BOE Policy Makers' Case for Rate Hikes Gets Thin

Monetary Policy Committee said it will continue to assume a Brexit deal in their forecasts until the government changes its policy

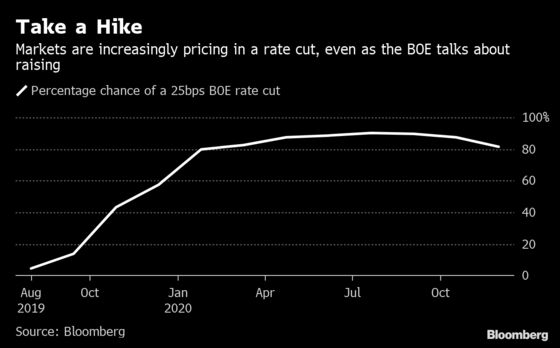

(Bloomberg) -- Bank of England policy makers may be losing faith in their own call for higher interest rates.

Officials have so far stuck to their expectation for interest rates to be raised “at a gradual pace and to a limited extent” over the next three years. Yet that projection assumes a smooth Brexit, which looks increasingly unlikely as both candidates to replace Theresa May as prime minister say they’re willing to leave the European Union without a transition.

The Monetary Policy Committee said it will continue to assume a Brexit deal in their forecasts until the government changes its policy. But both markets and economists are skeptical and are increasingly forecast rate cuts as soon as November.

Governor Mark Carney said that divergent outlook is “unsurprising,” and that officials will explore “how best to illustrate” the market “sensitivities” in August -- without elaborating on how.

But it would take more than a frictionless departure from the EU to prompt a tightening move. Any decision to raise would likely require global growth to maintain its pace. Since the June decision, policy makers Carney, Silvana Tenreyro and Gertjan Vlieghe have said the outlook is weakening.

Rate hike supporters also need to be confident that the current slowing in U.K. growth is a temporary phenomenon. Output looks set to be flat for the second quarter -- potentially avoiding the contraction that previously seemed inevitable, yet still representing a slowing of momentum from the start of the year around Britain’s originally scheduled departure date from the EU.

This volatile pattern risks repeating itself, Vlieghe said in a speech in London Friday, making the data harder for policy makers to gauge.

Price Pressure

There’s no impetus to hike from headline inflation. The rate held at the BOE’s 2% target in June, and the central bank sees it falling a bit more later this year.

For Tenreyro, the lack of inflation pressure is telling. Last week she said that “coupled with signs of a weaker global outlook, recent developments likely lengthen the period until there is a sufficient pickup in inflationary pressures for me to vote to raise bank rate. I do not currently anticipate such a pickup in the next few months.”

More hawkish members of the nine-member rate setting group have pointed to factors such as wage growth as backing the case for hikes. The most recent data -- which showed U.K. wages grew at the fastest pace in 11 years in the three months through May -- would seem support that view.

There were signs that the labor market may be starting to slow as Tenreyro has predicted though, with the weakest employment growth since the summer of 2018 and vacancies falling to their lowest level for a year.

Fed, ECB

Any rate increase would also require the BOE to swim against the tide. Federal Reserve Chairman Jerome Powell repeatedly cited a slower global economic expansion before Congress Wednesday, as he all but promised a cut at the end of this month.

At the European Central Bank, President Mario Draghi says more stimulus will be needed if the economy doesn’t improve, prompting investors to bet on a reduction of rates this summer.

“We have the Fed cutting rates this year, we have a mild U.S. recession coming maybe mid-next year,” said Brian Hilliard, chief U.K. economist at Societe Generale.“There is very little chance the BOE would raise rates this year -- very little.”

--With assistance from David Goodman.

To contact the reporters on this story: Lucy Meakin in London at lmeakin1@bloomberg.net;Olivia Konotey-Ahulu in London at okonoteyahul@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Brian Swint

©2019 Bloomberg L.P.