Big Income Swings Strain Savings Plans for Millions of Americans

Big Income Swings Strain Savings Plans for Millions of Americans

(Bloomberg) -- American households experience large fluctuations in monthly incomes and spending over the course of a year that make it harder to budget for expenses, pay off debt and save for unexpected bills or income dips, according to a JPMorgan Chase Institute study.

Such volatility in personal finances has remained elevated in recent years despite millions of new jobs, steady wage gains and the longest economic expansion in U.S. history, data released Wednesday in Washington show. Families with a median level of income volatility saw their incomes fluctuate by an average of 36% from one month to the next, according the institute, which uses the largest U.S. bank’s customer data to track economic trends.

The group’s latest study is based on checking-account data from more than 6 million families from October 2012 to December 2018. Amassing such high-frequency data on a massive scale “gets us much closer to the cash-flow picture and reality that people live on a month-to-month basis,” Fiona Greig, who co-authored the report, said in an interview.

The latest report sheds new light on just how resilient consumers may be in a downturn, a key question as they drive the expansion in the world’s largest economy. Growth slowed to an annualized 1.5% in the third quarter, according to economists surveyed by Bloomberg before the government report due Oct. 30, from 2% in the second quarter.

The good news is that consumers were twice as likely to see incomes jump as they were to experience a plunge. Upward spikes are often seasonal, such as those from annual bonuses or tax refunds, while it’s less frequent to experience monthly income dropping by more than 25% of the median level over the past year, according to the analysis.

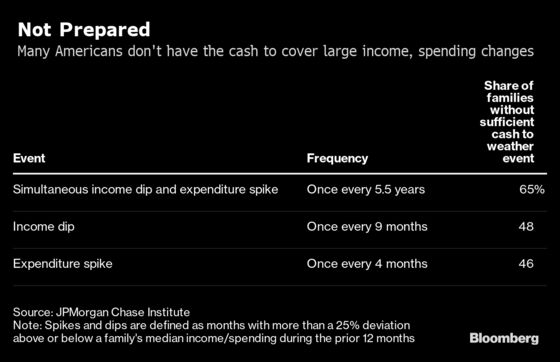

Even so, almost half of American families haven’t saved the equivalent of 2.8 weeks of income that would be needed to cover an income dip, which occurs about every nine months. In the rare event of a simultaneous spending spike and income dip, 65% of Americans wouldn’t have the approximately 6.2 weeks of income saved to weather it, the data show.

Volatility is greatest among high-income households and those where the primary account holder is between ages 18-24. Yet, when breaking down the difference between high-income and low-income households, income swings in the higher category tend to reflect larger and more frequent spikes, while volatility on the lower end typically reflects larger income dips, the data show.

In addition to fluctuations in income, month-to-month spending volatility is also high for the majority of households, and it includes predictable ones like holiday shopping as well as surprises such as medical bills. And those swings don’t decrease with age, according to the report by Greig, institute President Diana Farrell -- a former economic adviser to President Barack Obama -- and Chenxi Yu.

The institute says its mission is to use the lender’s customer data to help policy makers and businesses better understand the economy and make more informed decisions.

To contact the reporter on this story: Reade Pickert in Washington at epickert@bloomberg.net

To contact the editors responsible for this story: Scott Lanman at slanman@bloomberg.net, Jeff Kearns

©2019 Bloomberg L.P.