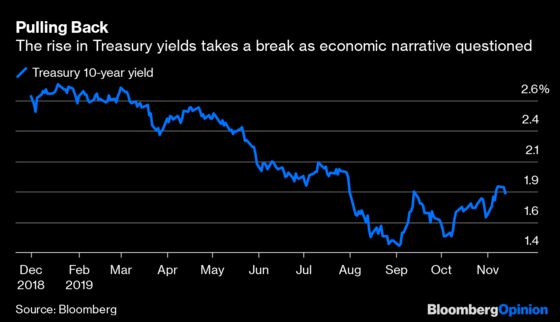

(Bloomberg Opinion) -- The bond market isn’t ready to concede that the economy is on a sustained upturn that will allow it to skirt a severe slowdown or even a recession. U.S. Treasuries followed most of the rest of the global government debt market higher Wednesday, providing a welcome respite from a sell-off that’s looking more like an adjustment of overextended positions than a referendum on faster growth.

Sure, some of the gains in the bond market may be related to doubts about the U.S. and China actually agreeing to the first phase of a trade deal after some downbeat comments by President Donald Trump on Tuesday and subsequent reports of a “snag” on Wednesday. But what hasn’t been discussed as much is evidence that the recent slump in bonds had much to do with the reversal of positions by general investors who bought government debt in August, September and early October as recession speculation peaked. That was borne out in the latest monthly survey of global fund managers by Bank of America released on Tuesday. It showed being long Treasuries is no longer the world’s “most crowded trade,” with 21% of respondents saying so, down from a massive 41% in October. The new “most crowded trade” is long U.S. technology and growth stocks at 39%. And with yields on benchmark 10-year Treasuries having risen from 1.43% in early September to 1.87% on Wednesday, there’s reason to believe that bonds are more fairly valued. In fact, the latest yield is higher than the 1.71% that economists expect it to be at the end of the year and the 1.78% they estimate at the end of the first quarter 2020, according to data compiled by Bloomberg.

Although the data show that the economy both in the U.S and globally may not be getting any worse, that’s far different from showing it’s getting much better and causing central banks to turn hawkish again. “We see the current stance of monetary policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook,” Federal Reserve Chair Jerome Powell told the Congressional Joint Economic Committee on Wednesday in Washington. “However, noteworthy risks to this outlook remain.”

STOCKS HIT A TRADE SNAG

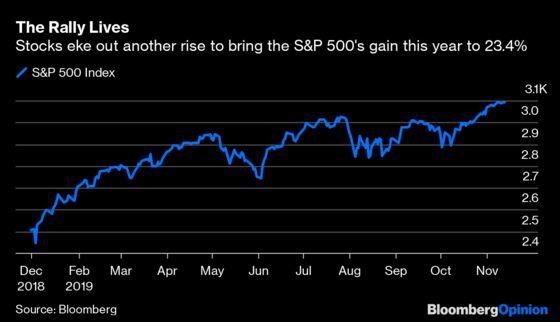

Thanks in part to Powell’s dovish comments, everything was going swimmingly in the stock market until the Wall Street Journal reported that trade talks between the U.S. and China had hit a snag, briefly causing equities to erase their gains. Citing people familiar with the matter, the paper said China is leery of putting a numerical commitment on agriculture purchases in the text of a potential agreement. The development seems to explain why Trump only a day earlier sounded unusually cautious about a trade agreement, saying only that it “could happen soon” and adding that if it didn’t, then he would just increase tariffs on Chinese goods. This is no small matter for the stock market, which has rallied to new highs largely on the notion that a “phase one” deal would be reached, eliminating a significant drag on the global economy. “A couple of weeks ago, it looked like that phase one deal looked all but certain. I think the market started to price in a really positive outcome on the trade side,” Jeff Mills, chief investment officer at Bryn Mawr Trust, told Bloomberg News. “Although I do think that progress is moving in a positive direction, I think it would be foolish for us to assume that we’re going to move completely in a positive direction in trade without any type of intermittent setbacks.” Although equities recovered in late trading, buying stocks in the hopes of a trade deal is proving to be a perilous strategy.

