BOJ Policy Tweak That Matters for Global Bonds Already Underway

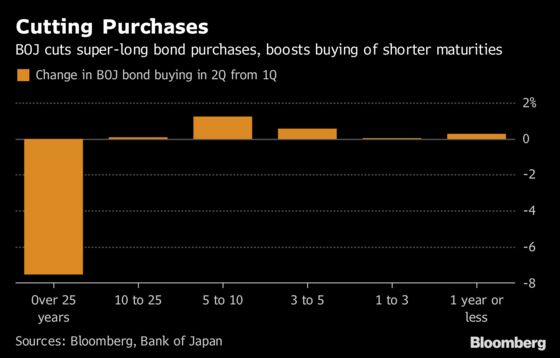

BOJ reduced purchases of bonds due in more than 25 years by 7.6% last quarter from the previous three months.

(Bloomberg) -- For all the speculation over possible Bank of Japan policy tweaks next week, the most important change for global bond markets may already be underway.

While market watchers disagree about whether the BOJ will adjust its target of keeping 10-year yields around zero percent, its steady reduction in purchases of longer-maturity debt and more expensive overseas hedging costs mean Japanese funds are already contemplating bringing more money back home.

The BOJ’s steps to buy fewer bonds has seen the annual increase in its debt holdings slow to 44.1 trillion yen ($397 billion) versus its guidance of 80 trillion yen. Last quarter the reductions were entirely focused on so-called super-long bonds, which are the most attractive to insurers. What happens next in the world’s second-largest bond market has the potential to cascade globally given Japanese investors hold $2.4 trillion of overseas debt.

“The BOJ is likely to cut bond purchases more drastically and more flexibly, which targets the super-long sector, to revive market liquidity and volatility,” said Jun Ishii, chief fixed-income strategist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo. “Once the 20- or 30-year yields approach 1 percent, funds that are taking a temporary shelter in foreign bonds will come back.’’

The BOJ reduced purchases of bonds due in more than 25 years by 7.6 percent last quarter from the previous three months, central bank data show. That compares with a slight increase for shorter maturities.

Two of the nation’s largest insurers, Japan Post Insurance Co. and Nippon Life Insurance Co., said in April they would consider buying more JGBs once 30-year yields climb above 1 percent. The yield closed at 0.815 percent on Friday, up from 0.685 percent a week ago.

Intensifying speculation about what the BOJ will decide at its July 30-31 meeting saw longer-maturity yields jump this week and affected debt markets are far away as the U.S., Europe and Australia. Reports from Reuters, Jiji, Bloomberg and other media indicated that officials are considering ways to reduce the side effects of their yield-curve control policy.

All 44 economists contacted by Bloomberg July 17-20 said the central bank will stick to its current settings for yield-curve control and asset purchases next week. The BOJ held an unlimited fixed-rate bond-purchase operation for five-to-10-year debt on Friday at a yield 0.10 percent, suggesting it is still determined to cap any increase.

Two of the most commonly talked about changes involve the BOJ allowing more fluctuation around its zero percent yield target, or adjusting the description of its 80 trillion yen bond holding guidance.

“If the BOJ were to make changes to yield-curve control, the spillover effects through global rates would be pretty significant,” said Richard Kelly, head of global strategy at Toronto-Dominion Bank in London. “If JGB yields start to move higher, you would see a waterfall effect of less demand for European or U.S. bonds that would likely shift the term structure higher globally.”

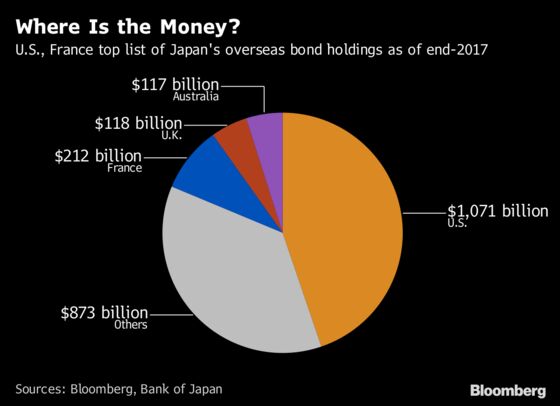

Japanese investors own more than $1 trillion of U.S. bonds, while their top 12 holdings also includes France, Italy and Spain, according to data from the BOJ. The following pie chart shows how their funds are distributed.

Japanese funds have already been pulling back from some overseas bond markets as currency hedging has become more expensive. The costs of hedging investments in dollars has jumped as Federal Reserve tightening pushes up U.S. short-term interest rates, and this has eaten into the extra yield Japanese investors can get for holding Treasuries.

If the BOJ does allow longer-maturity Japanese bond yields to rise, this will prompt local investors to put more money into JGBs, said Tsuyoshi Ueno, senior economist in Tokyo at NLI Research Institute, a unit of Nippon Life Insurance. “Investors will be delighted, having faced difficulties in raising returns given the high hedge costs for U.S. Treasury investments.”

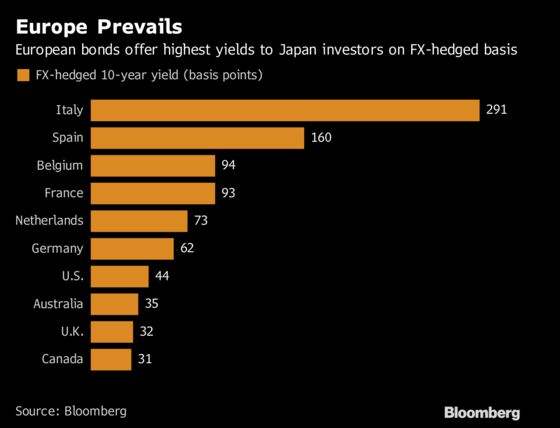

The premium for investing in European bonds has remained relatively more attractive as the European Central Bank maintains an accomodative monetary policy.

Not everyone believes next week’s BOJ meeting will have an outsized impact on global debt markets.

“The crux of the arguments is how the BOJ can improve the sustainability of its stimulus to continue it for a longer time,” said Masayuki Kichikawa, chief macro strategist at Sumitomo Mitsui Asset Management Co. in Tokyo. “I expect Japan’s long-dated yields to stay in a low range. A technical adjustment of 10 to 20 basis points wouldn’t change portfolio flows.”

Nikko Asset Management Co. predicts the BOJ will raise its 10-year bond yield target by 20 basis points during the fourth quarter and such a move may push up European yields by 10 basis points, said John Vail, chief global strategist in New York.

“Now that the market has accepted the likelihood of less dovish BOJ policy, the question is how it is structured and how quickly it will be implemented,” he said.

--With assistance from Emily Barrett, Liau Y-Sing and Cormac Mullen.

To contact the reporters on this story: Masaki Kondo in Singapore at mkondo3@bloomberg.net;Chikafumi Hodo in Tokyo at chodo@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds

©2018 Bloomberg L.P.