(Bloomberg Opinion) -- The Federal Reserve this week is holding its second meeting on monetary policy this year, and the topic dominating the conversation in markets is bond-market volatility. Or more precisely, the lack of it. There are many ways to think about this, but one stands out above the rest in a concerning way.

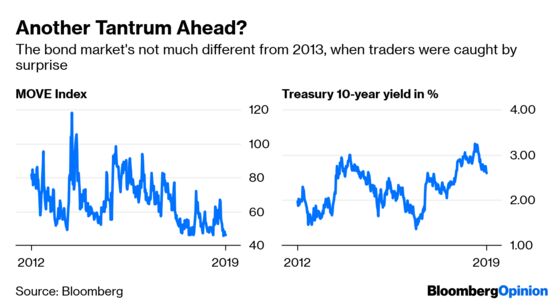

My Bloomberg Opinion colleague Brian Chappatta notes that the all-important 10-year Treasury note’s yield has fluctuated within a 22-basis-point range since early January, narrower than any calendar-year quarter since 1965. On top of that, expected implied volatility as tracked by Bank of America Corp.’s Move Index just fell to its lowest level since 1988. What this implies is that the bond market has reasserted control over the Fed. In other words, the central bank wouldn’t dare send a hawkish surprise and upset markets unless the bond market was prepared for such an outcome, which it isn’t, as evidenced by the drop in volatility and yields. But the Fed under Chairman Jerome Powell has made it clear that it’s independent and doesn’t take orders from anyone or anything, be it the president or the markets. So with longer-term bond yields back at their lowest since January 2017, the stock market having fully recovered from the December sell-off and financial conditions back to being about as loose as anytime in the past five years, it would be easy for the Fed to deliver a message this week that isn’t as dovish as the market expects to stamp out some of the complacency creeping into asset prices. After all, a Bloomberg survey of economists is forecasting a rate hike this year.

Such a move wouldn’t be unprecedented. Recall in 2013 when Fed Chairman Ben S. Bernanke suggested the central bank might soon end its bond-buying program. Bond-market volatility was as low then as it is now, but it spiked on Bernanke’s comments, causing some of biggest losses for fixed-income traders in years. The strategists at JPMorgan aren’t concerned about a volatility spike anytime soon. They wrote in a report that positioning in markets doesn’t match the drop in volatility across many asset classes. They added that the list of potential triggers for higher volatility, including failed U.S.-China trade talks, U.S. auto tariffs on the European Union and a destabilizing spike of Brent crude above $80 a barrel, are mostly low to moderate probability events. Famous last words?

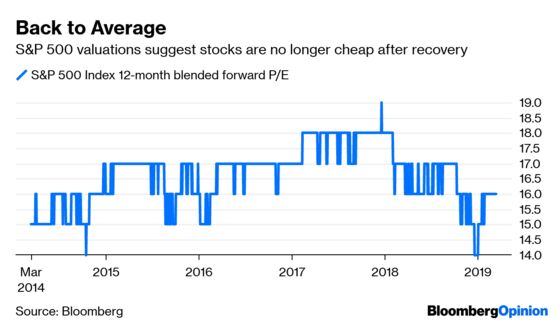

STOCKS ARE BACK TO AVERAGE

Last year, as stocks soared to record highs at the start of October, more than a few talking heads criticized the Fed for being behind the curve and maybe not raising interest rates fast enough to cool an overheating equity market. But the odd thing is, such talk is almost nonexistent even though stock valuations have recovered this year as the S&P 500 Index has rallied to almost within 100 points of a record. Also, inflows into the three biggest exchange-traded funds that track the S&P 500 totaled $11 billion last week, the most since the five days ended Sept. 21. With nearly all members of the benchmark having reported their most recent quarterly earnings, stocks are approaching their five-year average on a blended forward 12-month price-to-earnings ratio basis, according to Bloomberg News’s Sophie Caronello. Those are some remarkable stats given how much the economy is decelerating, with the Federal Reserve Bank of Atlanta’s GDPNow Index, which aims to track growth in real time, having fallen to a “stall speed” level of 0.4 percent.

