Bond Investors Are Daring to Whisper About a Return to Fed QE

Bond Investors Are Daring to Whisper About a Return to Fed QE

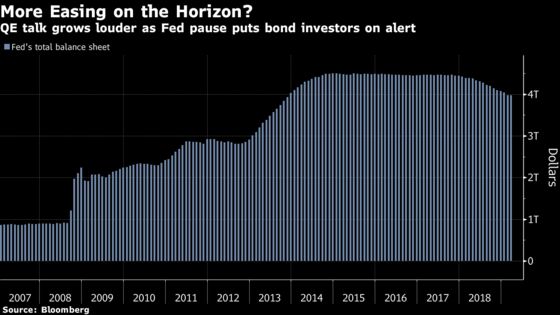

(Bloomberg) -- Bond-fund managers are starting to whisper about the prospect of more Federal Reserve quantitative easing to fight the next U.S. downturn, underscoring just how acute concerns over flagging global growth have become less than three months after the central bank last raised interest rates.

Gene Tannuzzo at Columbia Threadneedle says the likelihood the Fed resumes bond buying in 2020 is increasing as a rising tide of risks prompt monetary officials the world over to pivot toward more accommodative policy. Thomas Atteberry of First Pacific Advisors sees the next U.S. recession occurring in one to two years, and is positioning for the return of QE by moving into three- and four-year Treasuries, as well as mortgage pools with 10- to 15-year amortizations.

Traders of shorter-maturity debt already see lower rates as the most likely policy path for 2020. And with the fed funds target currently being held at a range of 2.25 to 2.5 percent, officials won’t have nearly the conventional firepower at their disposal as in the past to combat a downturn in the economy, a growing chorus of investors warns. San Francisco Fed President Mary Daly even suggested last month that faced with another slowdown, the central bank may want to use asset purchases “more readily,” not just as a last-ditch measure.

“The global picture continues to be quite concerning,” Tannuzzo, who manages the $4.5 billion Columbia Strategic Income Fund, said from Minneapolis. “Europe might be on the edge of recession now, and China has had the slowest growth in a decade. If that continues, there will certainly be an impact to the U.S. economy and we could possibly see QE in 2020.”

An abysmal U.S. jobs report Friday capped a week of disappointing data and dovish rhetoric from central banks across the globe. The European Central Bank lowered its growth forecasts Thursday, a day after the Bank of Canada dialed back its expectations for policy tightening. The Organisation for Economic Co-operation and Development cut its global outlook earlier this week, while China downgraded its goal for economic expansion.

The developments come on the heels of a dramatic shift in the Fed’s interest-rate outlook in recent months, pivoting from predictions of two more rate hikes this year as recently as December, to preaching an abundance of caution around the path of future policy.

A new round of QE could be deployed more quickly and on a larger scale than before, given U.S. policy makers’ familiarity with bond-buying initiatives, Tannuzzo said. He envisions any future program largely resembling the third round of post-crisis quantitative easing initiated in 2012, which involved $85 billion of monthly purchases of Treasuries and mortgage-backed securities.

This time the Fed could add up to $100 billion a month of Treasuries, agency debt and possibly even corporate bonds to its already inflated balance sheet, he said. Any initial widening of credit spreads as economic conditions deteriorate would give way to a rally in corporate bonds as the Fed steps in, he added.

“Our base case is for the U.S. to avoid recession,” Tannuzzo said. “But in order for that to happen, we would need to see stabilization in growth outside the U.S. in the first half, or the U.S. will be dragged closer to recession.”

Meanwhile, Columbia Threadneedle has reduced its exposure to emerging-market and high-yield debt as it takes a more conservative approach to asset allocation.

Policy Review

As the Fed embarks this year on a comprehensive review of the way it conducts policy, one idea officials are discussing would be whether to utilize asset purchases as a more routine part of how it guides the economy -- rather than solely when there are no other options on the table.

While the central bank would likely cut the fed funds target first in the face of economic deterioration, policy makers could potentially lower rates and execute QE simultaneously, according to Atteberry. On Thursday, Fed Governor Lael Brainard said officials intend to “use only one tool actively at a time,” and that they prefer the benchmark rate when it’s still above zero.

“There’s no chance of avoiding a recession, so there’s probably no chance of avoiding QE,” said Atteberry, who manages $6.9 billion in assets. He said that the next downturn will likely be a “credit-driven event.”

Policy makers may be more active in the front end of the Treasuries market the next go around in order to steepen the curve, he said, or they may use the long end to “help the triple-B corporate sector, which could be having financial stress.”

‘Too Soon’

Money-market traders are pricing in slightly more than one full Fed rate cut over the next two years, overnight index swap pricing shows. Still for many that’s a long way from QE.

Another round of quantitative easing is “possible of course, but it’s too soon to be talking about and not something that investors should be relying on as a guide to their allocations,” said Tad Rivelle, chief investment officer for fixed income at TCW Group Inc., which manages $190 billion. “The Fed’s toolbox is not all powerful, and doesn’t have the capacity to fix underlying problems, such as excess leverage.”

The Fed will still have the capacity to cut rates first in the face of any economic deterioration, especially given there may be at least one more hike left by year-end, according to Gautam Khanna, a senior fund manager at Insight Investment, which manages about $787 billion.

At the same time, “there is growing acceptance of QE as a legitimate part of the Fed’s toolkit, and it certainly will be on the table as an option as needed,” he said via email.

Khanna, who sees a realistic possibility of a recession in two to three years, would expect the Fed to avoid rushing back into mortgage securities given the housing market likely won’t be the epicenter of the next downturn. He also said the central bank could potentially try to tie bond purchases to economic objectives, such as U.S. unemployment reaching a certain threshold.

“The use of the Fed balance sheet is fair game as a policy tool,” he said.

--With assistance from Jeanna Smialek.

To contact the reporter on this story: Vivien Lou Chen in San Francisco at vchen1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.