Baidu Outlook Disappoints After Covid Surge, China Crackdown

Baidu Outlook Disappoints After Covid Surge, China Crackdown

(Bloomberg) -- Baidu Inc. delivered a conservative outlook for the current quarter as a resurgent pandemic outbreak in China overshadowed the internet search giant’s push into newer arenas like cloud and smart devices.

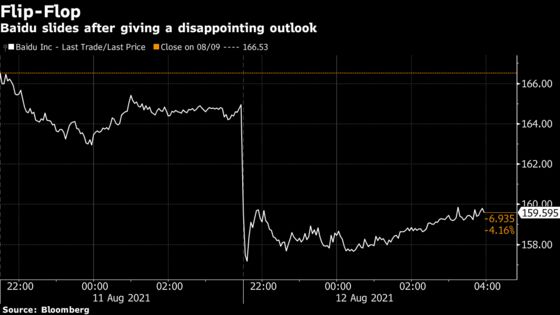

Revenue for the three months ended June climbed 20% from a year earlier to 31.35 billion yuan ($4.8 billion), compared with the 30.9 billion yuan of estimates. The company predicted sales of 30.6 billion yuan to 33.5 billion yuan for the September quarter, versus the 33.1 billion yuan seen by analysts, saying that the recent increase in Covid-19 cases across large parts of China left business visibility “limited.”

Baidu swung to a net loss of 583 million yuan in the second quarter, after marking down the value of its stake in Kuaishou Technology. Shares of the livestreaming giant sank 28% in the quarter and are currently trading below its initial public offering price, as China’s tech crackdown expands beyond e-commerce and antitrust to online content. Baidu’s stock dropped 3.2% in New York trading.

On Thursday, executives fielded questions on regulatory uncertainties from data security to the scrapping of tax incentives. When asked about the possibility of more state control over private-company data, founder Robin Li said he hasn’t heard anything “that’s very abrupt” or “adverse” to business operations. Chief Financial Officer Herman Yu, who’s moving into a new role as chief strategy officer, predicted government incentives like tax breaks will shift from older consumer internet businesses to high-tech areas like electric vehicles and artificial intelligence, after Alibaba Group Holding Ltd. was said to have recently warned investors of fewer tax breaks for the industry.

What Bloomberg Intelligence Says:

Baidu’s below-consensus 3Q sales outlook appears prudent given rising risks to its core online advertising business from the spread of the delta variant of Covid-19, even as the business performed strongly in 2Q. Strength in artificial intelligence, cloud and other new business segments may remain through 2H and beyond after 2Q’s 80% year-on-year growth, but at just 16% of total revenue, the heavy investment required to sustain this expansion may keep weighing on profits.

-- Matthew Kanterman and Tiffany Tam, analysts

Click here for the research

Once China’s runaway leader in desktop search, 21-year-old Baidu is trying to reposition itself as an AI company with use cases in everything from ride-hailing to smart speakers and the cloud. It has teamed up with carmakers like BAIC and Geely to develop autonomous and electric vehicles, while expanding a nascent chip business beyond just in-house applications.

Baidu “continues to invest heavily in new areas to capture the new frontier of technological development and to diversify its business beyond search,” TH Data Capital analyst Tian Hou wrote in a note before the results. “While some of these businesses are still in relatively early stages of monetization including its AI and no-man driving businesses, they are in the phase of rapid growth.”

Near term, Baidu is still counting on search and other content offerings like live-streams and web shows to fuel its advertising platform, which contributed roughly 66% of sales for the second quarter.

While Li’s firm has largely escaped Beijing’s campaign to rein in big tech, a harsher-than-expected ban on for-profit after-school tutoring will likely cripple the spending power of some of its key ad clients. Executives on Thursday told analysts that the K-12 segment represents a smaller portion of its revenue from the education sector.

Its Netflix-style service iQiyi Inc. could face tighter scrutiny after state media criticized platform operators for hyping up celebrity fan culture. The video platform on Thursday forecast third-quarter sales of 7.62 billion yuan to 8.05 billion yuan, compared with the 7.9 billion yuan average of analyst estimates.

©2021 Bloomberg L.P.