(Bloomberg Opinion) -- When times are good, focus on the top line and the bottom line will look after itself. When times are bad, you should do the reverse.

That looks a lot like the strategy the world’s biggest miner, BHP Group, has followed over the years in appointing its chief executive officers. The question the resources sector should ask in looking at Thursday’s appointment of Mike Henry to succeed Andrew Mackenzie is whether his focus is the top line, or the bottom.

Henry has spent the last three years as the operations chief for BHP’s Australian assets, where he’s focused on improving efficiency and bringing down costs — resolutely bottom-line work. The bulk of his experience, however, is in the top-line marketing side of the business — finding ways to get the best possible prices for the minerals BHP digs and pumps.

That resume harks back to Mackenzie’s predecessor.

With an upswing in prices for its key commodities of iron ore, coal and oil under way in 2007, BHP appointed Marius Kloppers, a South African veteran of its manganese business, to the chief executive role. Kloppers pushed hard to shift the pricing of first manganese, and then iron ore and coal, toward spot markets that more closely track supply and demand.

That helped BHP and its competitors extract additional revenues from their customers as spot prices surged in the years before and after the 2008 financial crisis — but when the market started to turn six years later, the emphasis started to look misplaced. After the demand growth that had supported the capital spending boom of the Kloppers era started to ebb, BHP's operations looked bloated and wasteful.

Mackenzie, with a background running petrochemicals for BP Plc and mines for Rio Tinto Group and BHP, was brought in as an operational wizard to fix the rot. He slimmed down the business, spun off the less attractive assets as South32 Ltd., and reduced expenditure to a level that could survive in the new, leaner environment.

At first blush, Henry looks like a swing of the pendulum from Mackenzie’s operations focus back to Kloppers’ marketing background.

He sold first coal, then energy and freight and petroleum for BHP before being appointed as Kloppers’ marketing president and then chief marketing officer in 2010. Only after Mackenzie took over the top job and Henry was entering the frame as a potential eventual successor was he shifted over to round out his experience on the operations side.

There’s reason to think that a more bullish focus is finally due. The resources sector has never really climbed out of the slump it entered around 2014, but the S&P 500 breaks new records on a daily basis. Forecasters could be underestimating the potential of a strong economic rebound in 2020, according to Goldman Sachs Group Inc.

Bloomberg’s indexes of energy and industrial metals are still at subdued levels, but the run-up in iron ore prices this year put Australia & New Zealand Banking Group Ltd.’s index of bulk materials such as iron and coal at its highest level since 2013. That should be good news for BHP, since its share price tends to track that benchmark closely.

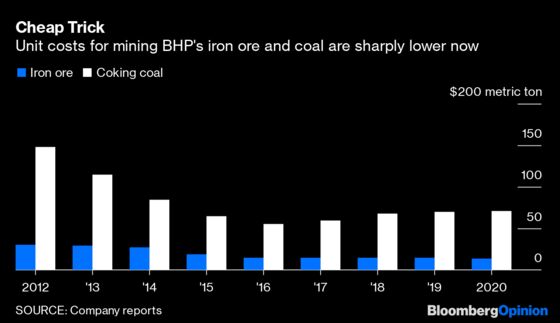

At the same time, it seems to have been as much Henry’s recent experience managing mines that’s recommended him for the top job. He’s been responsible for rolling out autonomous trucks at the Jimblebar iron ore mine in northwest Australia and for setting up operations centers in Perth and Brisbane to run the company’s iron and coal mines remotely. Costs of late have been sharply lower in both divisions, although those for Queensland coal are creeping back up.

If anything, it’s a sign of how things have changed for the mining industry that even scions of the marketing business like Henry have turned into born-again operations experts. BHP still has Elliott Management Corp. hanging around as a major shareholder. While its activist campaign will have been quiet for almost two years by the time Henry assumes the top job in January, it remains a constraint on any chief executive in a bullish mood.

More to the point, a stronger outlook for the U.S. economy isn’t the medicine that can revive BHP’s boom years. China still consumes about half of almost every major mined commodity and accounted for about 55% of BHP’s revenue last year — and all the evidence is that the economy there is slowing. BHP’s key commodities could be heading for an even rougher patch if China’s car market continues to crater and its still-buoyant conditions in real estate fall to more normal levels.

Should that be the case, the pendulum won’t be swinging back from the bean-counters to the marketers. If anything, it will have further to go in the other direction.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.