Biden’s Plans for Recovery Face Corporate America Debt Problem

Biden’s Plans for Recovery Face Corporate America Debt Problem

(Bloomberg) -- As President-elect Joe Biden looks to pull the economy out of the wreckage caused by the pandemic and onto a sustained path of recovery, his team faces one increasingly big problem: a mountain of corporate debt.

U.S. companies have borrowed billions of dollars to boost cash in order to get them through the outbreak that has shuttered businesses across the country. Investors, meanwhile, have been willing buyers amid unprecedented support by the Federal Reserve as a lender of last resort.

That poses a problem for the new administration when it takes over next month, as it’ll need companies that are ready to invest and hire in order to achieve their policy goals -- from raising the minimum wage to creating clean-energy jobs and getting unemployed Americans back to work. Instead, corporate America looks vulnerable.

“We’re playing this game against time,” said Kathy Jones, chief fixed-income strategist at Charles Schwab & Co. “Corporations can hang on, they have cheap debt, but the longer it takes to come out from under this, the more burdensome that debt is.”

Fed Backstop

When the Fed slashed interest rates to almost zero and backstopped corporate debt markets with its emergency lending facilities in March, investors rushed back in to capitalize on higher yields. That kicked off the biggest wave of corporate borrowing on record, allowing companies to load up on cash to weather the pandemic or refinance existing debt at cheap rates.

Corporate debt securities and loans ballooned by more than $850 billion from the end of last year through September, according to data from the Fed this month. Issuance of both junk and investment grade bonds hit new records this year.

The expectation of continued support is palpable on Wall Street. Though Treasury Secretary Steven Mnuchin has said the corporate lending facilities will close at the end of the year, analysts still perceive an implicit backstop.

“We see few risks that central bank support wanes if it is needed, whether it is through backstops, actual purchases, or new policies,” said Barclays Plc credit strategist Bradley Rogoff in a Dec. 4 note.

With an approved vaccine now in existence, investors are also betting on the best of all outcomes -- strong growth and limited credit stress for borrowers -- sending risk premiums on blue-chip corporate debt close to pre-pandemic levels and yields on junk bonds to all-time lows.

The Fed validated that optimism Wednesday, revising up its forecasts for growth and employment for next year. The median estimate by officials for 2021 GDP was 4.2% with unemployment averaging 5% in the final quarter of next year versus 6.7% last month.

The rapid jobs recovery would be unusual in the history of recent recessions, and economists said it isn’t likely without more fiscal stimulus. Though that appears to be nearing final negotiations in Congress, there are other red flags that might stymie a recovery as the pandemic rages on.

Road Ahead

Virus cases are surging and consumption has retrenched as states issue another round of curbs on social activity. The number of jobs gained by Americans slowed in November and about 10 million people remain out of work.

“The first quarter will certainly show significant effects from this,” Fed Chair Jerome Powell said at his press conference Wednesday. “Getting through the next four, five, six months, that is key.”

AMC Entertainment Holdings Inc., the world’s largest movie-theater chain, said it needs to raise at least $750 million to stay open and might go bankrupt if the effort doesn’t succeed. Without new financing, existing cash will be depleted as soon as next month, the company said in a Dec. 11 filing.

“There is a yawning gap between underlying fundamentals and valuations,” said Henry Peabody, a portfolio manager who oversees about $15 billion of global credit investments at MFS Investment Management in Boston. “It is not a problem until it is.”

For now, he adds, companies have “unfettered access” to bond markets and nobody is questioning whether they can pay the money back.

Many borrowers parked that money on the balance sheet as a precaution, and some may already be paying it back, Fed data suggests. Non-financial corporate debt fell about $100 billion in the third quarter.

The total amount of cash and marketable securities being held by nonfinancial companies in the S&P 500 index increased to $2.23 trillion in the most recent quarter, up nearly $500 billion over the last three quarters, according to data compiled by Bloomberg.

But some have been burning through the cash to stay afloat until normal times return.

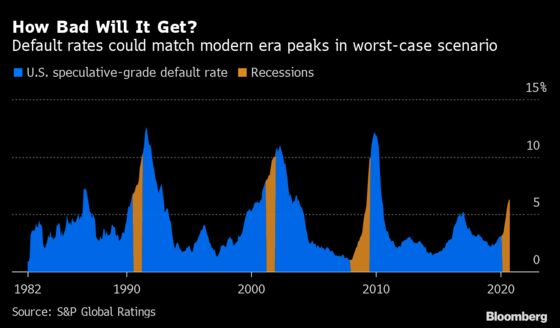

S&P Global Ratings says its base case scenario is for a default rate of 9% on speculative debt in the third quarter of 2021, while in a downside scenario of slow growth defaults could rise to 12%. That would be a level of credit distress not seen since the 1990 and 2008 recessions – and present a major challenge for Biden’s economic team.

Both those recessions featured an implosion of high-risk credits – junk bonds in the 1990s and dicey home mortgages during the financial crisis.

The pandemic borrowing surge “was a short-term massive benefit but there are long-term consequences,” said Gregg Lemos-Stein, global head of research and analytics at S&P.

“It is almost like a hangover effect. Except you never had the party,” he said.

There are ways out of the debt pile.

“You can inflate your way out, you can grow your way out, or you can restructure,” through default and bankruptcy, said Constance Hunter, chief economist at KPMG LLP. And growth is the optimal route, she said.

S&P’s best case scenario is for a default rate of just 3.5% in the third quarter of next year.

Looking across the economy, Albert Togut, founding partner at bankruptcy specialists Togut, Segal & Segal, says there is a “hope and a prayer that everything is going to come back like it was before the pandemic” on the part of some companies.

“What could happen is scary,” he says. “All the debt – it’s pervasive, it’s everywhere. How on earth are we going to pay it back unless there are restructurings at every level?”

©2020 Bloomberg L.P.