Bankers Are Sick of Choosing Sides Between Qatar and Saudi Arabia

When Saudi Arabia cut ties with Qatar in mid-2017, many international bankers chose to chase a potential fee windfall in Riyadh.

(Bloomberg) -- When Saudi Arabia cut ties with Qatar in mid-2017, many international bankers chose to chase a potential fee windfall in Riyadh over doing deals with its rich but isolated neighbor.

They’re not willing to pick sides anymore.

Executives from HSBC Holdings Plc, Goldman Sachs Group Inc. and other global banks are intensifying efforts to repair ties with Qatar’s finance ministry and sovereign wealth fund, according to interviews with people close to the lenders and Qatar’s government. While the kingdom remains key for business, some bankers regret diverting their attention from Doha after being blindsided when the Saudis delayed the sale of a stake in oil giant Aramco in July, they said.

“Banks are never fond of picking sides, but decreasing tensions in this affair provide an opportunity for executives to explore normalizing their activity,” said Ayham Kamel, Eurasia Group’s London-based practice head for Middle East and North Africa. “The geopolitical context for the Qatar crisis has changed, and at the very least, the crisis will not move in an escalatory direction.”

Bankers are especially keen to win back the trust of Finance Minister Ali Shareef Al Emadi, a man who sits on the boards of the country’s biggest bank, national airline and sovereign wealth fund, said one person with direct knowledge of the government. In December, about a dozen managing directors from global banks descended on Doha for the Euromoney conference where Emadi was speaking. Some flew in from Dubai via Oman or Kuwait since direct flights were banned after the feud erupted. Almost none had shown up to the same event a year earlier.

The stakes of doing business with Qatar seemed a lot higher at the time because Saudi Arabia and the United Arab Emirates were informally warning bankers that close ties with Doha could have consequences, according to some of the executives who declined to be identified because of the sensitivity of the subject. Central banks even demanded that lenders reveal their exposure to Qatari clients, people familiar had said.

Along with Bahrain and Egypt, the two countries were several months into an economic, diplomatic and political boycott of Qatar, which they accuse of financing terrorism and cozying up to Iran — allegations Doha denies. More broadly, Crown Prince Mohammed bin Salman, the kingdom’s young leader known as MBS, has made enemies with a series of aggressive foreign policies.

“MBS has changed the rules of the game in terms of Saudi domestic and economic policy, without much sense of what the new rules are,” said Gregory Gause, a professor of international affairs and a Saudi specialist at Texas A&M University. “That is going to discourage investment. His risk-taking on the international scene is similarly going to cause doubts for international investors.”

For a while, the coercion worked. Bankers had spent years arranging cheap loans and bonds for the kingdom’s borrowers so they’d be favored once more lucrative initial public offerings, mergers and acquisitions came to fruition. With Aramco presumably months away from raising as much as $100 billion in an IPO and another $40 billion in privatizations on the horizon, staying on the fence was risky.

So, while they kept offices and staff in Doha and said nothing publicly about the political quandary, behind the scenes many chose to play it safe and distance themselves from Qatar, people said. Meanwhile, a lot of Qatari business started to be done from London or New York instead of Dubai, the Middle East’s financial hub.

HSBC, traditionally the region’s biggest dealmaker, hasn’t arranged a single public transaction in Qatar since the standoff started in June 2017, according to data compiled by Bloomberg. It worked on 15 bond sales in the country in the previous two years, the data show.

Japan’s Mizuho Bank Ltd. wasn’t as careful. It was hired to help Qatar arrange $12 billion of bonds last year, but later quit the deal because officials from Saudi Arabia’s Debt Management Office, a unit of the finance ministry, made the bank choose which bond it wanted to work on, according to a person with direct knowledge of the events. The peace offering wasn’t enough — the Saudis ended up kicking Mizuho off their $11 billion Eurobond, too. Mizuho declined to comment. “The Ministry of Finance appoints banks based on their capability, commitments and availability to serve the kingdom,” said a spokesman for the ministry.

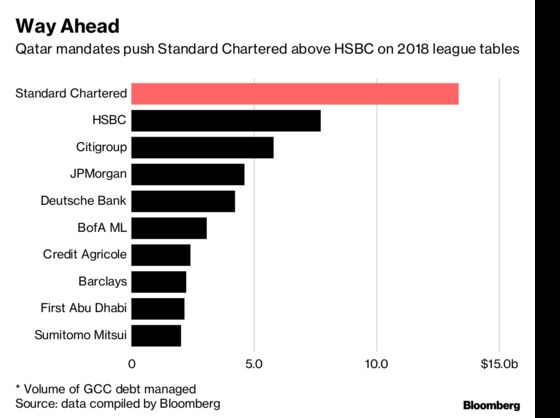

Not everyone who played both sides got stung. Standard Chartered Plc arranged $12 billion of bonds for the Qatari government in 2018, and still managed to carve out another $1.4 billion from Saudi issuers. It overtook HSBC as the biggest manager of regional bonds for the first time as a result.

Representatives from HSBC, Standard Chartered and Goldman Sachs declined to comment on how they’ve navigated the political turmoil. Qatar’s finance ministry and the Qatar Investment Authority didn’t respond to requests to comment.

The tide moved in Doha’s favor when Saudi Arabia did an about-face on the Aramco IPO that many banks were counting for big fee payouts, according to people familiar. Some privatization plans — the sale of the Riyadh airport, a stake in the stock exchange and others—have also gone nowhere. Even so, bankers prefer to rebuild bridges with Qatar quietly so as not to jeopardize their Saudi business, people said, especially with the privatization authority hoping to generate about $11 billion from asset sales this year.

The international outcry over the murder of U.S.-based columnist Jamal Khashoggi has only helped things along for Qatar. Just weeks before the Qataris invited global banks to two investment conferences, some bank executives skipped a major gathering in Riyadh to avoid the negative publicity. Many regional representatives who attended pulled their neck ties over their badges to conceal their identity, something they didn’t do at Euromoney or the Doha Forum in December.

Christian Sewing, chief executive of Deutsche Bank AG, withdrew from the Riyadh event at the last minute, only to later appear on a panel in Doha, home to some of the lender’s biggest shareholders. A number of bankers attended the conference for the sole purpose of shaking hands with the finance minister Emadi and officials from the country’s sovereign fund, some of the people said.

While people familiar said Qatar will hesitate to mend fences with banks that are deeply aligned with the Saudis, it’s likely to welcome overtures from others for the big deals it has in the pipeline, according to Rory Fyfe, chief economist at the London-based research company MENA Advisors.

Qatar is spending $25 billion on infrastructure upgrades this year to prepare for the 2022 World Cup. It’s also building liquefied natural gas capacity to add $40 billion to revenue by 2024, furnishing the $320 billion Qatar Investment Authority with more cash. The fund is currently eyeing U.S. tech acquisitions to balance holdings in European bank stocks and London property.

“There are deals coming up in Qatar that are too lucrative to miss,” said Fyfe. “Qatar would welcome most of them back and I suspect, given the changing climate, that Saudi is likely to apply less pressure” on the international banks it works with.

--With assistance from Zainab Fattah.

To contact the editor responsible for this story: Stefania Bianchi at sbianchi10@bloomberg.net, Daliah Merzaban

©2019 Bloomberg L.P.