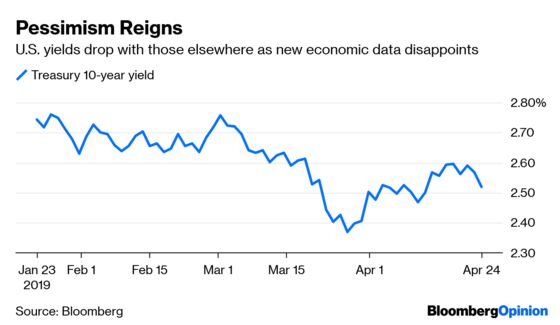

(Bloomberg Opinion) -- It’s been a rough few weeks for the global government bond market. Yields as measured by the Bloomberg Barclays Global Aggregate Treasuries Index have risen from this year’s low of 1.15 percent in late March to 1.27 percent on Tuesday. The rise came as investors embraced a new narrative, which is that perhaps the global economic outlook isn’t as bad as thought earlier in the year. As a result, investors doubled down on riskier assets, pushing the S&P 500 Index to a record on Tuesday and equities globally to within 1 percent of an all-time high. But on Wednesday, the bond market made clear that it’s too soon to sound the all-clear.

In a sign of just how pessimistic the bond market is on the economic outlook, government bonds globally rallied unusually hard after a small miss in a second-tier German economic report on business sentiment, with yields on that nation’s 10-year bonds dropping back below zero. Bond yields throughout the euro zone fell as well. In the U.S., 10-year yields declined the most in a month, and the Treasury Department’s auction of $41 billion in five-year notes generated above-average demand. “There is still this underlying sense of eternal pessimism in the market,” Thomas Simons, senior money markets economist at Jefferies LLC, told Bloomberg News. “Any time there’s even a sniff of a recession sign, it’s latched onto as the base-case scenario.” That’s not to say other factors didn’t contribute to the rally in bonds. It helped that a report in Australia showed inflation slowed sharply in the first three months of the year, reinforcing the notion that consumer prices are in check globally. Then there’s the Bank of Canada, long considered the most hawkish major central bank in the world. On Wednesday, it dropped its long-held bias for more interest-rate increases, in part citing a global slowdown. The move was a mild surprise given how energy prices have rebounded in what should be a net benefit to Canada’s largely oil-dependent economy.

These are not isolated events. To Medley Global Macro Managing Director Ben Emons, they are all a byproduct of the U.S.-induced slowdown in global trade, which data compiled by Bloomberg show has dropped to its lowest since 2009. Emons pointed out in a research note that in Australia alone, tradeable goods CPI has gone from rising 0.8 percent quarter-over-quarter to falling 0.6 percent. In fact, tradeable goods deflation globally has gone from rising 3.7 percent on average in 2018 to falling below 1 percent in the first quarter. Nothing scares bond traders more than inflation, but right now the global economy is too soft to produce anything worth getting nervous about.

THE DOLLAR GAINS TRACTION

Bonds, or at least U.S. Treasuries, also seem to be getting a boost from a stronger greenback. The Bloomberg Dollar Spot Index reached a new high for the year on Wednesday, rising as much as 0.71 percent. Its two-day gain of 1 percent is the most since August. For bond traders, a rising dollar has two main benefits. First, it has the potential to act as a drag on the economy by making American-made goods less competitive. Second, it makes foreign goods relatively cheap, thereby helping to put a lid on inflation. Consider that the government is forecast to say Thursday that the core personal consumption expenditure index, which is the Federal Reserve’s favored measure of inflation, rose just 1.3 percent in the first quarter, matching its smallest increase since 2015. That’s important because the bond market increasingly believes that a slowdown in inflation may prompt the Fed to cut rates later this year. “I think the answer has to be yes,” Chicago Fed President Charles Evans said this month when asked whether low inflation could be grounds for a cut. “If core inflation were to move down to, let’s just say, 1.5 percent,” that would indicate the current level of rates “is actually restrictive in holding back inflation, and so that would naturally call for a lower funds rate, at least so that it was accommodative.”

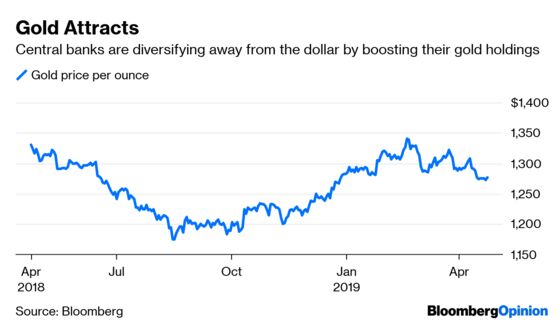

CENTRAL BANKS GORGE ON GOLD

In one way, the dollar is fighting an uphill battle. There’s growing evidence that some major central banks are scooping up gold to reduce the percentage of dollars in their foreign-exchange reserves. China raised reserves to 60.62 million ounces in March, or by 11.2 tons, from 60.26 million a month earlier, according to data on its website. Should China continue to accumulate bullion at the rate it did in the first quarter for the rest of 2019, it may end the year as the top buyer after Russia, which added 274 tons in 2018, according to Bloomberg News’s Ranjeetha Pakiam. India may purchase 1.5 million ounces in 2019, or about 46.7 tons, according to Bloomberg News, citing Howie Lee, an economist at Oversea-Chinese Banking. India increased its stash by about 42 tons last year, and after adding more in January and February, the country’s gold reserves now stand at a record of almost 609 tons, data from the International Monetary Fund show. Global official sector gold purchases could reach 700 tons in 2019, according to Citigroup. Heightened geopolitical and economic uncertainty have pushed central banks to diversify their reserves and focus on investing in safe and liquid assets. Governments worldwide added 651.5 tons of bullion last year — the second-highest total of purchases on record, Bloomberg News reports, citing the World Gold Council. Further inflows should support gold prices, according to Goldman Sachs.

