The Bad Economic News That Used to Be Good Is Just Bad Right Now

The Bad Economic News That Used to Be Good Is Just Bad Right Now

(Bloomberg) -- Why is bad news still bad news for battered equities? The Fed put for financial markets and the China put for the global economy have disappeared simultaneously.

In prior periods of stress, bad economic data could often be framed as positive for risk assets: It increased the odds of support from one of the world’s two largest economies. Either the Federal Reserve would cool its jets on normalizing policy or even add stimulus, or Chinese policymakers would step in with measures to bolster demand.

Investors using this playbook have been bludgeoned as of late. U.S. stocks slid Thursday under the weight of Apple Inc.’s revenue downgrade and the ISM Manufacturing purchasing managers’ index showing its sharpest one-month drop since October 2008. That followed Wednesday’s frail reading on Chinese manufacturing. A slowdown in growth may have been expected this year, but not one this severe or this soon.

“Due to the weak China-related data such as PMIs, Asian exports and Apple guidance, the narrative which is taking hold is that either the policy stimulus currently under way from Beijing is not sufficient or it’s not effective,’’ said Mayank Seksaria, chief macro strategist at Macro Risk Advisors. “Both the Fed -– via lower hike expectations -– and China expanding credit -– are trying to cushion the slowdown, but are so far not trying to reflate.’’

China faces self-imposed constraints on bolstering domestic activity, as it conflicts with another goal: the financial deleveraging campaign.

When it comes to the U.S. central bank, American equities have seemingly priced in the carrot -– easier policy in response to an economic slowdown -- without pricing in the stick -– a deterioration in earnings that would elicit such a reaction.

Coming into 2019, bottom-up forecasts suggested earnings per share growth of 8.3 percent for S&P 500 companies was in the offing. For 2020, that metric is north of 10 percent. Meanwhile, the gap between January 2019 and 2021 federal funds futures contracts implies nearly one 25-basis point rate reduction over this stretch.

Peter Cecchini, global chief market strategist at Cantor Fitzgerald, says it’s also about one tool Fed Chairman Jerome Powell “is unwilling to use to respond to bad news” -– the pace of the central bank’s balance sheet normalization.

Add to this dynamic a European Central Bank that’s also far less accommodative in supporting the periphery and Chinese data that’s rolling over and it’s easy to see why risk aversion has ramped up, according to the strategist.

“But it’s still too early for markets to price in any late 2019 recession outcome, because the question is: What is the central bank response going to be?” he added. “I highly doubt that Powell and the Fed are going to remain static; they will react to the ISM data, they’re not going to sit still.”

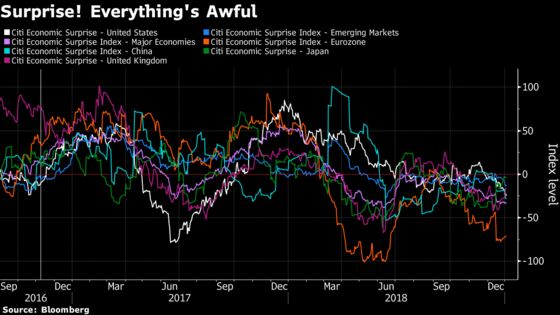

The latest data confirm that the U.S. is no longer immune from a synchronized slowdown in global activity. Economic surprise indexes for virtually every major region and country are in negative territory at the turn of the year.

This subpar data has investors seeking safety in liquid, haven assets, chief among them U.S. Treasuries. The iShares 20+ Year Treasury Bond exchange-traded fund is on its longest weekly winning streak on record, with 10-year Treasury yields tumbling 65 basis points over the course of less than two months.

Nonetheless, investors are still holding out hope for positive catalysts for risk appetite from the U.S. and China -- both separately, and together -- while acknowledging that the scope may be more limited.

“Global risk appetite is more sensitive to weakening Chinese data because of the perception that they have less room for stimulus because of their concern over high debt,’’ said Alec Young, managing director of global markets research at FTSE Russell. “On the other hand, if the Fed confirms the market’s increasing view that there won’t be any rate hikes in 2019 because of slowing global growth, that could help risk appetite. So could any improvement on U.S.-China trade negotiations.”

--With assistance from Wendy Soong and Ye Xie.

To contact the reporters on this story: Luke Kawa in New York at lkawa@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka, Andrew Dunn

©2019 Bloomberg L.P.