BOE Isn’t Tethered to Forecasts Suggesting Hikes, Saunders Says

Policy makers announce their next decision on Aug. 1.

(Bloomberg) -- Brexit vulnerabilities may stop the Bank of England from raising interest rates even if its forecasts imply a need to do so, according to policy maker Michael Saunders.

A smooth departure from the European Union, which the bank’s forecasts assume, is very uncertain, Saunders said in a Bloomberg interview. That means that even relatively hawkish projections will have a smaller-than-usual influence on his immediate policy vote.

Saunders has led the charge for the BOE’s last two interest-rate hikes, but his remarks suggest he’s in no rush to begin another push. The pound slid to the low of the day, and was down 0.3% at $1.2436 at 8:14 a.m. London time.

“The economy right now is clearly not overheating -- the underlying pace of growth, stripping out all of the funny effects, inventories, car shutdowns and so forth, is weak and below trend,” he said. In the bank’s previous round of forecasts, “the link from the forecast to my actual vote was quite loose.”

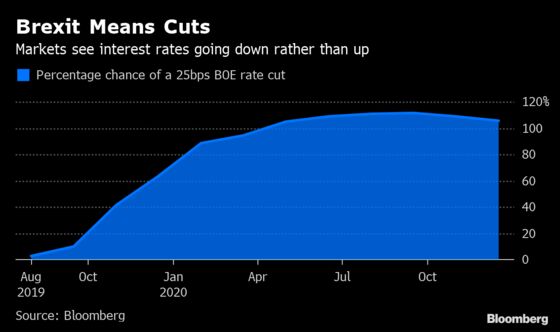

The Monetary Policy Committee updates its forecasts with its next decision on Aug. 1. The problem for the BOE is that it takes for granted the government’s stated policy for a smooth Brexit, while market expectations, which are also plugged into the estimates, are increasingly pricing in possible interest-rate cuts to contain the fallout from a chaotic departure.

Governor Mark Carney acknowledged the divergent outlooks in a speech in Bournemouth this month, and said officials will explore “how best to illustrate” the market “sensitivities” in August.

Speaking on Monday, Saunders said that the discrepancy means that the BOE’s official outlook may not be “a key driver of people’s policy vote.”

The most recent “forecast of excess demand and above-target inflation didn’t at that point prompt me to vote for higher rates, because the economy was not overheating, not growing above potential pace, we could afford to wait,” he said. “What you get then is a tension, a disparity, between the forecasts and the actual policy vote.”

If the U.K. does secure a deal, then rates will probably rise over time, Saunders said, adding that he is probably more optimistic than his colleagues about the outlook under such a scenario. The output gap has closed and the labor market has become tighter in recent years, he said.

However, if Britain falls out of the bloc on Oct. 31 without new trading arrangements in place, the policy response wouldn’t be automatic, Saunders said. Other MPC members have indicated in recent months that a cut in interest rates would be more likely.

“It’s hard to know how it would play out with any certainty,” he said. “I wouldn’t want to give a strong steer now as to which way policy would go.”

In the aftermath of the 2016 referendum, the MPC was faced with a more simple calculation when it cut interest rates. Now, the starting point of inflation at target and a supply-side economic disruption from a no-deal Brexit would pose more of a challenge, he said.

The current depreciation of the pound is an indication that the currency would fall even further if there’s a chaotic departure, he said, which would in turn lead to higher inflation and slower growth.

“Navigating a path back to the inflation target could be a pretty lengthy and complex period, but we would have the tools to fulfill our remit,” he said.

No matter what the BOE does though, “monetary policy could not prevent a no-deal Brexit being painful for the economy, for businesses and for households,” he said.

--With assistance from Lucy Meakin.

To contact the reporters on this story: David Goodman in London at dgoodman28@bloomberg.net;Jill Ward in London at jward98@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Brian Swint, Lucy Meakin

©2019 Bloomberg L.P.