Bond Market Debates How to Tame an Unpredictable Yield Curve

Bond Market Debates How to Tame an Unpredictable Yield Curve

(Bloomberg) -- The Treasury yield curve’s uphill sprint has faltered as investors contemplate just how the Federal Reserve might want to check its progress.

Investors are wading into the central bank’s debate over a possible return to the 1940s-era policy of yield-curve control to cap borrowing costs as the economy recovers. Billionaire money manager Jeffrey Gundlach sees rising long-end yields spurring the Fed to action. While most expect a low-yield target for shorter maturities, potentially as soon as September, Societe Generale sees a case for focusing further out the curve. And BlackRock Inc. is skeptical that the Fed will go out on a limb with a specific level until more drastic action looks needed.

How the Fed proceeds is key for investors who have plowed into steepening bets, a move that peaked with last week’s surge in 10- and 30-year yields. Few expect the Fed to unveil anything definitive in its policy statement Wednesday. But all are on the lookout for signs that officials have shifted their focus for Treasuries from market repair amid the pandemic to a longer-term strategy.

“Having that yield-curve control or very supportive forward guidance is a critical component for investors,” said Hamish Pepper, a fixed-income and currency strategist at Harbour Asset Management in Wellington, New Zealand. “Markets need more than just the promise of buying whatever it takes.”

Fed Chair Jerome Powell is likely to field questions Wednesday about how, or whether, the central bank could put a ceiling on yields as the government unleashes spending to avert a lengthy recession.

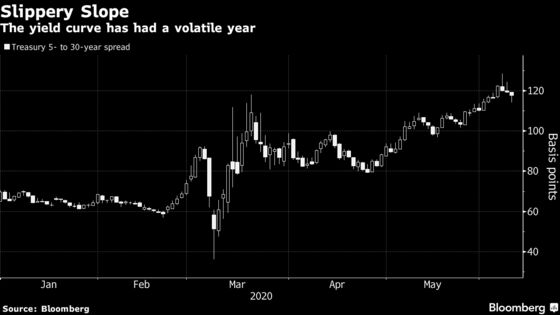

Ten-year Treasury yields, a benchmark for global borrowing, touched 0.96% last week, the highest since mid-March, before falling to just above 0.8% as the rally in stocks lost steam. Yields on the long bond have dipped back after reaching the highest since 2016 relative to 5-year rates.

Different versions of curve control appear to be in play: The Reserve Bank of Australia pinned its three-year yield at 0.25% in March, while the Bank of Japan has tethered the 10-year around zero since 2016. India’s central bank is taking less explicit steps to contain long-end yields, analysts say, with asset-purchases similar to the Fed’s Operation Twist.

Short End

The strategy of targeting the short end is seen as the likeliest approach for the U.S., in part because it’s the easiest segment of the curve for the Fed to control. It would also send a strong signal that the Fed intends to keep short rates low.

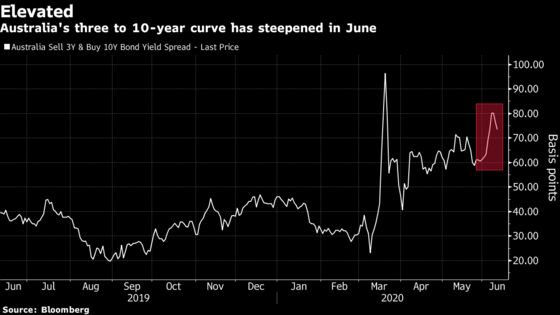

In Australia, the 3- to 10-year curve has steepened almost 20 basis points this month, which should draw buyers to the longer maturity.

“The safest trade you can come up with is to buy five- to six-year bonds,” said Chris Rands, a money manager at Nikko Asset Management Ltd. in Sydney. “In two years’ time, you’ll have a three-year bond and the RBA could be pinning it to 0.25%.”

How this strategy would translate to the U.S. is another question. But Fed Governor Lael Brainard has favored a similar approach, stressing the benefits of forward guidance and interest-rate caps on short-term securities.

Long End

The Fed’s focus may be wasted on the front end, says Subadra Rajappa, head of U.S. rates strategy at SocGen. She notes that forward guidance and asset purchases kept these rates close to the Fed target for years after the global financial crisis. And the Fed is unlikely to leap to yield-curve control before exhausting its more-familiar tools.

The 10-year is both more variable and a more relevant rate to the real economy. And this section of the curve is under supply pressure as the government boosts long-term issuance to records. A measure of demand at Tuesday’s 10-year auction was the lowest since August.

Rajappa’s point looks stronger after last week’s Treasuries sell-off. She has backed the steepening trend since March, when “everybody laughed us out of the room” because the Fed was buying $75 billion of Treasuries a day, an amount that has dwindled to $4 billion. The steepening move still has room to run, she says.

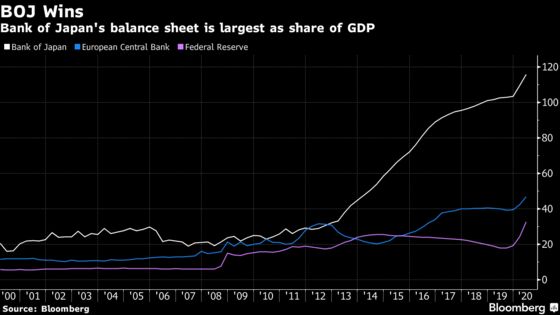

Japanese-style curve control isn’t an obvious model for the Fed. It’s fallen well short of the original aim to return inflation to the 2% target. What the policy has achieved is allowing the Bank of Japan to scale back its massive asset-purchase program -- at least before the pandemic.

As Mitsubishi UFJ Kokusai Asset Management Co.’s Akio Kato points out, the BOJ already owns a lot of the market, and it had also held front-end rates below zero. The Fed has made clear that’s not a path it wants to take.

“The BOJ can keep the grip as it holds some 40% of Japanese government bonds,” said the general manager of strategic research and investment. “The grip of the Federal Reserve may not be as strong initially.”

Flexibility

While it may frustrate investors, there’s an argument for the Fed to maintain ambiguity around its asset purchases. BlackRock’s Bob Miller sees the central bank preserving its policy ammunition for as long as it can until the path of economic reopening becomes clearer.

Should the recovery progress relatively smoothly -- a hope but not an expectation, by Miller’s reckoning -- the Fed is likely to welcome an orderly rise in yields. This is the scenario in which a measured climb doesn’t spook stocks or spark broader market volatility.

“That healthy type of increase in interest rates won’t tighten financial conditions, because equity risk premium will be coming down more rapidly than rates are going up,” said Miller, head of Americas fundamental fixed income.

©2020 Bloomberg L.P.