Kuroda to Keep Investors Guessing With Three-Month Policy Review

BOJ Plans Policy Sustainability Review as Price Falls Deepen

(Bloomberg) -- Haruhiko Kuroda conjured up another surprise at the Bank of Japan’s latest meeting, promising a review of its ultra-easy monetary policy without a total overhaul and leaving economists and investors with three months to speculate about possible changes.

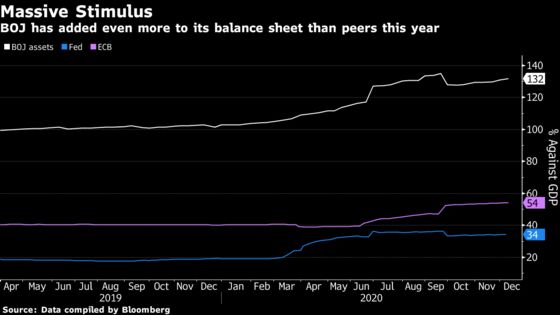

At its last meeting of a testing year, the BOJ officials led by Governor Kuroda extended by six months its special support programs for pandemic-hit businesses and kept its key interest rates and asset purchases unchanged, a combination expected by a majority of economists.

The review to make policy more sustainable was unexpected but comes amid growing concern over the length of time needed to hit the BOJ’s 2% inflation target. Figures out earlier in the day showed inflation even weaker than when Kuroda launched his massive easing campaign, with prices falling at the fastest pace in more than a decade.

With the review, Kuroda reinforces his reputation for surprises and showed once again a willingness to adjust course as he has following previous reassessments, along with a knack for buying time. The BOJ said it aimed to disclose the results of its review at its March meeting, extending the possibility of a stimulus change for an entire quarter and perhaps keeping yen bulls at bay.

“We’ll take a thorough look at all our various asset purchases and our management of yield-curve control,” Kuroda said at briefing after the decision. “Our intent is to keep short and long term policy interest rates at their present or lower levels, and we won’t be reviewing negative interest rates.”

Economists largely agreed that tweaking the BOJ’s framework was necessary to reduce its side effects as the time frame for achieving 2% inflation extended further into the future. Some said the bank would tweak forward guidance and increase the flexibility of its asset buying, while others wondered if the bank might try to target a shorter bond yield.

“Kuroda wanted to make it absolutely clear that this review isn’t about a tapering of monetary easing. He can’t back off when inflation is falling deeper and when the road to the price target has gotten even longer,” said Naomi Muguruma, senior market economist at Mitsubishi UFJ Morgan Stanley Securities.

The review would be more of a fine-tuning rather than a major change in policy framework as happened in 2016, she added.

A comprehensive assessment in 2016 dug the central bank out of a hole after the yen ended up appreciating, not falling, in the months following the BOJ’s adoption of negative rates. Banking sector stock prices plunged as profitability was squeezed and bond yields fell deeper into negative territory.

The resulting yield-curve-control framework gave central bankers a reworked approach for tackling the difficulties of supporting the economy, prices and market stability that also reduced the heavy lifting required by straight quantitative easing. In this way, the BOJ again forged another novel path for its peers, after they had followed the BOJ’s lead on QE.

The YCC framework has stayed intact since then, with only minor tweaks, and has been closely examined by other global banks.

The Reserve Bank of Australia adopted some parts of YCC earlier this year, but chose to target three-year government yields instead of the 10-year yields in the crosshairs of the BOJ.

At the briefing, Kuroda said the BOJ wasn’t specifically thinking about targeting a shorter maturity.

“The assessment probably won’t produce anything jaw-dropping,” said Kazuo Momma, a former executive director at the BOJ in charge of monetary policy. He said the BOJ would probably strengthen its forward guidance by tying it to progress toward the inflation target.

“They could make the ETF purchase program more like an emergency measure by ditching the upper limit and the annual target,” he added, referring to the BOJ’s current policy of buying exchange-trade funds at an annual pace of up to 12 trillion yen ($116 billion).

Bank of Japan Eyes Sustainability After Decade of ETF Buying

The BOJ may also have decided to announce its review now because of an awareness that Japan’s currency could come under pressure if investors see it as being less aggressive than other central banks as the world closes out one of the most fraught years in memory.

The Federal Reserve on Wednesday said it will maintain its asset purchases program until it sees substantial progress in the U.S. economy. The European Central Bank last week increased its emergency bond buying.

The yen was trading at around 103.55 against the dollar at 7:15 p.m. in Tokyo, a fraction weaker than immediately before the decision. The Japanese currency has strengthened from over 111 at the end of March. Yen appreciation squeezes the profitability of Japan’s big exporters and can add to downward pressure on domestic prices.

Economists see the 95-yen mark against the dollar as the line in the sand for the BOJ to cut rates. The possibility of policy changes in March could help keep a lid on appreciation over the coming months.

“We shouldn’t rule out further easing in March,” warned Hideo Kumano, executive chief economist at Dai-Ichi Life Research Institute and a former BOJ official. “I can’t imagine the BOJ will just say that fine-tuning is enough to give their stimulus longer life.”

©2020 Bloomberg L.P.