DEFICITS (SOMETIMES) DON’T MATTER

The Bloomberg Dollar Spot Index rose for the seventh time in eight days on Wednesday to its highest in a month even though the U.S. government said its budget deficit widened in October, the first month of the fiscal year, as government spending increased and receipts declined. The shortfall grew about $34 billion, or almost 34%, from the same month last year, to $134.5 billion. This comes after the budget deficit for fiscal 2019 clocked in at just shy of $1 trillion at $984.4 billion. One benefit to having the world’s primary reserve currency is that such deficits don’t exactly matter as much as they would in a place such as Greece. Still, an out-of-control deficit and borrowing could reduce demand for the greenback and U.S. debt at the margins. The upshot is it looks as if the U.S. may not borrow as much as previously estimated to finance the deficit, thanks to recent moves by the Fed to buy Treasury bills to ensure reserves remain abundant. As a result, the strategists at JPMorgan Chase wrote in a report this week that net debt issuance to the public by the U.S. Treasury will be just $720 billion, down from a projected $1.27 trillion in fiscal 2019. That should provide some support to the dollar and, by extension, the U.S. government.

ITALY GETS BYPASSED

One place where the bond rally failed to make an appearance was Italy. Demand slumped to the lowest in 14 months at an auction Wednesday of seven-year notes, even with yields near the highest in three months. That suggests investors prefer countries with slimmer returns but lower credit risk and comes after a recent rise in yields in markets such as Germany and France, weakening Italy’s relative appeal, according to Bloomberg News’s James Hirai. Investors have been cooling toward Italy after political uncertainty and a recent revival in the fortunes of euro-skeptic politician Matteo Salvini. “Peripheral spreads become more vulnerable the higher core yields go as investors switch demand to safer core, semi-core bonds,” Peter Chatwell, head of European rates strategy at Mizuho International, told Bloomberg News. “Higher yields, without a broad based and structural rise in nominal growth, will pose a sustainability risk to Italy’s debt.” With $2.26 trillion of government debt, Italy has more bonds outstanding than all but the U.S., China and Japan, data compiled by Bloomberg show. Italy also has one of the highest debt-to-gross domestic product ratios at 131.5%, compared with 82.3% in the U.S. So when Italy has a poor debt auction, it’s worth paying attention.

HOT COCOA

Chocolate lovers may soon have to dig a little deeper in their pockets to afford their favorite indulgence. Cocoa prices have staged an impressive rally in recent months, approaching an almost 18-month high in New York on Wednesday. The gains come amid speculation that near-term supplies are getting tighter, according to Bloomberg News’s Agnieszka de Sousa. The clearest sign that traders expect tighter supplies can be seen in the prices of so-called nearby contracts, which have moved into a premium compared with later deliveries in a market structure known as backwardation and a sign of tightening supplies. “Traders are blaming the upsurge on concerns about a shortage in the short-term availability of cocoa beans,” Carsten Fritsch, an analyst at Commerzbank AG, said in a note. Still, it’s not clear why short-term supplies should be so tight as shipments in top grower Ivory Coast are still in full swing and higher than a year earlier, he said. There are also some concerns that a new $400-a-ton premium for supplies from West Africa, the world’s top producing region, may affect the way cocoa is traded on the exchanges. The new pricing system could mean that fewer supplies end up getting delivered to warehouses monitored by ICE Futures U.S., driving a rally in the market, according to NickJen Capital Management.

TEA LEAVES

There is a good chance that talk of a global recession could heat up again as soon as Thursday. That’s when Germany — Europe’s largest economy — reports on GDP for the third quarter. The median estimate of economists surveyed by Bloomberg is for a contraction of 0.1%, which would mark a technical recession because the economy shrank by the same amount in the second quarter. But as Bloomberg Economics points out, whether the German economy records the shallowest of recessions or escapes one by the narrowest of margins isn’t important; what’s important is how long the dip will persist.

DON’T MISS

FOMO Doesn’t Cut It as a Buy Signal for Stocks: John Authers

The World Is Being Inundated With Financial Capital: Noah Smith

Jamie Dimon Is Wrong About Negative Rates: Ferdinando Giugliano

The IEA’s New Energy Outlook Comforts No One: Liam Denning

Trump’s Economy Complicates Democrats’ Message: Karl W. Smith

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.