Bank of England Set to Take Steps Toward Tightening Monetary Policy

Bank of England Set to Step Toward Tightening Monetary Policy

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

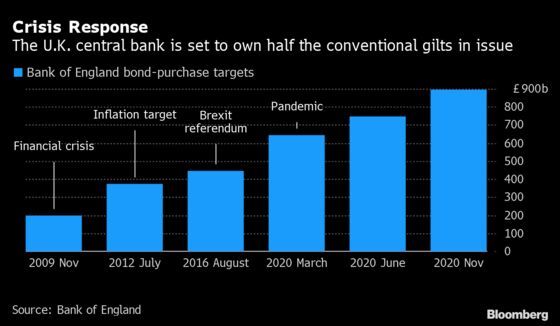

The Bank of England may move a step closer to tightening monetary policy, showing a path toward unwinding almost 900 billion pounds ($1.2 trillion) government bond purchases while also opening the possibility that borrowing costs could be pushed below zero.

While the two decisions pull in opposite directions, they could prove inextricably linked. They feed into the debate about which policy levers the U.K. central bank will pull first when the time comes to tighten monetary policy.

Officials led by Governor Andrew Bailey have signaled that they want interest rates higher than their current level before selling off some of the government bonds they’ve built up through their quantitative easing program. Adopting negative rates as a potential policy tool could allow them to bring forward the moment when they scale back their bulging balance sheet. They also could prepare the ground for bolder action.

“It makes sense for them to come out and let the market know what their new guidance is, sooner rather than later,” said John Wraith, head of U.K. and European rates strategy at UBS Group AG. “The simplest thing,” he said, would be for the BOE to lower the 1.5% threshold for where rates should be before bond sales start -- a possibility if there’s acknowledgment that rates may slip into negative territory.

Officials are due to announce their latest policy decision on Thursday. They’re expected to keep their stance unchanged at 0.1%, albeit with some dissenting voices calling for an early end to bond purchases. The current QE program envisages 150 billion pounds of bond purchases this year. Here are the issues guiding the BOE’s decision:

Economic Outlook

While the U.K. has rebounded sharply from its pandemic recession, central bankers are likely to hold off on tightening until more of the 1.9 million people on the government’s furlough program are back at work. That measure supporting wages finishes at the end of September. The concern is that unemployment will surge in the coming months.

“You have a lot of people on furlough who used to work in retail or air travel,” said Elizabeth Martins, senior economist at HSBC. “You can’t just persuade them to be truck drivers.”

There are also signs that the U.K. growth may have “seen the best of the rebound,” according to George Buckley, chief U.K. and euro-area economist at Nomura International. Real-time indicators showed more of a pop than a boom from the end of most restrictions on July 19. Businesses are wary about the spread of new virus variants, which put a chill on the outlook of purchasing managers.

What Bloomberg Economics Says ...

“The Bank of England is likely to keep its foot firmly on the pedal in August even amid hawkish noises from some members of the Monetary Policy Committee. The rapid spread of the delta varianthas created more uncertainty about the economic outlook, while the current surge in inflation is likely to be seen as transitory. Our base is that the first rate hike comes at the end of 2022.”

--Dan Hanson, Bloomberg Economics. Click for the full PREVIEW.

Inflation Forecasts

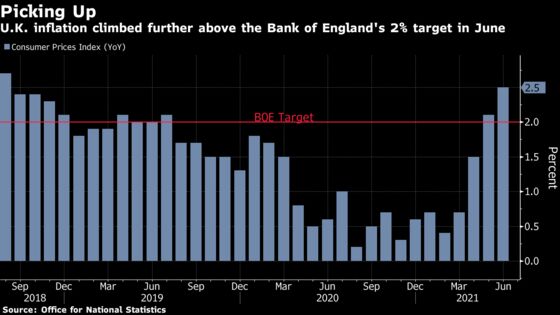

Much of the conversation in the past few months has been dominated by a spike in inflation, both in the U.K. and around the world. Consumer price growth rose 2.5% from a year ago in June, the most since 2018 and a half point higher than the BOE’s target.

While Governor Andrew Bailey and the majority of other MPC members have repeatedly said that much of the increase is likely to prove temporary, bank now estimates that inflation will exceed 3% this year. A sharp increase in the bank’s forecasts for price growth could provide a hint that tightening may be required earlier than expected.

Signs of a Split

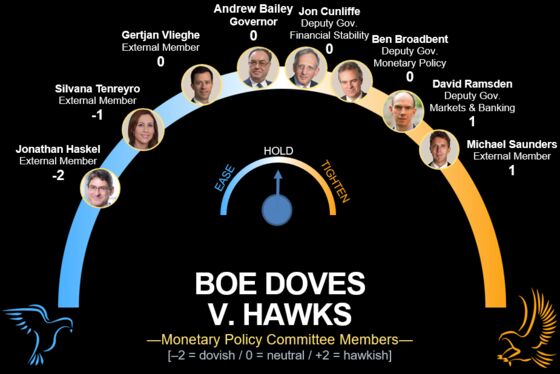

After unifying on the need for stimulus last year and in the early months of 2021, policy makers are starting to diverge on when to tighten. Michael Saunders, an external member of the MPC, is most likely to vote against completing the QE program in full. He could be joined by Deputy Governor Dave Ramsden. Both made hawkish comments in recent weeks.

“Markets are expecting a vote split 6-2,” said Robert Wood, chief U.K. economist at Merrill Lynch International, adding that further dissent would constitute a surprise.

Traders have increased bets on rate increases. They’re pricing in 13 basis points of hikes by the middle of 2022, versus as few as 7 points last month.

Charting an Exit

Talk of tighter policy has sharpened the focus how and when the MPC will act. Officials began a review earlier this year, and the BOE may provide some update on that discussion.

Most economists expect the bank to lower the level of interest rates needed to before QE starts to unwind. At the moment, the bank has suggested that rates need to move to 1.5% before they sell bonds. Opening the possibility of negative rates might allow the BOE to act before rates rise to that level.

A more drastic change remains possible. Bailey last year suggested he was open to a major shift, and was prepared to reduce the institution’s balance sheet before raising interest rates.

Still, not everyone expects that the review is imminent, with RBC economists suggesting it may not come until November.

©2021 Bloomberg L.P.