Bank of England Weighs Up What to Throw Next at Virus Misery

Bank of England Weighs Up What to Throw Next at Virus Misery

(Bloomberg) -- Bank of England policy makers will meet this week knowing that they’ll probably have to do more to combat the U.K.’s economic slump, if not now then soon.

With the government all but certain to ramp up spending to save jobs and keep businesses afloat, Governor Andrew Bailey may signal he’s willing to buy more debt to keep borrowing costs from rising. At the current pace, the central bank will hit its current bond-buying goal around the end of June.

In their policy decision on Thursday -- a rare early morning one that includes a financial stability report -- officials will also likely lay out multiple paths for growth and inflation based on how long the lockdown lasts. Those will highlight the risk of economic “scarring” that they are especially eager to avoid.

“The question is, do they want to do more quantitative easing, and that’s a question they’ll have to address sooner rather than later,” said George Buckley, chief U.K. Economist at Nomura. “They probably will end up announcing more in June, and it may be that they give a nod to that this month.”

Like other central banks, the coronavirus has pushed the BOE to the limits of its powers, with a focus on its controversial role helping Prime Minister Boris Johnson’s administration spend its way out of the crisis.

While the bank’s job isn’t to finance the government, officials are aware that if they don’t use QE to soak up the massive public debt issuance needed to cover the cost of the pandemic, wary investors could eventually push up borrowing costs. That could prolong the downturn.

This will be the bank’s first formal forecast round since the pandemic struck the U.K., and modeling the future is even harder than usual. Publishing scenarios is an approach taken by the European Central Bank, which said the euro-zone economy could shrink by 5-12% this year, fully recovering either next year or only as late as 2022.

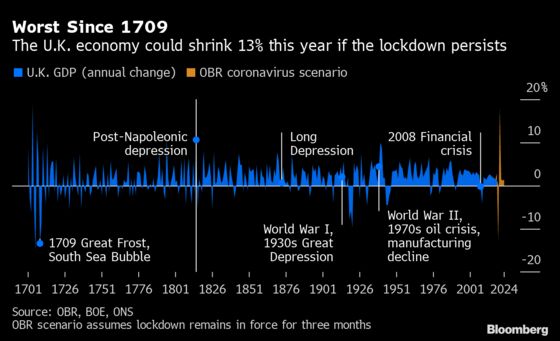

The BOE has already acknowledged that British output could slump, describing an Office for Budget Responsibility scenario that suggested a 13% drop based on a three-month lockdown as not implausible.

It’ll need to be careful not to give the impression it’s making hard forecasts for the length of the crisis though. Bailey won’t address the issue at the usual press conference, which has been canceled and replaced by an embargoed call with journalists.

What Our Economists Say:

“Alongside concerns about the economic recovery, the BOE will also be mindful that with gilt issuance continuing apace, financial conditions could easily tighten again later in the year. This makes it likely the central bank will increase its asset purchase target again in both June and August.”

--Dan Hanson, Bloomberg Economics. For the full INSIGHT, click here

The additional 200 billion pounds ($250 billion) of QE announced in March almost exactly match the government’s plans for extra borrowing to cover crisis stimulus. If more public spending is needed, as seems likely, the BOE could feel it needs to take the pressure off already-strained investors.

That raises concerns that it may be directly financing the government and risks fueling rapid inflation in the future. Monetary Policy Member Gertjan Vlieghe dismissed such worries last month by saying the BOE isn’t following government orders and its operational independence isn’t being compromised.

The BOE has already slashed its benchmark interest rate to a record-low 0.1% and stepped up government and corporate bond purchases. For commercial lenders, it has cut the liquidity buffer they’re required to hold to zero, and has teamed up with its peers to ensure plentiful access to dollars and euros.

The slump in demand and subsequent downturn could be the biggest in centuries, Vlieghe said. The outlook for inflation -- below the BOE’s 2% target even before the virus -- has weakened considerably, exacerbated by the collapse in oil prices.

The bank will probably take the view that it faces disinfltionary pressures over the next 2-3 years, according to JPMorgan Chase economist Allan Monks, “reinforcing the case for announcing further stimulus.”

©2020 Bloomberg L.P.