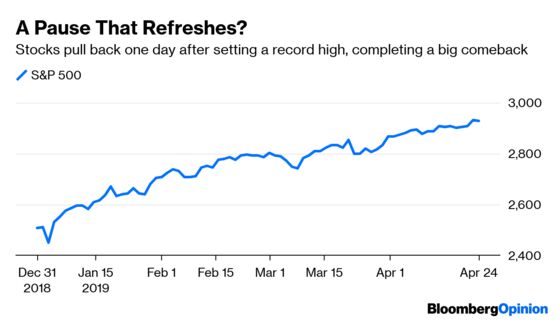

STOCKS TAKE A BREATHER

The U.S. stock market was unable to follow through on its gains from Tuesday that sent the S&P 500 to a record high, ending down 0.22 percent. That’s understandable. Investors surely want to step back, take a breath and figure out their next steps. One thing to note is that at Tuesday’s closing level of 2.933.68, the S&P 500 was only about 0.5 percent away from the median year-end target of 2,950 based on a survey of about 25 Wall Street strategists by Bloomberg News. The good news is that strategists are 1) notoriously behind the curve, and 2) generally paid to be optimists. In other words, a big part of their job is to drum up support for stocks so clients feel compelled to increase their trading activity. So, in that sense, expect a slew of higher S&P 500 forecasts in the coming days that should help lift, or least support, equities. Nevertheless, the S&P 500 is up 16.8 percent this year, and history shows that for the 11 times since 1933 that the benchmark had rallied more than 15 percent through April, gains tended to stall in the final eight months of the year. There’s also the earnings picture to consider. Profit growth is nonexistent at the moment, but earnings are forecast to rise 8.7 percent in the last three months of 2019, which should help companies show a small increase for the year. But Wall Street has a near- perfect record of overestimating earnings, according to Bloomberg News’s Sarah Ponczek and Vildana Hajric. Full-year earnings estimates normally drop by about half a percentage point each month, according to research firm Quanitative Management Associates, which would wipe out any earnings increases for the year if history holds.

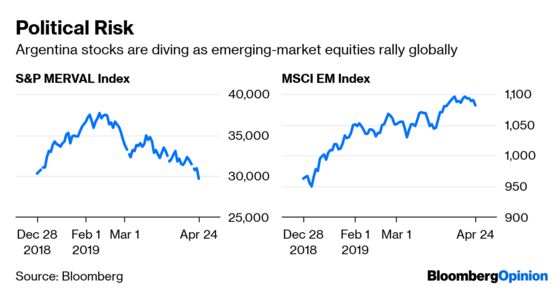

ARGENTINA’S IN FREEFALL

Trying not to peek at what’s happening in Argentina’s financial markets these days is like trying not to look at a car crash — you know you should look away, but you just can’t. Argentina’s stock market and currency both plunged more than 3 percent on Wednesday. The peso is now down more than 14 percent for the year while the benchmark S&P Merval Index of equities is at a new low for the year. As for Argentina’s bond market, yields are the highest since the nation was last in default. The latest weakness comes as polls show President Mauricio Macri, once seen as Argentina’s economic savior when he was elected in 2015, in a dead heat with his populist predecessor Cristina Fernandez de Kirchner. Investors clearly doubt Macri can fend off the electoral challenge while taming inflation of almost 55 percent. And while Argentina hasn’t enjoyed the economic renaissance many expected when he was elected, Kirchner’s policies of tax and spend share some blame for the subsequent economic crisis, according to Bloomberg News’s Pablo Gonzalez. “It clearly seems the election is slipping away from Macri,” Alberto Ramos, head of Latin America research at Goldman Sachs, told Bloomberg News. “There’s increasingly less guarantee that policy continuity will be maintained after the election, and that makes markets nervous.”

TEA LEAVES

If the definition of insanity is doing the same thing again and again and expecting different results, then the Bank of Japan qualifies as insane. In a few hours, the central bank will release new forecasts that are expected to show Japan will again fall short of its inflation target after nine years of unprecedented stimulus. Maybe it’s time to try something different than keeping benchmark interest rates below zero and buying bonds and exchange-traded funds? Economists predict the fiscal 2021 price forecast will be 0.8 percent, the BOJ’s lowest new projection looking two years into the future since Haruhiko Kuroda took the helm of the central bank in 2013 and promised 2 percent inflation in about two years, according to Bloomberg News’s Toru Fujioka. The central bank is also likely to consider trimming some of its growth projections to reflect weaker output and export data, according to people familiar with the matter. Should Kuroda express pessimism over Japan’s economic strength, speculation may rise that the BOJ’s next policy move will be further easing should growth and inflation buckle after a planned sales tax hike later in the year, Fujioka reports.

DON’T MISS

Stocks at Record Highs Hold a Lot of Appeal: Charles Lieberman

Trump Can’t Easily Break the Federal Reserve: Bill Dudley

The Crisis Risk at the ECB Is All Too Real: Ferdinando Giugliano

Junk Bonds Vex Portfolios, But Investors Love Them: Nir Kaissar

Soak the Boomers in Order to Save Capitalism: Karl W. Smith

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.