Bond Bears Popping Champagne Say U.S. Yields Have Room to Rise

The bond selloff deepened after data on U.S. private-sector jobs bolstered the case for the Fed to keep raising rates into 2019.

(Bloomberg) -- A week after Treasuries mysteriously rallied in the wake of the Federal Reserve lifting its long-term interest-rate forecast, short sellers in the $15 trillion market have reason to celebrate.

The bond selloff deepened Thursday after data Wednesday on U.S. private-sector jobs bolstered the case for the Fed to keep raising rates into 2019, sending 10-year notes down the most in more than a year. Thirty-year Treasury yields pushed above the 3.25 percent level that fixed-income veteran Jeffrey Gundlach identified as a “game changer.”

“Solid data releases, higher oil prices and a technical backdrop that suggests there are not a lot of obstacles for yields to continue to push higher will have many wondering how far this new push higher can go,” said Rodrigo Catril, a Sydney-based strategist at National Australia Bank Ltd.

With an American economy in good shape and equity prices flirting with record highs, 10-year yields appear to be breaking out of the range of about 2.8 percent to 3.1 percent that’s lasted for months. Next up on the potential-catalyst list is Friday’s payrolls report, which gets even more focus given the emphasis Fed officials are placing on data.

Short sellers were already positioned for more pain in the Treasury market. Speculative net short positions on 10-year notes climbed to a record, the most recent Commodity Futures Trading Commission data showed. An update to those figures comes Friday.

“In hindsight we wish we were even shorter on U.S. rates,” said Raymond Lee, a fund manager at Kapstream Capital Pty in Sydney. “My view was that U.S. yields were going to go up -- maybe to 3.25 percent -- but I didn’t think it would be this quick.”

Ten-year yields reached as high as 3.23 percent on Thursday, handily above the peak in May, and the highest since 2011. It’s also above where most analysts had expected them to end the year, with the median estimate at 3.10 percent in a Bloomberg survey. The rate was 3.18 percent as of 10:37 a.m. in New York.

Read our research roundup of U.S. rates strategists’ views

Aside from data, there’s another dynamic at work: the Fed’s accelerating reduction of its balance sheet. It’s now letting $50 billion a month of its bond portfolio run off without replacement. Along with an escalation in U.S. borrowing requirements -- the federal deficit hit $898 billion in the 11 months through August -- that’s a lot more supply to digest.

“That gradual withdrawal of liquidity is causing yields to rise,” Bob Baur, chief global economist at Principal Global Investors, said in an interview with Bloomberg Television in Tokyo Thursday. “We look for 10-year Treasury yields to hit 3.5 percent at some point -- later this year, early next year -- and I think that’s going to be a real problem for stock markets.”

Others, including Macquarie Group Ltd.’s Viktor Shvets, say ballooning debt levels will keep a lid on yields. “Yields will have to stay very low, primarily because we’re overleveraged,” Shvets, the bank’s head of Asian strategy, told Bloomberg TV in Hong Kong. “There’s just too much debt in the global economy.”

Back on Sept. 19, Gundlach said two closes above 3.25 percent on 30-year bond yields would mark a significant milestone. The Thursday session could be key, for him at least, after the Wednesday close at almost 3.34 percent.

Another reason yields might trend higher is market-based measures of inflation have been steady for most of this year, according to Greg Gibbs. That suggests investors don’t see inflation exceeding Fed officials’ 2 percent target on average over the next decade, even as commodity prices climb and wage pressures build.

“The fact that they haven’t risen yet may point to further upside risk for yields,” said Gibbs, founder of Amplifying Global FX Capital Pty. in Breckenridge, Colorado, who previously worked on the foreign-exchange desk at Australia’s central bank.

For Bill Gross, dimming demand from foreign investors is adding to the pain as hedging costs rise. At the heart of this phenomenon is the swelling cost to convert payments from euro and yen into dollars.

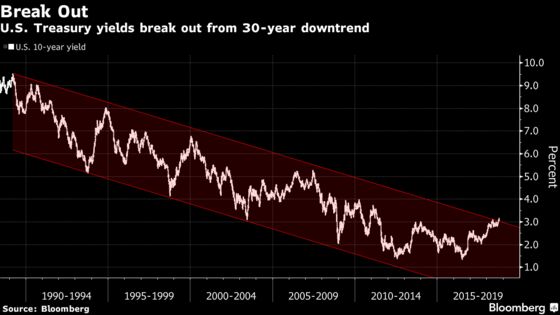

Meantime, chart levels may support the bearish view on Treasuries, after yields broke out of their 30-year downtrend. That set off “technical alarm bells” for some investors, according to Citigroup Inc.

For Marvin Loh, whose career in finance began in the 1980s when yields topped 15 percent, it’s important to remember that past. “There is still room for higher real yields from a historical perspective,” said Loh, a global strategist at Bank of New York Mellon Corp. in Boston.

--With assistance from Cormac Mullen, Shery Ahn, Chikafumi Hodo, Gregor Stuart Hunter, Manus Cranny and Yousef Gamal El-Din.

To contact the reporters on this story: Adam Haigh in Sydney at ahaigh1@bloomberg.net;Ruth Carson in Sydney at rliew6@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Cormac Mullen

©2018 Bloomberg L.P.