Bets on 2022 Fed Rate Hikes Dented as CPI Matches Expectations

Treasuries pared earlier declines after a keenly watched figures on U.S. inflation were largely in line with expectations.

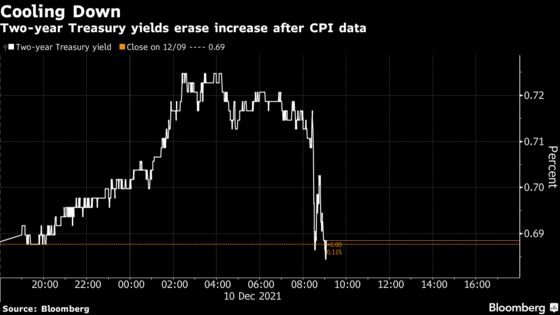

(Bloomberg) -- Treasuries erased losses after keenly watched figures on U.S. inflation matched expectations, with traders paring their bets on rate hikes by the Federal Reserve.

Benchmark 10-year yields fell two basis points to 1.48%, after early rising as high as 1.52%. The move was mostly driven by a decline in inflation expectations, with the 10-year breakeven rate slipping four basis points to 2.45%. The real yields, or rates on Treasury Inflation-Protected Securities, rose above minus 1%.

Prospects that inflation will be held in check may weigh against the need for the Fed to speed up the process of policy tightening. Swaps tied to Fed meetings indicate around 70 basis points of benchmark rate increases for 2022, down a few basis points from before the consumer-price data.

Officials are due to deliver their next decision on Wednesday, and analysts are watching for a potential acceleration in the pace of asset-purchase tapering -- a precursor to eventual rate hikes by the central bank. The Fed will also release its latest dot-plot on future path of interest rates, which is currently evenly split between no-hike and at least one increase.

The consumer price index increased 6.8% from November 2020, the fastest annual pace in nearly 40 years. It matched the median forecasts in a Bloomberg survey of economists. Some of the economists had predicted an increase above 7%.

“Perhaps people positioned for worse,” said John Briggs, global head of desk strategy at NatWest Markets. “It feels like a bit of a buy the rumor, sell the fact. I think market will worry about a higher dot-path and could flatten a bit more.”

Friday’s rally pared the Treasuries’ loss this week, with 10-year yields rising 11 basis points. It reversed a three-week rally, as concerns receded that the omicron Covid strain may derail the global economic recovery.

The market measure of inflation expectations has peaked in mid-November as the Fed signaled that it may accelerated its retreat from the pandemic stimulus to shift their focuses on taming inflation. Even so, the five-year breakeven rates remained at 2.75%, suggesting investors expect inflation to stay elevated. Friday’s inflation report showed core CPI index rose 0.8%, more than the median forecast of 0.7%.

Core inflation “continues to remain sticky and you are continuing to see inflation broaden out,” Erin Browne, portfolio manager at Pacific Investment Management Co., told Bloomberg Television. “If that continues into early next year and mid next year, that’s when the Fed is going to make the decision of whether or not to accelerate their tightening.”

While rate traders have ramped up their expectations for the Fed tightening next year, they are pricing in a total rate hikes far less than what the Fed projected on the dot-plot. The one-year swap rate in five years, a proxy for the peak of the Fed’s policy rate, is trading below 1.5%, compared with 2.5%, a level that the Fed indicates as neutral.

The benign expectation of the Fed’s upcoming tightening cycle has capped the long-term Treasury yields, leaving the real-yields deeply negative. The markets are debating whether this represents a mispricing of the Fed’s policy or pointing to a sluggish economic outlook in coming years.

“The market is telling us that it believes the Fed will contain inflation,” said Kathy Jones, chief fixed-income strategist at Charles Schwab & Co. “That high debt levels and weak demographics will limit inflation long term and that strong demand globally for long duration assets is keeping a lid on yields.”

©2021 Bloomberg L.P.