Biggest U.K. Stimulus Since 1992 Relies on Borrowing Binge

Biggest U.K. Stimulus Since 1992 Relies on Borrowing Binge

(Bloomberg) -- The U.K.’s largest fiscal giveaway in almost three decades will be rooted in a borrowing binge that takes advantage of rock-bottom interest rates.

Rishi Sunak, the country’s finance minister, on Wednesday announced a 30 billion-pound ($39 billion) spending spree that ended years of austerity and laid out the most comprehensive response to the coronavirus threat among advanced economies. Just hours before his address, the Bank of England delivered an emergency interest-rate cut and unveiled other steps to help struggling businesses.

With the budget focusing on supporting the economy, the former Goldman Sachs banker avoided large tax increases or other measures to boost the government’s coffers. Instead, he is relying on the biggest borrowing program in eight years -- a splurge that will likely grow once the 12 billion pounds of stimulus to combat the virus is taken into account.

As major central banks almost run out of policy space to fight what could be the worst economic crisis since 2008, the focus has shifted to public spending to cushion the impact of the virus. An unprecedented drop in borrowing costs is signaling an all-clear from the bond market.

“We suspect this is just the tip of the iceberg of the fiscal loosening we’re likely to see in the U.K. in the coming years,” said Karen Ward, chief market strategist for EMEA at JPMorgan Asset Management. “Ambitions to balance the books have been abandoned.”

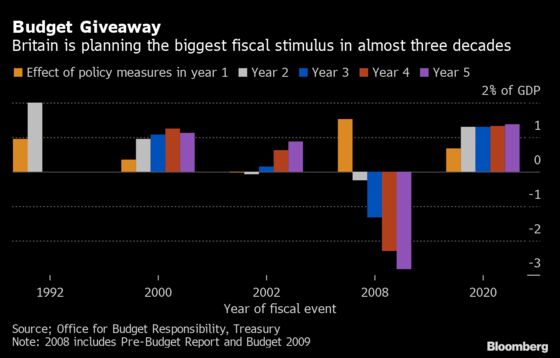

The extra borrowing marks a shift for the Conservative Party. It came to power following the global financial crisis pledging to bring the public finances under control after the budget deficit surged to 10% of economic output. While a decade of austerity reduced the shortfall to 2%, it took a brutal toll on public services, pay and welfare.

What Our Economists Say:

“Taken together, the U.K.’s policy response is unlikely to prevent the economy suffering in the first half, but it raises the chance of a rebound later in the year.”

-- Dan Hanson. For the full U.K. INSIGHT, click here

Enter Boris Johnson

That changed with the government of Prime Minister Boris Johnson, who pledged to increase spending to help poorer regions -- where voters switched to his party for the first time in December’s elections -- and close a wide wealth gap with London. The details of Johnson’s most ambitious plans have been postponed as the emergency response to the virus crisis dominates the government’s agenda.

Read more: DMO seeks guidance on auctions by phone due to virus

Yields on gilts, as U.K. government bonds are known, barely moved after the announcement, suggesting investors aren’t concerned that the spending will have an inflationary impact on an economy bracing for a hit to demand as well as supply-chain shocks.

“Given that borrowing costs are near zero, it makes perfect sense to rely heavily on the sale of gilts to fund the spending plan,” said Stefan Koopman, a market economist at Rabobank. “If the cash will indeed be used to boost productivity and improve the nation’s infrastructure, rating agencies probably won’t punish the nation for selling more debt.”

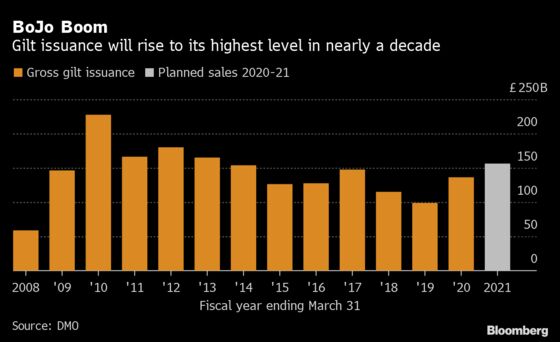

The stimulus is the U.K.’s biggest since 1992, when Conservative leader John Major was prime minister. In total, the giveaway will add around 125 billion pounds to Britain’s debt pile by 2025, taking outstanding borrowing over 2 trillion pounds for the first time.

Ratings company Moody’s Investors Service said while the plan will support the economy, it also means a “deterioration in the U.K.’s fiscal position.” That highlights the country’s ongoing difficulty in meaningfully reducing the high debt level, it said.

Robert Chote, chairman of the U.K. fiscal watchdog, also said public finances are now more vulnerable to “nasty surprises.”

“The risk is that financing conditions do not remain benign and borrowing costs rise because of risk premia, rather than a stronger outlook for economic growth,” he told reporters.

But the plunge in bond yields means that the U.K.’s debt services costs are now similar to the early-2000s as a share of gross domestic product, despite the overall burden being far higher. Money markets suggest policy makers probably won’t raise interest rates anytime soon.

Free Money

Boris Glass, U.K. economist at S&P Global Ratings, noted that the government “can currently borrow for almost free and is actually getting paid by lenders -- taking inflation into account.” The BOE’s rate cut “should push borrowing costs down even further. That creates some extra fiscal room,” he said.

For Ranko Berich, head of market analysis at Monex Europe Ltd., all of this means more debt sales.

The prospect of higher bond issuance “is now about as close to a metaphysical certainty as you can get in financial markets,” he said.

--With assistance from Neil Chatterjee, Dana El Baltaji and Zoe Schneeweiss.

To contact the reporters on this story: David Goodman in London at dgoodman28@bloomberg.net;William Shaw in London at wshaw20@bloomberg.net;Andrew Atkinson in London at a.atkinson@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Alaa Shahine, Fergal O'Brien

©2020 Bloomberg L.P.