Bond-Hungry Investors Hand U.K.’s Sunak License to Spend

Bond-Hungry Investors Hand U.K.’s Sunak License to Spend

(Bloomberg) -- For all the pressure on U.K. Chancellor of the Exchequer Rishi Sunak to explain how he’ll repair public finances ravaged by the coronavirus, investors are lending the money with very few questions.

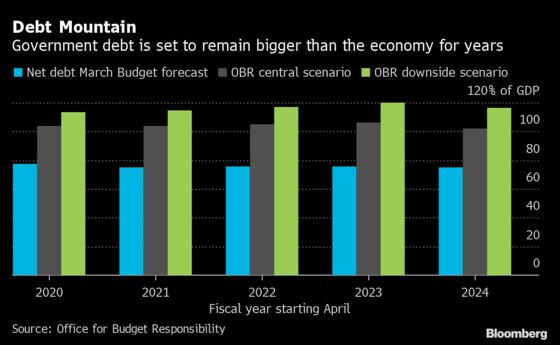

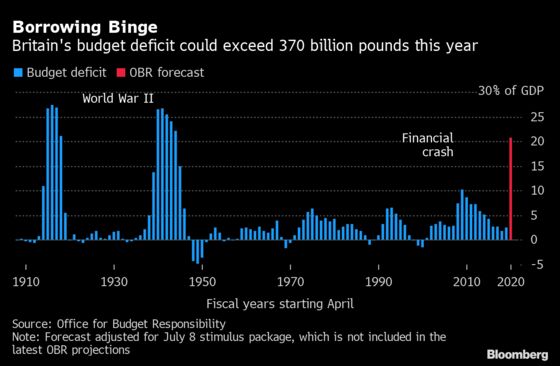

In a week that saw Britain’s fiscal watchdog predict that the budget deficit this year could soar to the highest level during peacetime, government borrowing costs fell closer to record lows. The Office of Budget Responsibility also said the national debt, which has exceeded 100% of economic output for the first time in more than half a century, could stay at that level for the next five years.

There was a time when a fiscal outlook nowhere near as bad would have caused an upheaval in the market by so-called bond vigilantes, who punished profligate politicians by charging more to lend them.

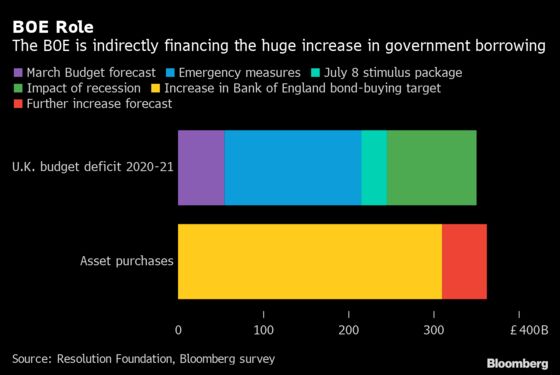

But the angst is somehow lost on bond investors. In fact, yields fell on Thursday even after the Debt Management Office ramped up its bond sale plan by another 110 billion pounds ($138 billion.) A big player in all this is the Bank of England, which is hoovering up debt and keeping interest rates at a record low, a situation that may not change for some time.

The following charts explain the fiscal outlook, why demand for bonds remains strong and the risks ahead.

At almost 2 trillion pounds and rising, the stock of government debt is high. Yet the cost of servicing it amounted to around 4% of total revenue in 2019-20, well below a target set before the crisis. That’s not just because yields are falling, but because around a quarter of all gilts are now held by the BOE.

“The debt-interest rate dog is not barking particularly loudly but we need to be alert,” OBR Chairman Robert Chote said Tuesday.

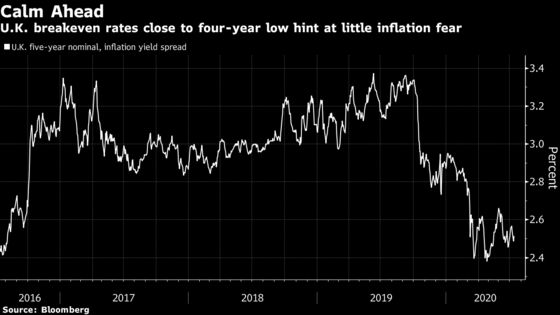

What makes it relatively easy for the BOE to maintain loose policy, which includes a benchmark rate of just 0.1%, is low inflation. In fact, while some argue that the surge in spending could cause prices to increase, most central bankers and economists worry about the risk of deflation. That’s not to say it’s safe to assume the current outlook won’t change.

“Everything is pretty well aligned precisely because inflation has fallen a lot,” said Oliver Harvey, macro strategist at Deutsche Bank AG. If that changes down the line, “there may be a tension between the need of the government to keep interest rates relatively low and monetary policy goals,” he said.

The central bank has increased its asset-purchase target by 300 billion pounds since March, covering all of the projected increase in the budget deficit. Economists forecast that it will add another 50 billion pounds by the end of the year.

The BOE expects to carry out purchases at a slower pace in the second half, though says it’s ready to ramp up again if necessary.

Most gilts are held by overseas investors as well as domestic insurance companies and pension funds. Demand from these quarters has remained solid over more than a decade that has included the financial crisis, Brexit and now the Covid-19 turmoil. Pension funds seeking an income stream to match their liabilities have been eager buyers of long-dated bonds.

Right now, gilts are benefiting from their reputation as a haven asset. Fiscal deficits are blowing across the developed world and yields in many countries are now negative, meaning an investor holding the debt to maturity is guaranteed to lose money.

But the scale of the government’s borrowing is unsettling to anyone who associates high levels of debt with financial ruin. Britain now owes more as a share of the economy than at any time since Harold Macmillan was prime minister, the Profumo scandal gripped the nation and The Beatles released their first album.

The vast cost of direct of support may prove a one-time expense, but the loss of tax revenue and increased welfare spending caused by the slump now engulfing Britain is likely to persist.

“It’s going to take decades before we manage that debt back down to the levels we were used to pre this crisis,” said Carl Emmerson, deputy director of the Institute for Fiscal Studies.

The U.K. and many other advanced economies tolerated high levels of debts following World War II. That was partly done by allowing economic growth and inflation to bring down the crucial debt-to-GDP ratio over decades. That might not be easy this time because about a third of the debt is indexed to retail prices, according to Richard Hughes, the Treasury’s preferred candidate to succeed Chote as head of the OBR. He described as the prospect of inflating the debt away as “idle chat.”

©2020 Bloomberg L.P.