Bond Traders Just Can’t Wait to Bet on Fed Rate Cuts

Bond Traders Just Can’t Wait to Bet on Fed Rate Cuts

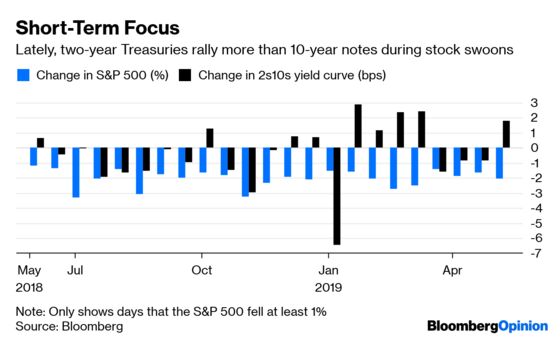

(Bloomberg Opinion) -- The standard playbook for bond traders during periods of market volatility used to be buying 10-year Treasuries. Lately, though, they appear to be taking a more short-term view.

Upon news that China was escalating the trade war with the U.S. by raising tariffs on some American imports, investors flocked first to two-year Treasury notes, pushing those yields down more than 8 basis points to 2.176%. If that holds, it will represent the lowest closing level since February 2018. Yields on 10-year Treasuries, by contrast, fell 7.5 basis points, causing the much-watched yield curve from two to 10 years to steepen.

Curve steepening has been a more unusual pairing with a sharp decline in the S&P 500 Index over the past year, but that’s changed in recent months after Federal Reserve Chair Jerome Powell took a series of abruptly dovish turns. The hot trade is clearly placing bets on when the central bank will cut interest rates. Fed funds futures are now pricing in a full quarter-point reduction by the end of the year and a second by mid-2020, a reversal from just two weeks ago, when Powell made clear that policy makers viewed the economic outlook as solid and low inflation as transitory.

What makes this move all the more drastic is the absolute level of Treasury yields. The lower bound of the target fed funds rate is 2.25%, and two-year yields have closed below that level only three times this year. Barring a big reversal in the coming days, that signals that bond traders are as convinced as ever that the Fed won’t sit back and let the trade war play out before stepping in and easing monetary policy. For some further context, two-year yields are at the same level they were when the Fed’s benchmark lending rate was a full percentage point lower in early 2018.

All this feels like a bit of an overreaction. Of course, in the midst of wide-ranging uncertainty, it’s never an obviously bad decision to purchase two-year Treasuries. In fact, on a nominal total-return basis, that maturity has never lost money in a given calendar year, according to ICE Bank of America Merrill Lynch data going back to 1988. That’s as unblemished of a track record as any asset, and there’s nothing out there in the months ahead that should snap that win streak.

Still, this probably isn’t a momentum trade, judging by how previous rallies of this magnitude have fizzled in the recent past. I wrote in April that bond traders went overboard on their Fed rate-cut bets, and Powell’s stance on inflation earlier this month proved that to be correct. It feels as if they’re getting ahead of themselves again. There’s no doubt that a full-blown U.S.-China trade war is a serious threat to global growth, but the Fed is also likely to be patient and let things develop rather than immediately capitulate to the markets. On Monday, even with an updated view of the trade tensions, Minneapolis Fed President Neel Kashkari said he wasn’t in the rate-cut camp. Vice Chair Richard Clarida reiterated that the U.S. economy is running at or close to the central bank’s twin objectives.

Bond traders are grappling with many different moving parts, including a fresh round of speculation that China will dump some of its $1.1 trillion in U.S. Treasuries in retaliation of President Donald Trump’s latest tariff increase. When it doubt, investors appear to lean into wagers that the Fed will step in to support the financial markets. That may pay off eventually, but only if conditions take a true turn for the worse. The S&P 500 falling to just 5% off its record high doesn’t qualify as such.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.