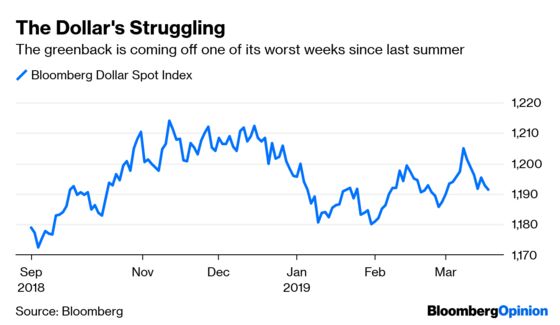

THE DOLLAR EFFECT

U.S. stocks are also getting a strong tailwind from the dollar. The Bloomberg Dollar Spot Index fell on Monday after matching its biggest weekly decline since July in the period ended March 15. S&P Global Ratings figures that 30 percent of the revenue of S&P 500 companies comes from outside the U.S. Jodie Gunzberg, managing director and head of U.S. equities at S&P Dow Jones Indices, calculated that the S&P 500 rises 3.7 times more from a falling dollar than a rising one. So, all else being equal, the drop in the dollar should benefit riskier assets such as stocks. A weaker greenback also gives a boost to emerging markets by damping concern about the ability of borrowers in these economies to pay back the trillions in dollar-denominated debt they have taken out in recent years. The extra yield investors demand to own the dollar-based debt of emerging borrowers instead of Treasuries has shrunk to about 3.45 percentage points from 4.22 percentage points at the beginning of the year, according to a JPMorgan index. At the same time, the MSCI Emerging Markets Index of equities rose on Monday to its highest since August.

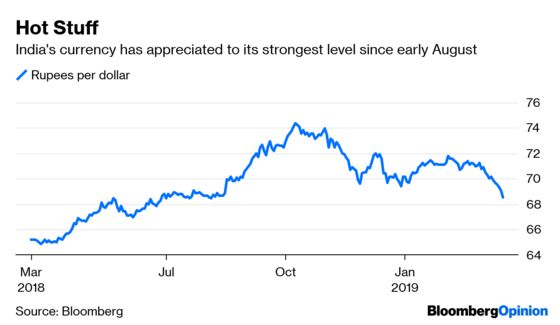

THE RUPEE IS ON FIRE

No currency is as hot right now than India’s rupee. It was the world’s biggest gainer Monday, appreciating 0.82 percent to bring its increase this month to a world-beating 3.23 percent. It’s now the strongest since early August, while a global index of emerging-market currencies from SCI is only at its highest in a couple of weeks. The rupee has received a boost amid a surge of flows into its stocks on optimism that Prime Minister Narendra Modi will be re-elected after recent tensions between India and Pakistan. Investors have poured $2.4 billion into Indian equities this month, taking net foreign purchases to $4.7 billion, the highest in Asia, according to Bloomberg News’s Kartik Goyal. Global funds have raised holdings of rupee-denominated bonds by $833 million this month, according to exchange data. The currency could strengthen further if India is able to convince the keeper of the global MSCI indexes that it’s under-represented in several benchmarks. A team led by Modi’s principal economic adviser Sanjeev Sanyal has been in discussions with MSCI since February to push for higher benchmark weighting for Indian stocks, The Economic Times reported Monday, citing people it didn’t identify.

COPPER’S HEAD FAKE

In February, many of the stocks bulls pointed to the strong rally in copper to suggest the weaker global economic outlook narrative had gone too far. After all, the metal has a reputation for being a great leading indicator for the global economy given its wide use. Well, it turns out the gains in copper had less to do with a bullish economic outlook than it did with a lack of critical supply. As such, the rally has stalled this month and a large amount of metal that had been previously earmarked for withdrawal in depots in the U.S. is being placed back into the LME’s warehousing system, helping to boost the amount of metal available on the bourse to the highest in nearly six months, according to Bloomberg News’s Mark Burton. Canceled warrants, which represent withdrawal orders, fell by 29,725 tons to 45,575 tons on Monday, the largest-ever daily decline in data going back to 1997, according to data from the exchange. “The copper market has gotten used to these types of moves,” Colin Hamilton, the managing director for commodities research at BMO Capital Markets, told Bloomberg News. “There’s no real change to the supply-and-demand balance, and it’s just a case of metal shifting from invisible to visible inventories, and becoming more available to buyers on the LME.”

TEA LEAVES

No, you’re not imagining things. U.S. economic data has been pretty dismal of late. Citigroup Inc.’s economic surprise indexes show that the data has not only been consistently missing estimates since mid-February, but the degree to which the data are missing is the greatest since mid-2017. So when the government releases its factory orders data for January on Tuesday, don’t be surprised if the numbers fall short of forecasts. The median estimate among economists surveyed by Bloomberg is for a gain of 0.3 percent. Although that’s pretty weak, the thing to know is that particular data point has fallen below the estimates for October, November and December. Of course, factory orders aren’t going sway the Fed this week, but it does add to a mosaic of anemic data.

DON’T MISS

A Recession Is Coming, And Maybe a Bear Market: A. Gary Shilling

Bonds Trade Like ’65 After Fed Kills Volatility: Brian Chappatta

Index Funds Don’t Have Much in Common With Libor: Barry Ritholtz

China Banks Have a Hidden Wave of Bad Debt: Christopher Balding

The Shaky Six Cloud the Future for OPEC Oil Cuts: Julian Lee

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.