank in Dubai, have limits on foreign ownership of stocks that make it hard for large international investors to acquire significant stakes.

“While on the equity side one could argue that risks are higher due to liquidity or transparency, on the debt side the region is viewed as having better credit quality in general versus other emerging markets,” said Arqaam Capital’s Hussain. For bonds “to go to the next level we need a more vibrant local-currency market,” he said.

--With assistance from Yasmina Daou.

To contact the reporters on this story: Netty Ismail in Dubai at nismail3@bloomberg.net;Filipe Pacheco in Dubai at fpacheco4@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Paul Abelsky, Alex Nicholson

©2019 Bloomberg L.P.