Bank of England Plays Tough Cop in U.K. Economy Role Switch

Bank of England Plays Tough Cop in U.K. Economy Role Switch

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

Like they did after the 2008 crash, the U.K.’s two economic policy heavyweights are playing good cop-bad cop. It’s just that this time they’ve swapped roles.

In the years following the financial crisis, the Bank of England stuck resolutely to easy money while fiscal policy got tough when Chancellor of the Exchequer George Osborne imposed swingeing budget cuts.

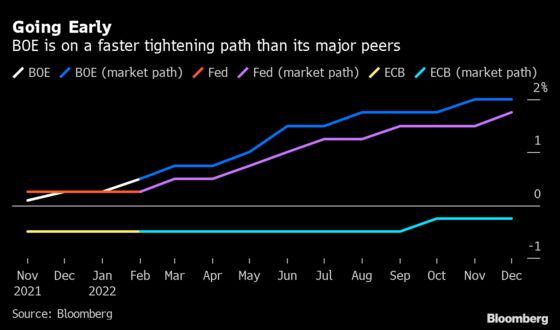

But as the economy grapples with the highest inflation level in three decades and the fallout from the war in Ukraine, it’s BOE Governor Andrew Bailey who’s playing the bogeyman. The central bank, which is expected to hike interest rates for a third straight meeting on Thursday, is taking the lead among global peers with a high-speed tightening of monetary policy,

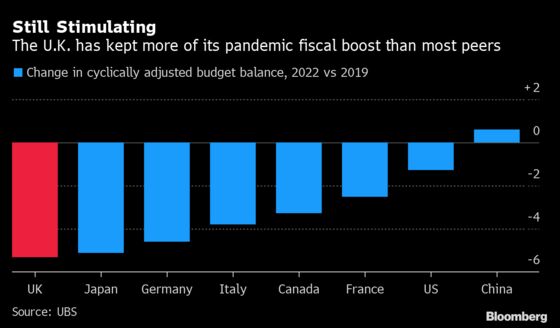

By contrast, Treasury chief Rishi Sunak -- for all his talk of the need to rein in borrowing -- is keeping more of his pandemic fiscal stimulus in place than most other developed countries and spending billions more to shield households from a surge in the cost of everyday goods and services.

Tellingly, as the conflict in Ukraine rages, it’s also the Chancellor, not the BOE, who is facing increasing calls to step in to support the economy further.

The switch among the policy heavyweights may come into sharper focus this month, when the BOE’s rate decision is set to be followed within days by Sunak’s spring statement, a fiscal update akin to a mini-budget.

The turnaround is part of a wider re-evaluation of how fiscal and monetary policies can best work to support economies, in the U.K. and beyond.

“Having got through this thing, there’s a real need for ongoing fiscal support,” said David Owen of Saltmarsh Economics. “Fiscal policy should be used pretty proactively. The combination of that along with a tightening of monetary policy to me makes perfect sense. I’m really all for it -- it puts the U.K. internationally in a good position.”

Put simply: In the pandemic, compared with the Great Recession, budget spending did more of the heavy lifting. Governments doled out more cash. Economies bounced back faster. And policy makers trying to manage the recovery now face a different set of problems -- above all, inflation.

The U.K. was one of the biggest Covid spenders. Its budget stimulus was matched only by the U.S., relative to the size of their economies, according to UBS. Sunak’s measures to prop up incomes for workers and businesses cost a total of about 370 billion pounds ($484 billion), including loans.

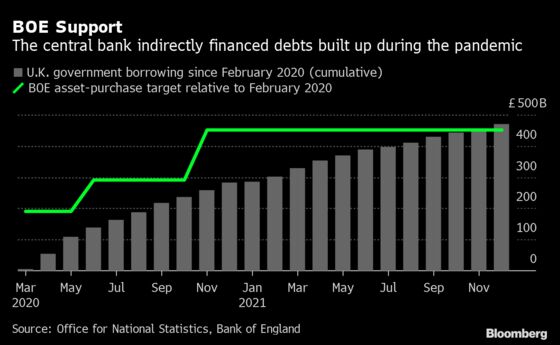

The BOE offered full support, slashing interest rates to near-zero and buying government debt to soak up the extra borrowing. The 440 billion pounds of BOE bond buying between March 2020 and December 2021 was enough to offset about 94% of the increase in the U.K.’s net borrowing requirement over the period.

In the years after 2008, when the economy was slow to recover, the government soon pivoted to arguing that the top priority was to lower budget deficits and debt.

Osborne used the specter of bond-market turmoil and debt crises in euro-area countries like Greece or Spain to invoke the need for fiscal austerity. And he pointed to the low interest rates on British government debt as evidence that his plan was working.

In hindsight, though, many economists are inclined to credit monetary policy for that achievement. In other words: if U.K. borrowing costs stayed low, it was because the BOE kept them that way. That argument was only reinforced when intervention by the European Central Bank -- Mario Draghi’s famous “whatever it takes” –- succeeded in bringing down bond yields in even the most fiscally challenged euro-members.

“I never understood George Osborne’s mantra of the need to get the deficit down at the time,” Owen said. “Covid has changed a lot of these things in this world we are currently in and I don’t see an issue with rolling out more targeted measures.”

As the pandemic fades, Sunak -- like his Conservative Party predecessor Osborne -- has also been talking about the need to get public finances back into shape. He’s actually gone further than many finance ministers by raising taxes to pay for some of the pandemic spending.

But that step has been accompanied by policies like giving households financial aid to cope with higher energy bills and signing off spending increases for every government department over the next three years. Now, the Treasury is facing calls is turn the spending taps on further, to help firms cope with a historic surge in energy prices following Russia’s invasion of Ukraine.

Meanwhile, with inflation hitting an 30-year high of 5.5% -- and forecast by some to hit 10% later this year as a result of the Ukraine crisis -- it’s been the central bank that hit the brakes early and hard. The BOE has already hiked rates twice -- before the U.S. Federal Reserve, for example, even got started on tightening -- and announced a run-down of its bond holdings.

At some point, the chancellor himself may feel the sting of the BOE’s newfound hawkishness. If central bank policies helped keep government borrowing costs down after 2008, then they’re having the opposite effect right now, as gilt yields rise in line with anticipated rate hikes.

Should the BOE benchmark hit 2% this year, as markets are predicting, then the cost of servicing bonds held under the BOE’s QE plan alone will jump hit 17 billion pounds a year, about double the level before officials hiked rates for the first time in December, according to calculations by Bloomberg.

©2022 Bloomberg L.P.