Bond Markets’ Tea Leaves Send Sobering Signal: Trouble Is Ahead

Investors are piling into safety trades with risks growing for world output heading into 2020.

(Bloomberg) -- The world’s biggest government-debt markets are sending a clear signal that global economic growth is stalling and inflation expectations are fading fast.

That sobering message is evident in tumbling yields on Treasuries and German bunds, in bond-market inflation metrics projecting further declines in price pressures and in a gauge that shows investors see no need for extra compensation to load up on long-term debt. The theme was reinforced Thursday as a surprisingly weak reading on the American service industry compounded the angst from reports showing manufacturing already faltering around the globe.

Investors are piling into safety trades with risks growing for world output heading into 2020. Headwinds abound, with the U.S. House having begun an inquiry into impeaching President Donald Trump, the U.K.’s Oct. 31 Brexit deadline approaching and the trade war dragging on. Even another likely Federal Reserve rate cut this month is seen as no panacea.

“The consistent theme seen through the bond markets is that there is higher risk of a bad outcome: a disinflationary scenario with a recession,” said Dennis Debusschere, head of portfolio strategy at Evercore ISI. “Monetary policy is increasingly a weak tool, so with a recession you will run the risk of very low inflation expectations becoming entrenched. There’s a massive move into the deepest and most liquid debt markets.”

That shift is rippling through major debt markets as investors express concern for the economic outlook. Benchmark two-year Treasury yields sank to 1.37% Thursday, the lowest since 2017. It was little changed Friday at 1.39%.

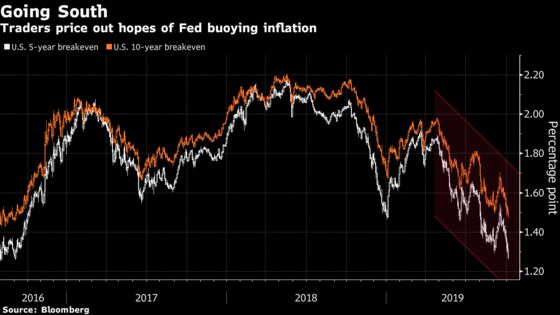

In the U.S. inflation market, 10-year breakeven rates -- a proxy for expectations for the next decade -- tumbled Thursday to 1.47%, the lowest since 2016. They’ve come down from a 2019 high of almost 2% in April.

Fed Chairman Jerome Powell made clear this year that the central bank sees inflation expectations as “the most important driver of actual inflation.” So falling breakeven rates are a concern because they signal the Fed’s stimulus efforts are failing to buoy inflation, let alone achieve its 2% target.

Fed funds futures see a rate cut at this month’s meeting as increasingly likely, with an over 80% probability, compared with under 50% last week. Overall by the end of the year, futures imply about 38 basis points of further easing, with more to come in 2020.

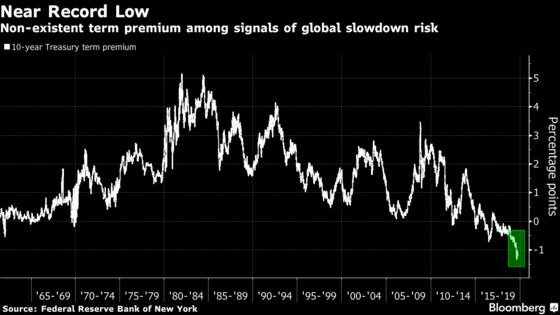

And then there’s the signal from term premium, the compensation investors typically demand to hold longer-term Treasuries rather than rolling over short-dated obligations.

While most agree that the Fed’s trillions of dollars of crisis-era bond purchases siphoned out term premium and helped push it to the current levels near record lows, investors still see it as an ominous sign of economic malaise.

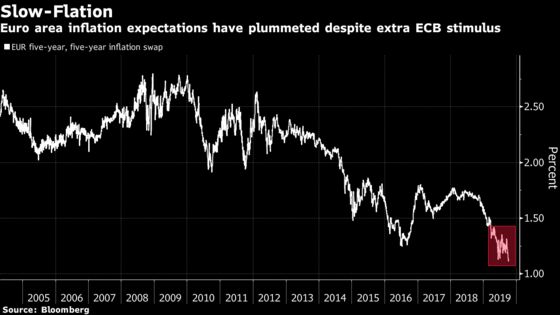

European markets are giving off a similarly gloomy vibe. Long-term proxies of price pressure in the euro zone are slumping: A measure known as the five-year, five-year swap rate, a gauge of inflation expectations for the next decade, is plumbing record lows and raising the specter of deflation.

It’s worrying policy makers. ECB Governing Council member Ignazio Visco said on Thursday the central bank can’t risk losing control of inflation expectations, adding the more serious risk is “deflation in a situation of high public debts.”

With an outlook as grim as that, it might seem that markets have concluded that the European Central Bank was behind the curve and refraining from any supportive action. Yet the ECB cut its policy rate to a record low of minus 0.5% last month and promised more quantitative easing.

Citigroup Inc. has recommended that investors short European inflation via the swaps rate, with a target of 1%. It’s around 1.1%, down from above 1.5% earlier in the year.

While ECB President Mario Draghi is about to leave his post, his successor Christine Lagarde inherits the tough task of getting anywhere near the institution’s goal of inflation just under 2%. It’s no wonder that all sides are pleading with governments to start spending more.

“Other policy areas should really do their job as well,” said Piet Christiansen, a senior euro area analyst at Danske Bank. “The ECB can’t be happy.”

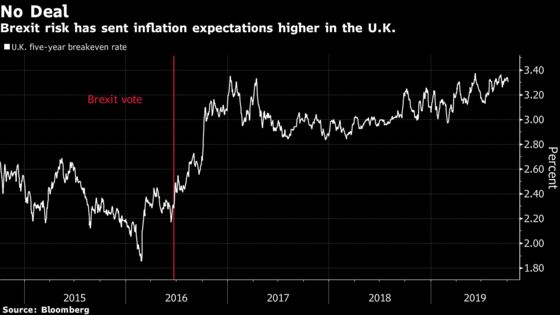

The U.K. is one of the few major economies where inflation expectations aren’t plummeting, and that’s primarily due to one reason: Brexit. The fear of a no-deal Brexit is real among investors, with such an outcome contributing to a slump in the pound to a three-year low and an increase in imported inflation.

The U.K.’s five-year breakeven rate is just off a decade-high of 3.38%. Britain is due to leave the European Union on Oct. 31 unless a deal is reached or an agreement to extend is announced.

So in the global bond market, it seems that for the foreseeable future all roads will lead to the oasis of government debt.

“At a time when we are already concerned about global growth, Brexit adds to the politically influenced reasons for economic slowing,” said Gene Tannuzzo, deputy global head of fixed income at Columbia Threadneedle Investments.

To contact the reporters on this story: Liz Capo McCormick in london at emccormick7@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Paul Dobson at pdobson2@bloomberg.net, Mark Tannenbaum, Anil Varma

©2019 Bloomberg L.P.