Bank of America Is Already Calling Time on China Stock Rally

Chinese authorities have a long history of stepping in to support equities via the so-called “national team” of state funds.

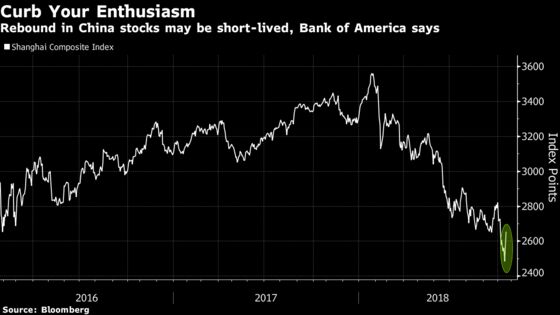

(Bloomberg) -- Don’t get too excited by the steepest rally in Chinese stocks since 2016, says Bank of America Merrill Lynch.

The Shanghai Composite Index’s two-day gain is a sentiment-driven, short-term rebound that is unlikely to be sustained, David Cui, BofAML’s head of China equity strategy, said Monday. Deep-pocketed state funds have been absent from the market, and their participation would be a last resort only if things get worse, he added, without giving specific index targets.

“If confidence in the market is lost and it declines sharply on consecutive days in huge volumes, the government may be forced to directly intervene," said Cui. “We cannot rule out such a scenario because the sentiment is jittery and fundamentals are still deteriorating. Direct purchases would be the government’s last resort as it prefers a more market driven approach."

The Shanghai gauge slid 2.3 percent on Tuesday, while the Shenzhen Composite Index dropped 1.9 percent.

Chinese authorities have a long history of stepping in to support equities via the so-called "national team" of state funds. Events of national importance, or periods of extreme volatility, are typically times when the hand of the state is seen.

But rather than the across-the-board purchases seen in efforts led by the central government in the wake of a $5 trillion sell-off in 2015, this time around aid appears to be channeled to specific companies in need of liquidity support.

Despite shares enjoying a two-day rally through Monday after top officials moved to shore up the economy and offer support to the struggling private sector, the Shanghai Composite remains one of the world’s worst performers after a selloff compounded by stock-pledge risks. With more than $600 billion of Chinese shares lodged as collateral for loans, the worry is that falling stock prices would trigger a downward spiral of forced selling. This can trigger systemic risk through contagion, said Cui.

China’s central bank announced on Monday a plan to support bond financing by private firms, while the Securities Association of China said eleven securities firms agreed to invest a combined 21 billion yuan ($3.02 billion) for an asset management plan designed to ease share-pledge risks of listed companies with sound prospects.

When China’s stock market bubble burst in 2015, the national team bought into index heavyweights such as state-owned banks and energy companies. This time around smaller private enterprises are pressuring the market, but it’s harder for the government to justify buying companies considered riskier with public funds, Cui said.

Private companies are higher risk because collateral requirements by lenders make it more difficult for them to obtain funds, compared with state-owned enterprises that are seen as offering an implicit guarantee of repayment, said Cui.

"Given the high leverage in the stock market and the uncertain outlook, I’m wary of the market dynamics," he said. "Moral suasion only works in the short term."

To contact the reporter on this story: Kana Nishizawa in Hong Kong at knishizawa5@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, David Watkins

©2018 Bloomberg L.P.