Fund Managers Sour on Global Growth Expectations, BofA Says

Fund Managers Sour on Global Growth Expectations, BofA Says

(Bloomberg) -- Fund managers may be quickly souring on global growth and earnings expectations, but their positioning remains pro-risk as they slash bond holdings to a record low and buy U.S. equities.

This is a key takeaway from the latest Bank of America Corp. monthly fund manager survey, conducted in the week through Oct. 14. While the outlook for global growth turned negative for the first time since April 2020 and the overall survey was the least bullish in a year, the allocation to bonds fell to the lowest level ever as inflation woes drove expectations for higher rates, according to BofA strategists.

Investors boosted their exposure to U.S. equities to a 16% overweight, the most since November 2020, while the overall positioning in stocks remained “very high,” but steady at a net 50%.

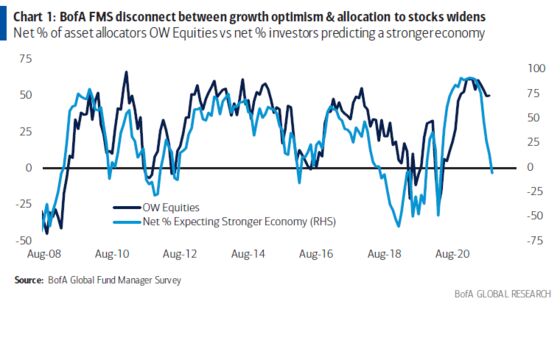

“The disconnect between growth optimism and allocation to stocks widens,” BofA strategists led by Michael Hartnett said in a note to clients.

Equities have been much more volatile over the past few weeks as inflation risks from higher energy prices and concerns over China’s slowdown have fueled an exit from frothier parts of the stock market. Still, as bond yields remain low, investors look to equities as the asset class that offers the most potential for returns.

But, some market participants did reduce their stock allocations. The BofA survey showed that hedge funds this month cut their net equity exposure to 26% from 41% in September. And the drop in bond holdings led to cash allocations rising to a net 27% overweight, the highest since July 2020, BofA said.

The global October survey included 380 participants with $1.2 trillion in assets.

Other global survey highlights include:

- Global profit expectations turn negative: net -15% is lowest since May 2020

- Majority of investors at 58% see inflation as transitory, while 38% say inflation is permanent although the gap continues to narrow

- Allocation to commodities increased to net 28% overweight, highest since July

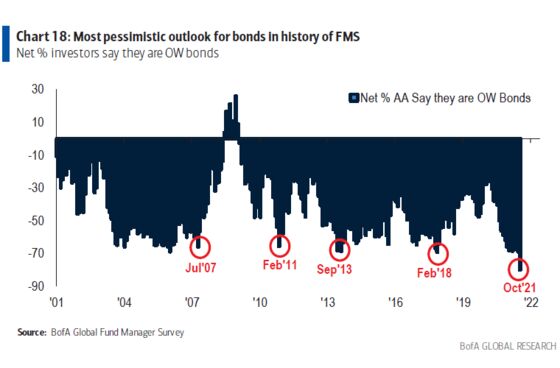

- Share of investors that expect a steeper yield curve has fallen “drastically” to 23%, the lowest level since June 2019; global bond allocation falls to a net -80%

- With the U.S. Federal Reserve expected to announce tapering in November, surveyed investors expect higher VIX volatility, stronger U.S. dollar and wider credit spreads

- Compared to September, fund managers bought energy, cash and banks, while reducing exposure to healthcare, bonds and staples

- Inflation is a top “tail risk” for 48% of surveyed investors, followed by China, asset bubbles and Fed tapering

- Most crowded trade is long tech stocks, followed by long ESG, short China and long Bitcoin

- Allocation to Eurozone equities declined to a net 34% overweight; allocation to U.K. equities fell to 12% underweight, largest underweight since January; exposure to Japanese equities increased to a net 7% overweight, first overweight since May

©2021 Bloomberg L.P.