Quants Ditch Treasuries Amid Battle Over How High Yields Can Go

Bond Market Debates How High Reflation Trade Can Boost Yields

(Bloomberg) -- With Democrats poised to take control of Congress and the White House, Treasury yields look set to climb, leaving bond traders trying to figure out just how high they might go.

That’s the key question after the results of the Georgia Senate runoffs on Wednesday triggered a long-awaited breach of the 1% level on the 10-year note. While many expect yields to edge up just a few basis points, more aggressive calls see rates climbing as high as 2% in short order. Quantitative hedge funds are busy liquidating loss-making bets on Treasuries and could begin to establish new short positions if the 10-year yield breaches 1.10%, according to market participants.

Momentum funds known as Commodity Trading Advisors likely drove the initial move upward in yields on Wednesday, based on activity in futures markets, Citigroup Inc.’s Edward Acton wrote in a note to clients. The funds have been cutting losses since 10-year yields reached around 1.02%, said Nomura Holdings Inc.’s Masanari Takada.

Fed Response

For months, investors have speculated that the Federal Reserve would act to prevent an unruly climb in yields from crimping the economic rebound. That potential action, a reliable bid from international investors, and the backdrop of surging virus cases have so far kept yields in check. But now, with the prospect for additional government stimulus spurring optimism on growth, a gradual climb in yields may prove more palatable to the Fed.

“As long as inflation expectations are driving the increase in the 10-year yield, we can continue to go up from here and the Fed is not going to change that,” said Gregory Staples, head of fixed income at DWS Investment Management, which oversaw about $800 billion globally as of last year.

The benchmark 10-year yield has already more than tripled from its record low set amid the market chaos of March. It was around 1.08% in New York trading Thursday.

Bloomberg Intelligence sees 1.17% as a target, while others are looking at the March high of about 1.27%. Mizuho Bank Ltd’s Vishnu Varathan sees a 1.5% to 2% range as possible.

Jobs in Focus

Friday’s U.S. labor data could prove a near-term catalyst -- particularly if it’s bad, according to DWS’s Staples. While a weak report in normal circumstances might push yields lower, a net loss of jobs this time could add to the momentum for more fiscal stimulus. Financial markets are factoring in $750 billion to $1 trillion of additional spending and a bad jobs report could lead to a break to the 1.09%-1.12% area in yields, Staples said.

He’s underweight 10- and 30-year Treasuries and sees potential for the curve to steepen further. Staples describes himself as “more cautious” on the long end, which will be prone to more swings because shorter maturities are anchored by the Fed’s low-rate pledge.

JPMorgan Chase & Co. strategists estimate that yields tend to rise by 15-20 basis points for each 1 percentage point gain in consensus growth expectations.

Should 10-year yields get ahead of growth expectations, some investors have said it could spark a domino effect across asset classes.

CTA funds “appear likely to keep closing out long positions with yields at 1.02% or higher,” Nomura’s Takada wrote in a note Thursday. “We cannot rule out the possibility that CTAs could turn short” at yields of 1.10% or higher, he said, but noted a significant selloff in bonds driving benchmark yields well above that level would likely need a marked shift in investor sentiment.

The Fed is now buying about $80 billion a month of Treasuries. The minutes of its last meeting, released Wednesday, showed officials unanimously backed holding the pace of asset purchases steady, although a couple indicated they were open to weighting purchases toward longer maturities.

As for December’s jobs report, the median forecast is for a net gain of about 50,000 nonfarm jobs, which would be the weakest since April’s massive decline. Data Wednesday showed the number of employees at U.S. businesses unexpectedly dropped in December.

Inflation Expectations

A key measure of the yield curve is the widest in four years. And the 10-year breakeven rate, a proxy for expected inflation over the coming decade, is the highest since 2018. It climbed above 2% this week for the first time since 2018 against the backdrop of the post-Brexit trade deal, the approval of additional virus-relief aid in the U.S., and the roll-out of vaccinations.

The breakeven rate extended its climb Thursday, reaching 2.1%, after a report showed growth at U.S. service providers unexpectedly accelerated in December.

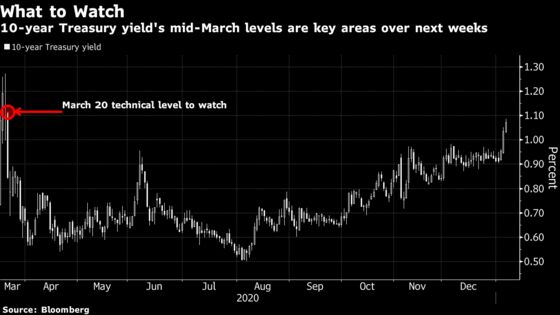

BMO Capital Markets strategist Ben Jeffery says the next technical levels to watch in the 10-year rate over the next couple of weeks are 1.11% to 1.14%, opening gaps formed in March, along with 1.27%, the intraday high on March 19. Those are the levels in which buying interest emerged at the time, and the yield began its downward trajectory to as low as 0.54% over the following month or so.

Whether the Fed chooses to step in or not to contain long-end rates “will really be a function of how financial conditions perform,” Jeffery said. “As long as financial conditions remain easy, the Fed will be content to be patient. But a pickup in volatility will inspire a bit more urgency from policy makers.”

©2021 Bloomberg L.P.